Editor’s introduction: The travel retail division of French drinks group Pernod Ricard is maintaining its sharp recovery from the impact of the pandemic through a well-nurtured premiumisation and pricing strategy. The Chivas Regal to Martell powerhouse posted a +33% year-on-year rise in travel retail sales for the first nine months of financial year 2023 ended 31 March. By the end of the financial year on 30 June, business in this ‘must win’ channel should reach pre-pandemic profit levels, according to group senior management.

Asia Pacific travel retail, in particular, was hard hit by the COVID-19-induced slowdown over the past three years, but that sector of the business is resurgent amid a rebound in travel.

At the recent TFWA Asia Pacific show, Pernod Ricard General Manager North Asia Travel Retail Simon van Moppes spoke to Dermot Davitt about sales acceleration, opening the doors to new consumers, the role of Hainan, product development and more.

The Moodie Davitt Report: We have seen a positive return of business for Pernod Ricard in travel retail this year, with strong growth in the first nine months and the outlook good for the financial year through June. What dynamics are driving the return to growth in your region, North Asia, in particular?

Simon van Moppes: We have talked about and read a lot about revenge travel and revenge shopping. To add to that for the Singapore show week I would add a new variant, ‘revenge TFWA’. The mood at the show really represents the recovery that is happening.

Specifically in North Asia, we are delighted to be out of this tunnel that was the pandemic after a very tough three years.

The first big step change was last October when Japan opened up to overseas visitors. I know because I was travelling there at the time and the restrictions suddenly fell away. The business accelerated fast from that point and has been nothing less than incredible since. It has not been without its challenges, such as staffing and supply, but now we are back at the point where our business in Japan is pretty much 100% of what it was in 2019.

Then in January this year we had the policy change in China which allowed travel to ramp up, though there is still a lot more to come with many countries yet to be added to the list of destinations for overseas tour groups.

We are already seeing huge step changes, depending on the location and the nature of travel. Take the border business between Hong Kong and China. Once those borders are open, they go back to 100% of the business almost overnight. A great example is the West Kowloon rail duty free business operated by Dufry, which has seen a really strong recovery.

The recovery is not without its headwinds. There remains some nervousness to travel among the population, and there are visa and passport processing challenges, though we understand that the issuing of visas is speeding up quickly now.

The biggest challenge to the industry more widely is cost of travel and capacity. There is a shortage of airline seats and those seats are expensive. There is a foreign exchange impact in some key markets such as Japan, which is amazing value to visit but very expensive if you’re Japanese and travelling overseas.

We must understand that things will take time and it will be 12-18 months before we get back to full recovery.

At Pernod Ricard we look at the big picture. Central to that is the rise of the middle class, with another billion people in Asia joining that cohort by 2030, according to projections. These are our travellers, our shoppers and that gives us a positive view of the outlook for travel retail.

To look at the Chinese shopper more closely, what are your observations about purchasing behaviour through COVID and today that affect your thinking and investments?

Certainly the trend that had started before COVID, and really accelerated during and after, is the multiple touchpoints across travel retail through which we engage. Omnichannel has become even more important. Shoppers do far more research before they travel; they look at prices and products more closely than ever.

But while digital engagement is vital, let’s not forget the physical in-store experience. That is really critical. We have invested a lot not only in the digital side, but also in the physical presence, in brand visibility, training of staff, new training tools and making sure we can have the right conversations in the right languages with the consumers who are travelling.

It’s also important to have a portfolio which offers something for everyone at multiple price points. We see in some locations that spend is way ahead of passenger growth, and passengers who are travelling are spending more. But equally, there are some locations where the spend per head is coming down because of economic considerations.

We have noticed both of these things happening in Hainan. There are people who visit who spend a lot of money. Among others, the average spend is lower. The important thing is to be able to cater for all budgets.

On that question of price, how do you continue to balance the premiumisation we see across the channel with catering to a younger adult audience, new demographics with new aspirations?

I don’t have any concerns about our ability to do this. We have 70 pieces of NPD coming through in the next 18 months. We have very high-end whiskies that we can only supply in very limited quantities, and that does not satisfy the demand among whisky connoisseurs and enthusiasts.

Then we have examples such as the limited-edition Royal Salute 21 Year Old Jodhpur Polo Edition, one of a series that is sold at a slight premium to the original 21 Year Old, but that is very interesting and collectable. These expressions are also accessibly priced and give people a way into some very unusual products in blended whisky.

You need a multi-faceted approach and we offer that. Among single malts the price is going up and up as demand way outstrips supply, despite regular and continuous price evolution.

But then we also have some very nice entry levels items that appeal to the young and trendy and that offer a recruitment tool to whisky too.

The important thing about all the NPD we deliver is that it is innovation with purpose. That can be a new brand coming in through acquisition, repackaging, modernising, and extensions that people want to see.

And one thing related to this is that as people travel again for the first time since the pandemic, after several years of not travelling, they will find completely new products on the shelves, including travel retail exclusives. Bringing that excitement into travel retail remains absolutely critical.

These exclusives play a really important role. When we do our traveller segmentation studies, we get to understand why people buy in travel retail. Gifting, collecting, value for money are all levers, but it’s also about finding things that shoppers cannot find elsewhere.

Where do you see the next big category opportunities emerging in your region?

The consumer in Asia looks for whisky and Cognac, but other categories are growing fast. In North Asia, although gin is small, we see it starting to grow fast in domestic markets and become an opportunity in travel retail.

We recently acquired KiNoBi gin, with three expressions in the range, and that category is very interesting for us. We have started in Japan as the home of the line, but there is interest in Taiwan, Korea and further afield.

In non-Scotch, Jameson has always been part of our range but we want to develop it in a way that has synergies with domestic markets. Triple Triple is a travel retail exclusive, we have Black Barrel, and other rare, high-end whiskies such as the Spot range and The Midleton. We will deploy these but they are rare so we need to selective. It is a long-term journey.

The Irish whiskey category is about a clear strategy in how we seed beginning with Jameson, moving into the higher styles and there is a lot of interest. Taiwan is a vast whisky market and the partners there are excited about how we develop it. We are making progress there already from a small base.

In American whiskies, we have a strong portfolio, and that is an opportunity. The key thing is to be clear on which markets to go for, and establish where the associations are, and how the traveller-market combination works.

To grow these emerging categories, one aspect is brand recognisability; the other is to find rare and unusual things that interest consumers.

Beyond the product offer, how do you see the evolution of the wider shopper experience? How much have traveller expectations changed and how well do you think we as an industry are responding?

The more the more experiences you deliver, the more experiences people want so it is about keeping things fresh. Because we live in this world of travel retail, we are among the most regular visitors to airports and duty free stores. But the average traveller only sees the shops infrequently. They will see something new each time and it’s important we have something new to delight them and give them an element of theatre. This is something we are very focused on.

We are very proud of having introduced the first in-airport Martell AI-powered boutique with Lotte Duty Free at Singapore Changi Airport. We have a range of immersive experiences and services for passengers including an AI Ambassador, fully-digitalised merchandising units, robot bartenders and VIP tastings.

We developed that robot arm and service in Hainan also, which has proved very popular.

AI-enabled tools in that regard are great, as is customisation and creating a personal experience, because people choose which product they want to taste or sample as part of the purchase.

And we also do a lot of personalisation now with laser engraving on the bottles. That is a fun thing to do and is very rewarding for the shopper.

You mentioned the evolving Hainan market. How do you see the role of offshore duty free there now that overseas travel in China has restarted? What are the long-term prospects?

I have been developing the Hainan business on behalf of Pernod Ricard since 2020. We decided to make a big investment there with the boutiques that you see now and we did that because we believe fundamentally in Hainan now and for the future.

I get asked a lot about Hainan’s role and future once international travel comes back. My answer is similar each time. Before COVID there were already tens of millions of travellers coming to Hainan each year, more even than go to France, which is the most visited country in the world by tourists. The scale of the opportunity remains vast.

Even when international travel is coming back now, why would people stop going to Hainan? In fact we believe more people will travel there. We have no concerns about that. It may be that during the course of a year they make two international trips and one trip to Hainan, but the number of people overall to Hainan will only increase.

Then it’s about making sure we have a steady, growing business and the right kind of business. We see Hainan as a great platform for brand-building, for retail theatre and where we can place a highly relevant offer and interact with the travellers who come. We do all that in partnership with our domestic business with which we are building synergy. We are talking to the same consumers after all, and what we do builds support for our brands in the domestic market as well.

The Hainan government has a strong desire and a game plan to increase international tourism. I can’t predict how that is going to develop but I am encouraged by the many five to seven-start hotel investments, with more to come. What is also really encouraging is how some of the luxury houses are very seriously looking at and now starting to come to Hainan too.

We have talked about the potential and the upside of Hainan for spirits. What are the challenges?

On Hainan it is about establishing a business in the right way and having the infrastructure to support it. We have opened a headquarters in Haikou and now have a warehousing set-up as well. It is important to make the business efficient and ensure we can service it really well.

I don’t believe we have seen the real Hainan yet. We only entered the market in 2020, with no retail spaces, and these came alive during COVID. Since then tourism has been on a rollercoaster, with 2022 a very difficult year. So we have yet to see the potential of Hainan in normal times for our business. It won’t be an overnight wonder; it is about stable, steady progression and for us at Pernod Ricard a long-term investment.

How do you see Pernod Ricard helping to drive the future of retail, not just travel retail, and how can the company help lead the change into the future?

We are going through a huge period of change, with new channels opening up, the commercialisation of those channels. We see online click & collect and other initiatives developing which helps travellers. Beyond that we have to ensure that for spirits, we are ensuring that travellers can access our brands in all the ways they want to.

Pernod Ricard has a role to play here, working closely with retailers to make sure that we develop the business with long-term sustainability in mind.

How aligned are brands with airport and retailer partners in terms of digitalisation?

This is a really key area that we focus on with our key retailers. We have some great examples over the last few years where we have been developing, for example, boutique online stores, providing more information about the brands to drive purchasing online for collection in-store, for example.

Every single customer I have engaged with in Singapore has that on their agenda. We have quite a lot of experience with this now. It is still a journey learning about marketing online versus marketing in-store and selling online versus selling in-store. There are some different skills and different ways of doing it. We have got the advantage of being able to also learn from our colleagues in America domestic, where that has been well developed.

Pernod Ricard has a firm commitment to sustainability as a central strategic platform. How well do you think we are doing as an industry here?

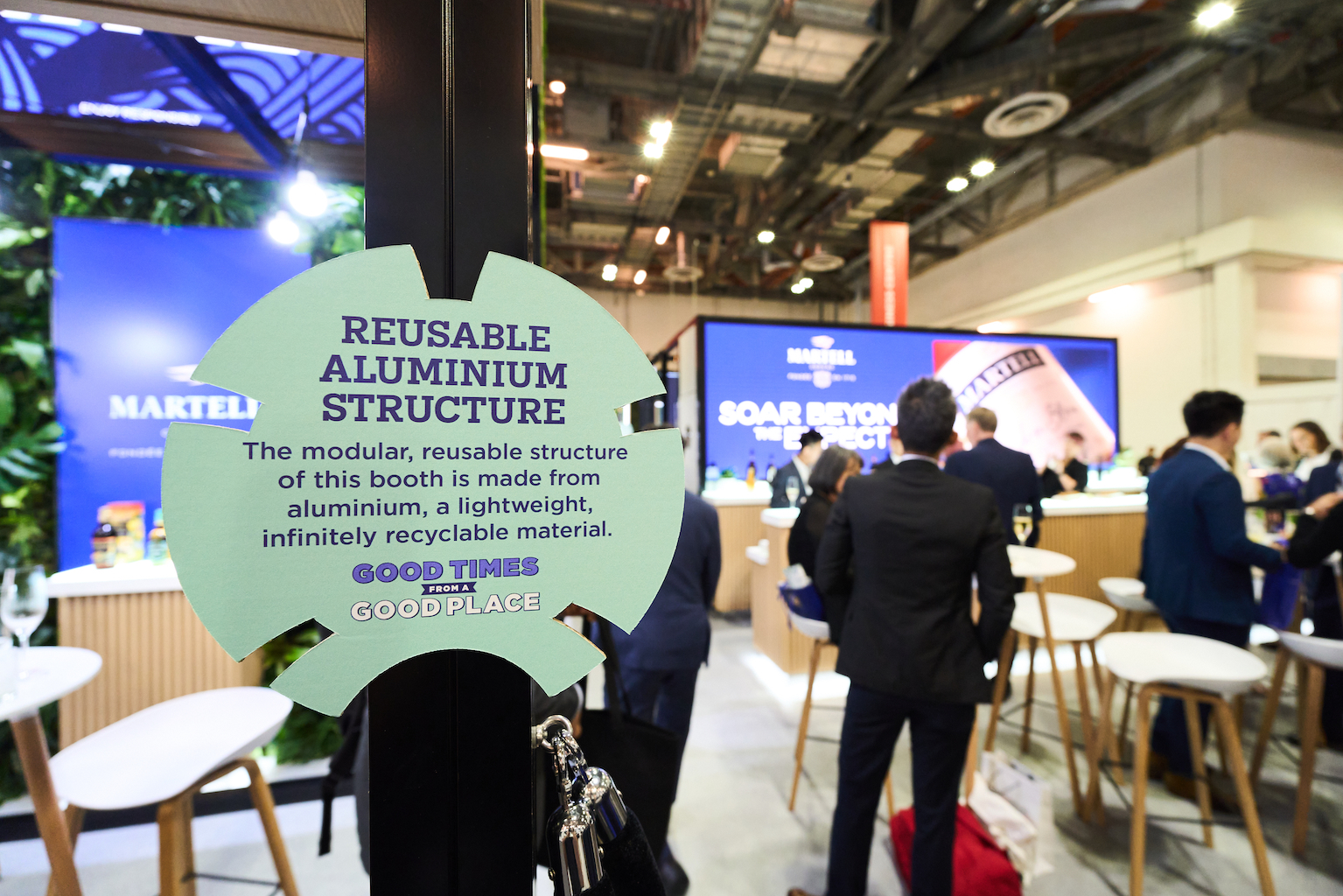

The airports should be demanding certain standards of any partner who installs a fixture of any kind today. We should have a commonality of standards around the industry. We at Pernod Ricard have taken a lead with our Lifecycle Analysis Tool, and now everything we do is analysed through the prism of that tool to assess its carbon footprint, longevity and so on.

Our entire booth in Singapore has gone through that programme too, from the materials to the plants that are all locally sourced. And our aim is to use the materials time and time again, as well as the LED screens which are made up of many small tiles that can be flexibly put together, and these represent low power consumption these days.

As a category, especially at the high end, we face the challenge of marrying sustainability with luxury packaging and the costs of doing business. How do you see this playing out in future?

It’s a vital point. For a certain level of our brands and SKUs we are going to minimise packaging, removing outer cartons and so on. This has been well publicised by us and by our competitors too.

When you go up the price ladder to more luxury products, packaging is part of the offering that people want.

This is about balancing the environmental impact of packaging versus the functionality of what we are producing. So a product which is designed for gifting or is a very high value item needs to be wrapped with some protection.

The packaging is two things: one is about the look and the design to complement the branding, but it’s a protective element as well.

What we are doing is really investigating what we do right through the supply chain, to understand how we can provide the right quality and the right brand image at the least impact on the environment.

Some packaging in our portfolio has so many different components from wood to metal to plastic, some of which is non-recyclable. But we are progressively moving to a much more sustainable packaging, even at the high end.

Our Royal Salute 25 Year Old for example is in much more sustainable packaging these days than if you look back to the old packaging with a velvet bag and a combination of leather, wood and plastic. Things have changed dramatically, and definitely there is more to do in the future. But the important thing is that it is in the mindset and that everything that is developed has sustainability top of mind.

Can we as an industry move as fast on sustainability as the consumer wants us to?

We have moved very fast with the changes to packaging at a certain level. But at the very high end, we must ask what it is that the consumer wants? We find that they do want the luxury packaging, so it’s not about removal, it’s about what materials we use.

And as with our Singapore booth for example, which used recycled materials to create a luxury effect, we can do this too with our brand packaging. We know it takes time to change the supply chain mechanics, but the important thing is that we have started.

As we go from recovery to growth in the market how do you view the evolution of industry partnerships today? Has COVID changed much in these relationships?

From a Pernod Ricard perspective, we have always said to our customers, we are not your fair weather friends, we are friends through good and bad weather. We have shown and proven that during the most challenging period for our industry.

We talk about conviviality, and while it is a phrase we use a lot at Pernod Ricard, it means doing business together on the basis of strong relationships. Yes we can have very tough conversations but we have those on the basis of strong relationships. And that is what conviviality is about. Those relationships don’t build overnight, they take a long time to develop, and they don’t stop because there is a crisis.

More broadly in the industry it is important to keep watching carefully how these relationships develop. We often talk about the Trinity and we need to make sure that now more than ever, the business works for everybody.

I don’t think we have got to the right point yet where the Trinity or even the Quaternity (including airlines) is aligned. With some recent tenders we have seen some of the big travel retailers making statements about how they view the dynamics in the industry. So clearly there is more work to do. ✈