INTERNATIONAL. Welcome to the fifth edition of The Moodie Davitt SPEND Index, a platform that tracks the effects of currency fluctuations across leading travelling nationalities and destinations – a key driver of travel retail spending.

Among all the factors affecting travel between nations, exchange rates are one of the most important, as they are central to determining relative spending power.

Our Moodie Davitt SPEND Index continues to track the effects of currency fluctuations across selected travelling nationalities and destination countries – a key driver of spending in travel retail.

The SPEND Index examines the changing value of selected home currencies against other currencies abroad. That relativity carries significant weight when it comes to decisions about whether and where to travel, and travellers’ propensity to shop while overseas.

The SPEND Index embraces 15 of the most common currencies used in global travel retail.

The nationalities that enjoy an increased spending power (‘Winners’), based on the evolution of their domestic currency over the past 12 months (up to 30 June 2019) versus a basket of other currencies, are listed below.

A SPEND Index of less than 100 indicates that the spending power of this nationality has improved over the past year due to a stronger currency. Likewise, a SPEND Index greater than 100 indicates that the spending power of this nationality has weakened due to a weaker home currency.

The nationalities to have benefited the most over the past year are those from Japan, Switzerland, Singapore, Brazil, Canada, the US and, particularly, Thailand. Currency values and rates of exchange on 30 June 2019 have been compared to those valid on 30 June 2018.

With a SPEND Index at 91.96 for Thailand, a basket of products that cost THB100 on 30 June 2018 now only costs THB91.96 on average (all countries and destinations), a significant saving of +8%.

Considerable spending power, a rising middle class and intense marketing activities by hotels, airlines and others boosted the number of Thai outbound travellers to about ten million in 2018, up from six million in 2013. Conversely, of course, the rise in the SPEND Index meant increased costs for travellers to Thailand, a key factor in a soft tourism performance this year in key locations such as Phuket.

Second-ranked Japan and the country’s travellers have benefited from the strengthening of the Japanese Yen (SPEND Index 96.75, saving +3.3%). At number three, Swiss travellers (SPEND Index 97.95, saving +2.1% have also benefitted from a stronger home currency. Both the Japanese Yen and the Swiss Franc are often termed ‘safe-haven’ currencies by investors, offering some protection in times of market uncertainty, instability and possible downturn.

The SPEND Index also offers the possibility to study details and numbers between pairs of nationality and country of destination (see table below). Destinations are given as countries rather than cities.

The above table shows that Thai travellers have been the big SPEND power winners over the past year. No matter which destination country they choose to travel to, Thai travellers are now making savings at every destination country in the SPEND index they visit compared to one year ago, due to the strengthening of the Thai Baht over the period.

Among the 14 destination countries included in the study, the Thai Baht has gained strength ranging from +12% in Australia to +4.6% in Japan, averaging +8% (SPEND Index 91.96) for all countries.

In addition to the increased spending power, accessibility is another major determining factor for Thais’ choice of destination. Japan (which eliminated visas for Thais in 2013) is currently a major destination, followed by South Korea, Taiwan and more recently Russia.

Neighbouring Association of Southeast Asian Nations (ASEAN) countries that offer visa-free access to Thai travellers are also proving to be popular destinations, while Latin America and Africa are still relatively unexplored outbound markets.

Japanese travellers also see benefits and savings when travelling to certain countries, especially Australia (SPEND Index 92.42, saving +7.6%) and the UK (SPEND Index 93.15, saving +6.9%). So far in 2019, the UK has recorded +10% more Japanese visitors than during the same period in 2018.

Brazil is seeing some recovery following the recent struggles of the Real. Travellers are able to make a saving of +5.8% (SPEND Index 94.24) on their shopping in Australia.

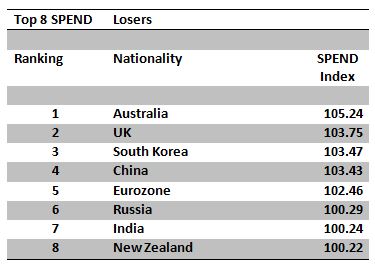

Some nationalities and currencies have suffered over the past 12 months, and those nationalities that have lost the most in terms of their spending power are shown in the table below.

The above eight countries, and their respective outbound travellers, have all seen their currencies weaken over the past year. This effectively means that the currencies are now worth less than they did a year ago.

Focusing on Australia, with a SPEND Index at 105.24, a basket of products that cost A$100 on 30 June 2018 cost A$105.24 on average one year later (all destinations), an increase in cost of +5.2%.

Likewise, UK travellers will have found that their overseas shopping spend has become more expensive (by +3.8% on average, SPEND Index 103.75) compared to 30 June 2018. Since 30 June 2019 the Pound Sterling has weakened further, making foreign destinations and shopping even more costly. Recently the Pound Sterling hit a 31-month low against the US Dollar amid increasing belief that the UK could leave the EU without a deal.

Chinese travellers have seen their overseas spend become +3.4% (SPEND Index 103.43) more expensive over the 12 month period ending 30 June 2019.

On 5 August, the Chinese Yuan weakened to CNY7.0432 to the US Dollar following President Trump’s threat of tariff hikes on additional Chinese imports. Last year on 5 August, CNY6.8314 bought 1 US Dollar, thus the Yuan depreciated -3% against the US Dollar during the 12-month period.

Notably, the Yuan hit a high in February 2019 of CNY6.6862 to the US Dollar, representing a -5.1% depreciation against the US Dollar over the past six months. As The Moodie Davitt Report recently wrote: “In travel retail terms the impact is straightforward – a weaker national currency means lower spending power abroad in any Dollar-based or Dollar-linked market. With the Chinese so fundamental to the global travel retail sector’s health, retailers and brands alike are monitoring the situation anxiously.”

As mentioned, there is always a flip side to a strength or weakeness of a currency. All nationalities now find it more expensive to shop in Thailand (SPEND Index 108.88) compared to a year ago, due to the strengthening of the Thai Baht against all the other currencies in the basket. While the average cost increase for all visiting nationalities is +8.9%, this ranges from +4.9% for the Japanese to +13.4% for Australian shoppers.

As noted above, a strengthened domestic currency has many advantages benefiting Thai travellers when shopping overseas, but there are also consequences for duty free shopping activities and economic realities at home.

There is still a significant gap between the number of tourists visiting Thailand and the number of Thais going abroad. In 2018, there were 38.3 million visitors to Thailand with about 10 million Thais going abroad, a ratio of 4:1. The valuation of the Thai Baht against other currencies is therefore of vital importance to the Thai domestic duty free industry.

Airports of Thailand recently approved the bid results for a number of major commercial concessions at its airports, confirming King Power International Group and its subsidiaries as winners. The retailer has a number of exciting and manageable challenges ahead, but one over which it can exercise no control is the rate of exchange between the Thai Baht and other currencies (although it can tailor pricing and promotions if necessary).

The Thai export industry, of which the Thai duty free industry is an intrinsic and integrated part, has expressed strong concerns and worries about the strength and possible continuing strengthening of the Thai Baht, making their products uncompetitive.

The current strength of the Thai Baht hurts Thai duty free retailers in two main ways. Firstly, the current high valuation of the currency can discourage some 10 million annual Thai travellers from shopping in domestic duty free shops upon departure or arrival. Instead, in order to reap some of the benefits of their strengthened currency, they may choose to shop upon arrival or departure at international destinations.

Secondly, the table above shows that all 14 nationalities will find the duty free prices in Thailand to be ‘expensive’, at least when compared to the prices of a year ago.

The consequences of the strong Thai Baht for the Thai tourism and duty free industry have already become visible.

In the first quarter of 2019 the number of visitors to Thailand increased from 10,608,686 to 10,795,246 year-on-year [Source: Tourism Statistics Thailand]. Authorities considered this +1.75% increase to be poor. “The strength of the Baht is part of the reason why the number of tourists has dropped as those who come would get less money from their currencies to spend,” Thailand Tourism Minister Piphat Ratchakitprakam commented in June.

Given that Chinese travellers made up 27.5% of all visitors to Thailand in 2018, a possible continued depreciation of the Chinese Yuan would not be a positive development for the Thai duty free industry.

On 7 August, Thailand’s central bank cut its benchmark rate by 25 basis points to 1.5%, with the aim of combating a weak economic outlook and partly due to the strength of the Thai Baht hurting the export industry.

The Moodie Davitt SPEND Index analysis embraces 210 nationality and country of destination pairs, as well as 15 averages for nationalities (225 value indicators). It will continue to monitor the consequences and possible impacts of currency fluctuations on duty free and travel retail trade in the months ahead.

PREVIOUS EDITIONS OF THE SPEND INDEX