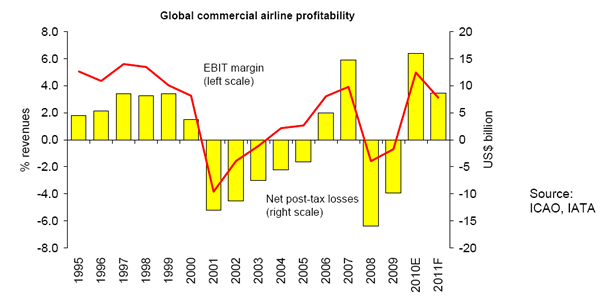

INTERNATIONAL. The airline industry’s profitability will be sharply hit by rising oil prices in 2011, according to the International Air Transport Association (IATA). The industry body downgraded its outlook for 2011 to US$8.6 billion in profits from the US$9.1 billion it estimated in December 2010.

This is a -46% fall in net profits compared to the US$16 billion (revised from US$15.1 billion) earned by the industry in 2010. On expected industry revenues of US$594 billion, the US$8.6 billion 2011 profit equates to a net profit margin of 1.4%.

IATA Director General and CEO Giovanni Bisignani said: “Political unrest in the Middle East has sent oil over US$100 per barrel. That is significantly higher than the US$84 per barrel that was the assumption in December. At the same time the global economy is now forecast to grow by +3.1% this year-a full 0.5 percentage point better than predicted just three months ago. But stronger revenues will provide only a partial offset to higher costs. Profits will be cut in half compared to last year and margins are a pathetic 1.4%.”

|

Forecast highlights

Fuel: IATA raised its 2011 average oil price assumption to US$96 per barrel of Brent crude (up from US$84 in December), in line with market forecasts. Including the impact of fuel hedging, which is roughly 50% of expected consumption, this will increase the industry fuel bill by US$10 billion to a total of US$166 billion. Compared to levels in 2010, oil prices are now expected to be +20% higher in 2011. Fuel is now estimated to represent 29% of total operating costs (up from 26% in 2010).

|

Giovanni Bisignani: “Today oil is the biggest risk. If its rise stalls the global economic expansion, the outlook will deteriorate very quickly” |

Growing economies give airlines the opportunity to recover some of these added costs with additional revenues, said IATA. For example, since early 2009, rising oil prices added 25% to unit costs while average fares (excluding surcharges) rose +20%. But in 2011 higher revenues are not expected to be sufficient to prevent the rise in oil prices from causing profits to shrink by -46% from 2010 levels.

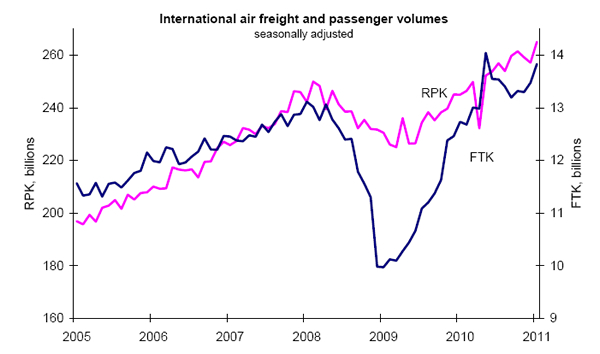

Demand: An increase in global GDP forecasts to +3.1% (from +2.6% in December) bodes well for continuing strong demand for air transport, IATA noted. In line with this, IATA revised its passenger demand growth forecast to +5.6% (from +5.2%).

Capacity: Published airline schedules indicate a capacity increase of +6%, slightly lower than the +6.1% previously forecast. Of this, 5% will come from the 1,400 new aircraft being introduced to the fleet over 2011. The additional 1% is expected to come from the normalisation of under-used capacity in the twin-aisle fleet, said IATA.

Yields: With capacity expected to increase by +6% in 2011 and demand by +5.7%, the gap is 0.3 percentage points. This has narrowed from the previously forecast gap which was 0.8 percentage points. While there has been some weakening in passenger load factors, as of January they remained near record levels at a seasonally adjusted 77.7%. Passenger yields are expected to grow by +1.5% (up from the previous forecast of +0.5%).

Premium Travel: Premium traffic is an important contributor of a network airline’s profitability. Purchasing managers’ confidence is a leading indicator for business travel. In January, the JP Morgan/Markit Purchasing Managers Index hit a record high. Moreover, strong corporate reporting at the end of 2010 and expanding world trade will continue to drive business travel in 2011, albeit at a slower pace than during the 2010 post-recession rebound, said IATA.

Risks: Rising oil prices are always a challenge for airline profitability, IATA noted. If they are accompanied by strong growing economies and world trade, airlines have some opportunity to command prices that can offset the rising fuel costs. If, however, rising energy prices stall global economic growth there is a strong downside risk to this forecast. With oil prices now being driven by speculation on geopolitical events in the Middle East rather than strengthening economic growth, this is a significant downside risk, the airline body said.

“This year the industry is performing a balancing act on a very thin tight-rope of a 1.4% margin. It is a structural problem that the industry has faced with an average margin of just 0.1% over the last four decades. There is very little buffer for the industry to keep its balance as it absorbs shocks. Today oil is the biggest risk. If its rise stalls the global economic expansion, the outlook will deteriorate very quickly,” said Bisignani.

|

Asia Pacific carriers are expected to deliver the largest collective profit of US$3.7 billion and the highest operating margins of 4.6%. This is down substantially from the US$7.6 billion that the region’s carriers made in 2010 and from the previously forecast US$4.6 billion for 2011. While the strong economic growth in the region is still driving profitability, inflation fighting measures in China are slowing trade and air cargo demand. The key reason for the downgrade from December’s forecast is that the region is more exposed to higher fuel prices, due to relatively low hedging on average.

North American carriers are expected to deliver US$3.2 billion profit, unchanged from the previous forecast and down from the US$4.7 billion profit made in 2010. Higher oil prices will damage profitability in 2011, but earlier cuts in capacity have led to much stronger conditions for yields than elsewhere. The US economy has also been stronger than expected. Compared to IATA’s December forecast, better revenues in 2011 will offset higher fuel costs.

European carriers are expected to make a US$500 million profit. This is up from the US$100 million previously forecast, but well below the US$1.4 billion that the region’s carriers made in 2010. It is the carry-over from better than expected 2010 second-half performance that has led to forecast revisions. The ongoing banking and government debt crisis are keeping domestic home markets fragile. But the weak Euro is continuing to provide stimulus to export industries, outbound freight and long-haul business travel which is driving the upgrading of the region’s profit forecast. Even so, Europe’s carriers remain the least profitable among the major regions with an EBIT margin of 1.1%.

Middle East carriers are expected to return a profit of US$700 million. This is considerably better than the US$400 million previously forecast, but down from the US$1.1 billion profit that the region posted in 2010. Political instability in the region is expected to take its toll in Egypt, Tunisia and Libya which combined account for about 20% of the region’s international passenger traffic. This is balanced by the Gulf area which benefits from economic activity related to high oil prices and whose hubs continue to win long-haul market share. Load factors have also improved significantly for these airlines, as new capacity is being added at a slower pace than demand increases.

Latin American carriers are forecast to post a US$300 million profit. This is down sharply from the US$1 billion that the region made in 2010 and from the previously forecast US$700 million. Strong economic growth and international trade in the region are driving travel and cargo demand and the region’s profits for airlines. Exposure to higher oil prices is the key reason for the expected deterioration in the region’s profitability this year.

African carriers are expected to break even. This is unchanged from the previous forecast but down from the US$100 million profit that the region posted in 2010. Strong economic and transport demand growth on the back of foreign direct investment and rapidly growing trade links with Asia is keeping the region’s carriers out of the red. However, they face intensifying competition from Middle Eastern carriers and others for lucrative business traffic, said IATA.