INTERNATIONAL. The latest Duty Free World Council (DFWC) KPI Monitor reveals a robust recovery across international air traffic and, it claims, global travel retail.

The study shows passenger volumes have passed pre-pandemic 2019 benchmarks, confirming a sustained appetite for international travel. It also claims shoppers are showing renewed engagement.

The Monitor, which is produced exclusively for the Council by travel and travel retail research agency m1nd-set, shows that in Q3 2025, international passenger departures soared to 634 million, eclipsing 2019 volumes by +12%.

Based on international traffic data provided by IATA to m1nd-set, the DFWC KPI Monitor reveals the Middle East and Africa region collectively reports the most robust zonal growth at 122% of the same 2019 number (i.e. +22%) to 74 million international departures, including connecting and non-connecting passengers.

Growth is broadly consistent across most regions, the monitor reveals. North America (121%), South America (118%) and Europe (113%) posted similarly impressive comparisons with their pre-COIVD numbers, while Asia Pacific (102%) has finally surpassed its pre-COVID volumes.

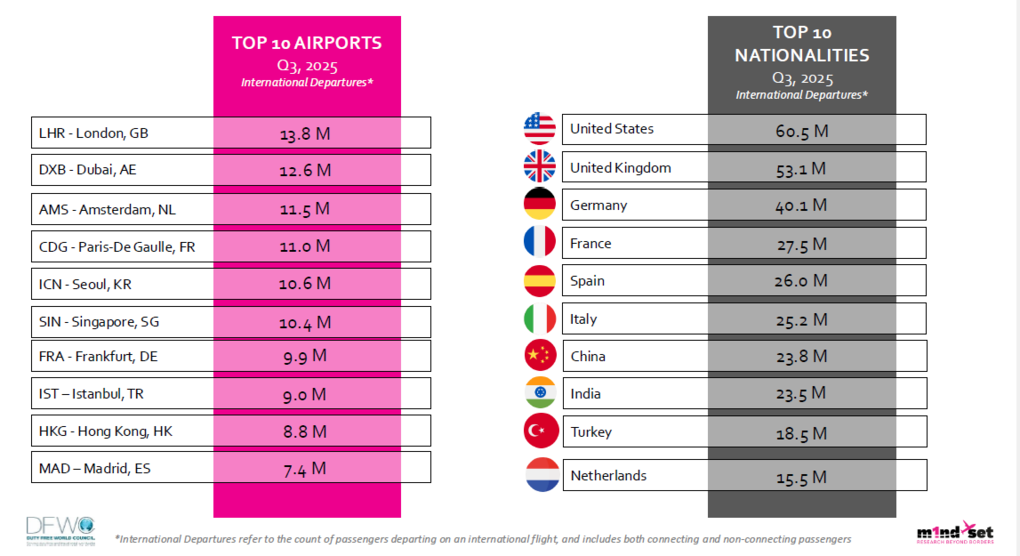

The rankings for the top ten international airports by international passenger traffic underline the strategic importance of major European and Middle Eastern hubs, balanced by strong performance among Asia Pacific gateways.

London Heathrow with 13.8 million international departures cemented its lead in the global rankings closely trailed by Dubai (12.6 million). Amsterdam Schiphol(11.5 million), Paris Charles de Gaulle (11.0 million), and Incheon (10.6 million) complete the top five.

Singapore Changi (10.4 million) follows closely in sixth position with Frankfurt (9.9 million), Istanbul (9.0 million), Hong Kong (8.8 million) and Madrid (7.4 million) rounding out the top ten.

The DFWC KPI Monitor reveals the USA (60.5 million) and UK (53.1 million) lead outbound travel by ‘nationality’ followed by strong departures from Germany, France, Spain and Italy, underlining the dominance of European demand {Note: The Moodie Davitt is confirming this definition as the table above refers to the count of passengers departing on an international flight from a country, rather than their nationality}. The figures include both connecting and non-connecting passengers,

China, India, Turkey and the Netherlands complete the top ten nationality rankings.

Turning to shopper trends, the DFWC KPI Monitor claims to highlight growing tendencies towards more self-indulgence and spontaneous purchasing, as well as positive staff interactions and renewed engagement with digital touchpoints, thanks in part to a growing share of Gen Zs among travellers and shoppers.

Shopper decisions in duty free remain fundamentally anchored in value and convenience. ’Good value for money’(26% vs 27% in Q2) and ‘convenience’ (22% vs 21% in Q2) stand out as the primary purchase drivers, while items that are ‘suitable as a “self-treat’ (19%) continue to gain traction, up from 17% in the previous quarter.

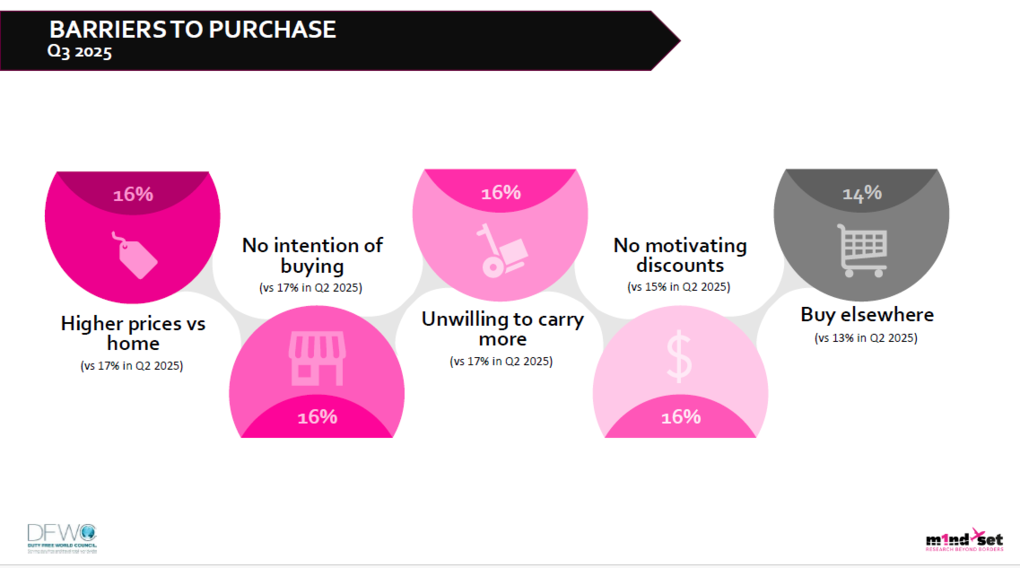

Barriers to purchase among shoppers in duty free point to price sensitivity and indifference. Despite improvement on the previous quarter, price perception still acts as a significant barrier. 16% of potential buyers are deterred by factors such as ’higher prices vs. home‘ (compared to 17% in Q2) and ’no motivating discounts‘ (up from 15% in Q2).

Shopper apathy remains a barrier too with 16% claiming they have ’no intention to buy‘ or are ’unwilling to carry more items also 16%.

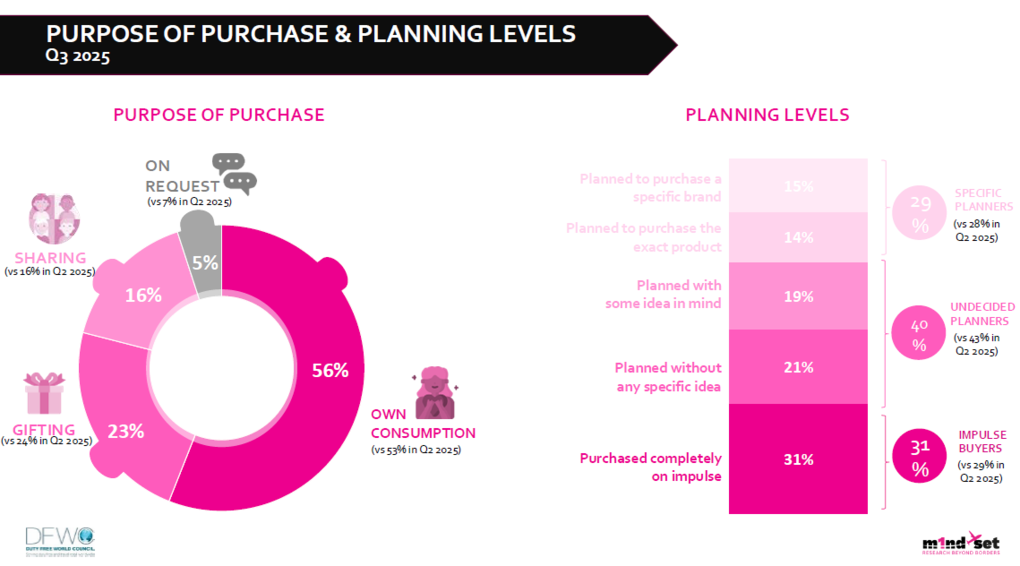

The purpose of purchase identified in the Monitor shows a clear and consistent hierarchy, with self-indulgence dominating – up 3% to 56%, followed by gifting (23% vs 24% in Q2), sharing (16% – no move) and on request (5% down from 7% in Q2).

Planning behaviour among global shoppers denotes a modest shift toward more decisive and more spontaneous purchases compared to the previous quarter, the report claims.

Impulse purchases rose from 29% to 31% between Q2 and Q3 while specific planning rose one point to 29%. The share of undecided planners fell three points to 40% across the period.

The Q3 Monitor also claims to identify a growing influence of digital touchpoints among shoppers with pre-trip digital engagement on the rise.

The share of shoppers exposed to pre-shopping information was up from 31% to 33%, primarily through internet searches (18% vs 16% in Q2), social media (15% vs 12% in Q2), and shopping sites (12% up from 10%). 11% of shoppers also searched for information on retailers’ websites, consistent with the previous quarter, while 11% also searched on travel apps, up from 9% in Q2.

{Again, The Moodie Davitt Report emphasises the m1nd-set study does not break down its sample base by nationality. The social media statistic above (15%), for example, would be much higher among, say, Chinese and Korean travellers.}

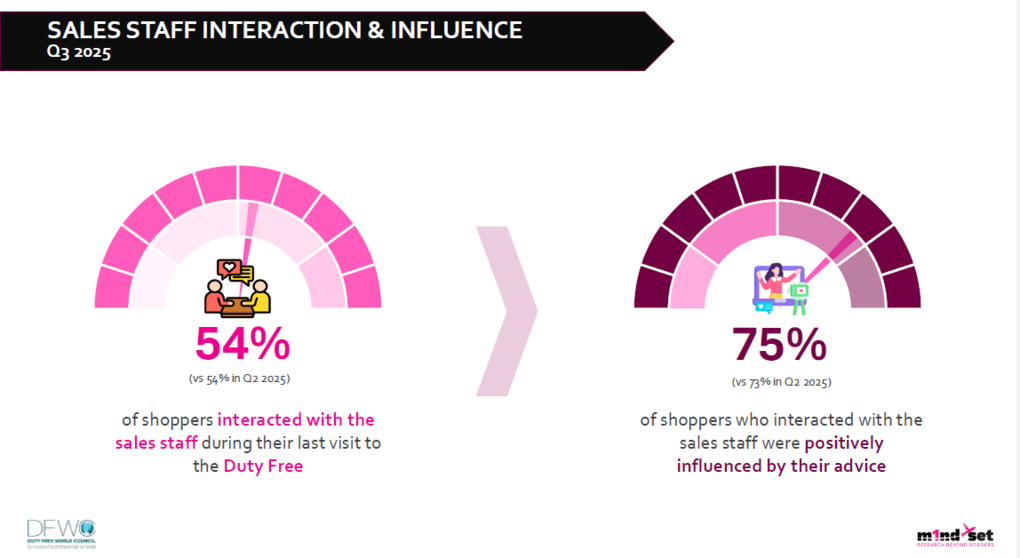

Sales staff interactions remain highly influential in driving conversion. Over half (54%) of shoppers engaged with staff during their last visit, consistent with the share in Q2, and of those 75% reported that the interaction positively influenced their purchase, up 2% on Q2.

DFWC President Sarah Branquinho welcomed the growing engagement. “The data confirms that digital and social platforms are increasingly shaping travel retail decisions before travellers arrive at the airport. confirming the growing influence of online channels.

“This provides stakeholders with a clear opportunity to engage with shoppers well in advance through these media and platforms to increase footfall and conversion.

“It is also encouraging to see the enduring power of in-store interaction.The data underlines the powerful role of personal engagement and well-trained retail staff.

“Success in travel retail lies in mastering the blend of enhanced digital pre-engagement with a personalised, high-quality in-store experience,” Branquinho added. ✈