SOUTH KOREA. Improved results from its Shinsegae Duty Free division and an influx of foreign travellers to the core department store business helped Korean retail powerhouse Shinsegae deliver a strong Q4 performance.

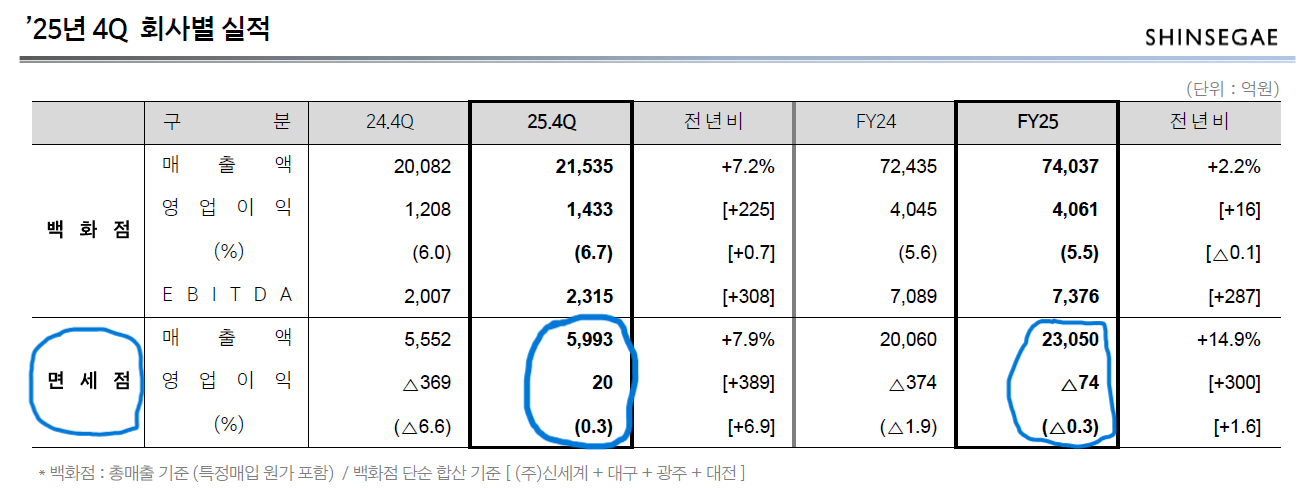

Shinsegae Duty Free’s Q4 sales rose +7.9% year-on-year to KRW599 billion (US$416 million). The travel retailer’s operating profit improved exponentially from a thumping loss in Q4 2024 (see table below) to a profit of KRW2 billion (US$1.39 million) a year later.

For the full year, Shinsegae Duty Free sales increased +14.9% to nearly KRW2.31 trillion (almost US$1.6 billion), while the operating loss improved from a whopping KRW374 billion (US$259 million) in 2024 to KRW74 billion (US$51.3 million) deficit in 2025.

The group said its duty-free performance had been boosted by a continued focus on profitability (notably through improved inventory management efficiency), though increased airport rent due to higher passenger departures added KRW7.8 billion (US$5.4 million) to costs.

Department store business rivals duty-free shopping for foreigner spending

In a trend being mirrored at Shinsegae’s arch-rival Lotte, which also operates across multiple retail channels, the department store business benefitted from a sharp rise in inbound passenger traffic annd increased business with foreign shoppers.

Sales to international visitors rose from 4.5% of business in Q1 2025 to 5.7% in Q4.

Shinsegae said the duty-free business had benefitted from a continued emphasis on “profit-focused operations” and strong sales of overseas fashion and imported cosmetics.

The group said it is establishing a foundation for mid- to long-term growth through restructuring of subsidiary business structures.

That reference includes Shinsegae Duty Free, whose Incheon International Airport DF2 concession is set to end on 27 April, following the retailer’s decision to quit the heavy loss-making contract in late 2026 (and not to bid on the subsequent retender).

Mirae Asset Securities Equity Research said in a note: “Shinsegae [i.e. total group] posted above-consensus Q4 2025 results, with net revenue of KRW1.93 trillion (+6% YoY) and operating profit of KRWW172.5 billion (+66% YoY).

“Strong revenue growth at department stores was the main driver of profit growth, while the duty-free business delivered an unexpected return to profitability.

“Looking ahead, structural drivers of department store growth should remain intact, and the firm’s exit from the DF2 zone at Incheon International Airport should enhance duty-free earnings visibility.

“While rental expenses increased both YoY and QoQ due to higher airport passenger traffic, profitability recovered on the back of improved commission rates at downtown stores and inventory optimisation.

“While cost pressures should grow again with the end of the temporary rental fee reduction for Incheon International Airport’s Terminal 2 zone in Q1 2026, most of the rental expense burden should be lifted after the company exits the DF2 zone in April.”

The department store business generated almost KRW7.4 trillion (US$5.3 billion) in sales for 2025, up +2% year-on-year. Operating profit edged ahead +0.4% to KRW406.1 billion (US$285 million).

Mirae Asset re-rated Shinsegae to hinge on inbound tourism momentum. “Accelerating wealth effects continue to support the department store segment and inbound tourism growth has emerged as an additional catalyst. We believe Shinsegae is positioned as the major beneficiary of these trends… further upside will likely hinge on confirmation of sustained inbound tourism momentum.

“In this regard, key factors to watch include the strength of Chinese tourist flows, Won weakness, and China-Japan travel developments.” ✈