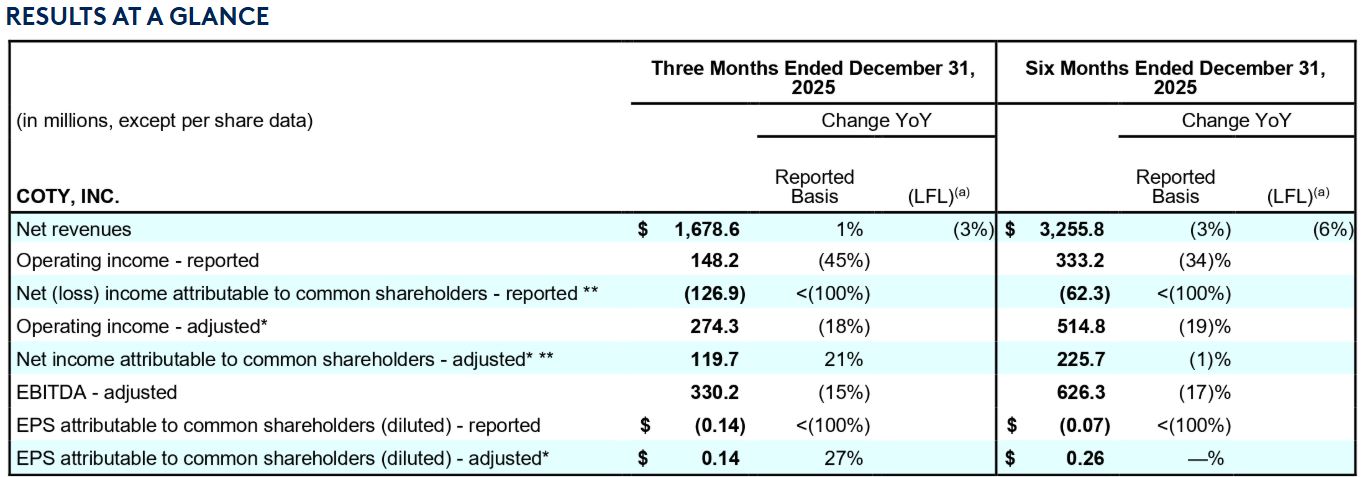

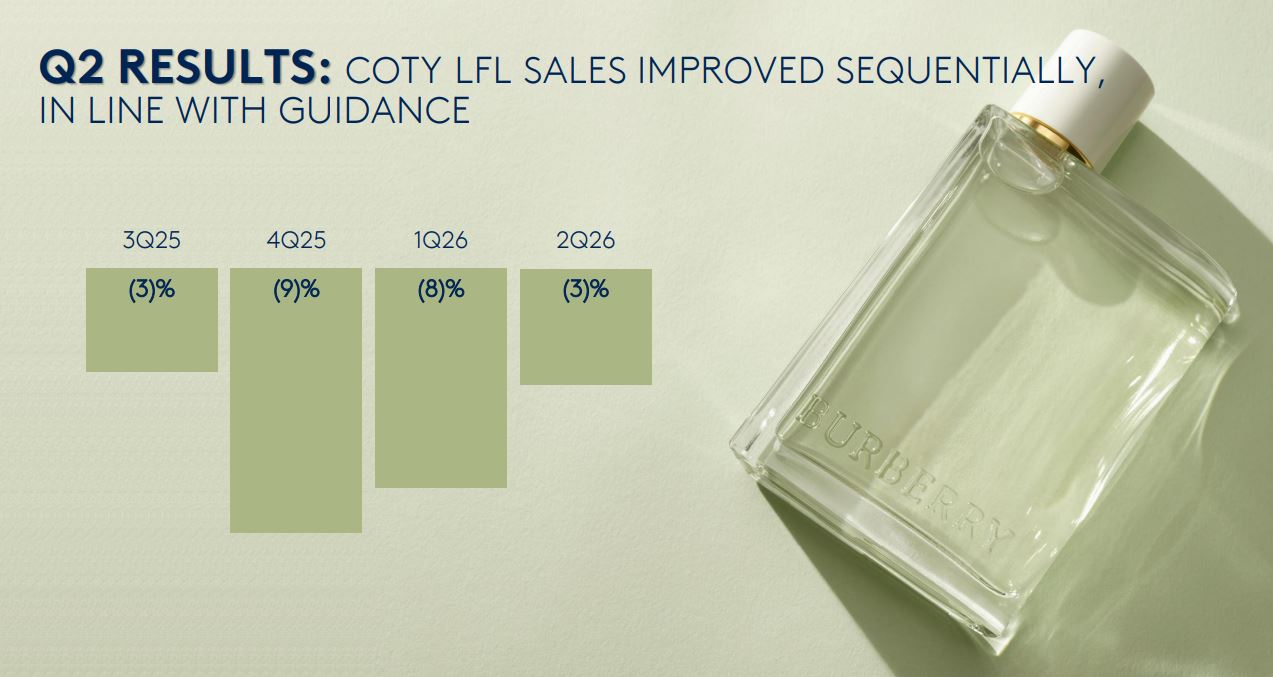

Coty has reported US$1,678.6 million in net revenues for the second quarter ending 31 December 2025, marking a +1% year-on-year increase on a reported basis (-3% like-for-like).

The results aligned with forecasts while cutting net debt and leverage to their lowest levels in nearly a decade, the company noted.

Weaker sales were recorded in key markets, including the USA, Germany and the UK, but largely offset by strong sell-out in travel retail and emerging markets such as Asia Pacific, the Middle East and Latin America.

Following his recent appointment, Coty Executive Chairman and Interim Chief Executive Officer Markus Strobel said, “I’m truly excited and energised to join Coty at this pivotal moment.

“In my first month in the role, having visited our largest markets and key sites, it’s very clear to me that Coty has many top-notch assets and competitive advantages: highly attractive brands, best-in-class fragrance innovation capabilities, a vertically integrated business model, and a creative, entrepreneurial organisation.

“At the same time, our financial performance over the past year and a half has been disappointing, and our current share price reflects that reality. Both things are true: Coty has outstanding assets and capabilities, yet we have not been delivering at the level we should.”

The Prestige segment led overall revenues, contributing US$1,133.6 million, or 68% of total sales, up +2% on a reported basis (-2% like-for-like).

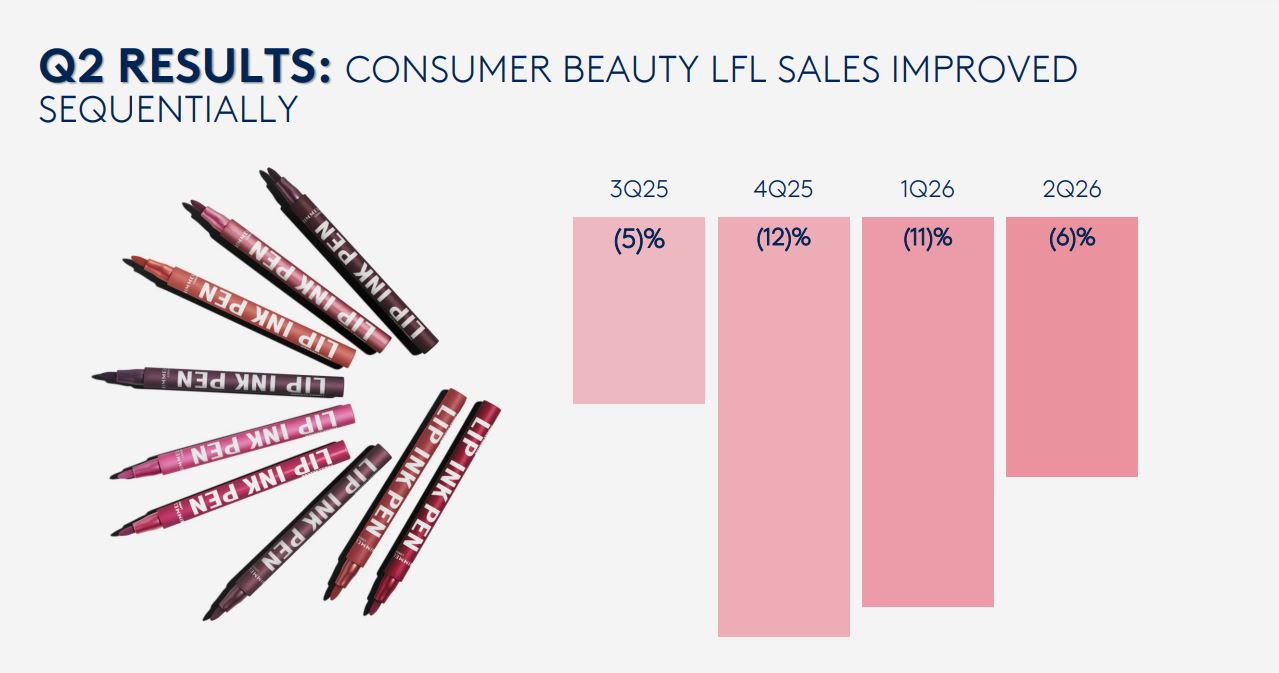

Consumer Beauty added US$545 million, accounting for 32% of total sales, with a -2% reported decline (-6% like-for-like).

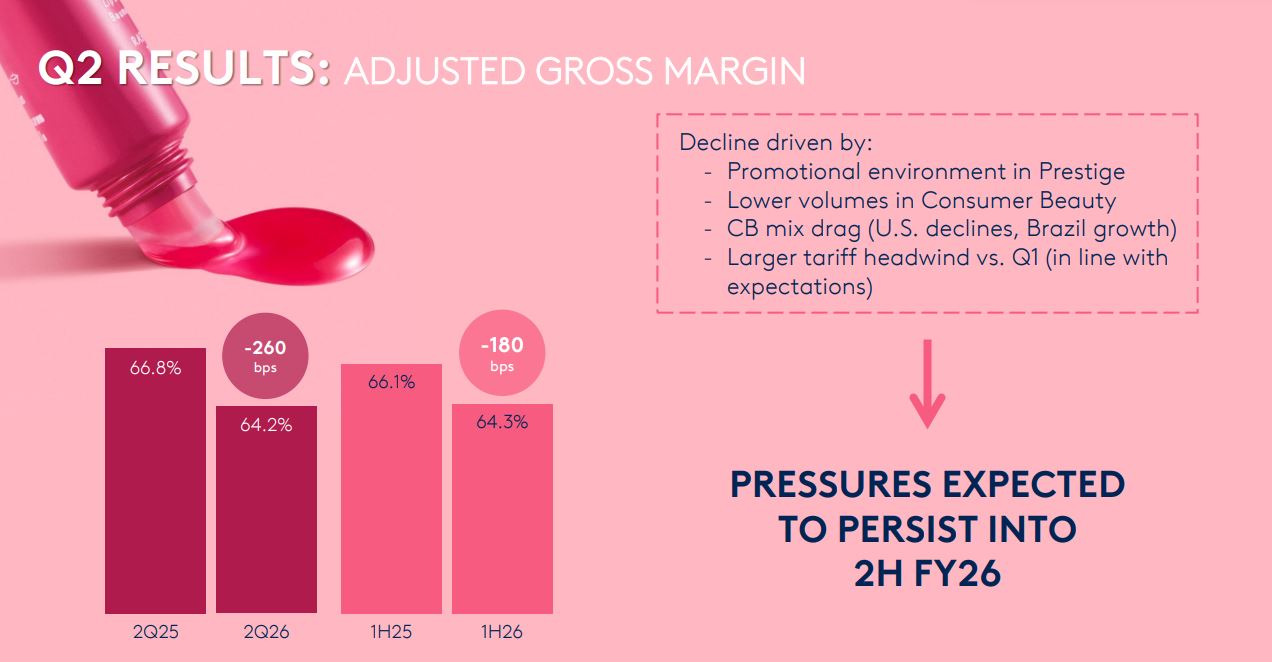

During the period, Coty reported a gross margin of 63.8%, down 290 basis points year-over-year, while adjusted gross margin declined 260 basis points to 64.2%.

Reported operating income stood at US$148.2 million, down from US$268.2 million in the prior year, resulting in a reported operating margin of 8.8%.

Adjusted operating income fell -18% to US$274.3 million, with the adjusted operating margin declining 370 basis points to 16.3%.

The beauty company posted a reported net loss of US$126.9 million, down from a net income of US$20.4 million from the previous year, with a reported net loss margin of 7.6%.

Adjusted EBITDA fell -15% to US$330.2 million, with the adjusted EBITDA margin declining 370 basis points to 19.7%.

Performance by segment

The Prestige segment showed signs of stabilisation in Q2, with net revenue reaching US$1,133.6 million, representing 68% of total quarterly sales.

Reported growth of +2% was supported by favourable currency movements and strong performance in EMEA, despite ongoing challenges in the Americas.

The like-for-like revenue decline of -2% reflected a sequential improvement driven by a sharp reduction in retailer destocking.

Category performance was mixed, with prestige makeup improving in the mid-single digits, led by Burberry and Kylie Cosmetics, while skincare achieved double-digit gains, led by Lancaster and philosophy.

The Consumer Beauty segment generated US$545 million in net revenue during Q2, accounting for 32% of total sales.

Reported revenue dropped -2% (-6% like-for-like) as strong mass skincare performance and a 4% foreign exchange benefit partially offset declines across colour cosmetics, body care and mass fragrance.

Performance by region

Americas net revenue in Q2 totalled US$624.5 million, representing 37% of overall company sales.

Reported revenue fell -2%- (-3% like-for-like) as both Prestige and Consumer Beauty segments underperformed, despite a 1% positive foreign exchange benefit.

EMEA delivered US$864.2 million in net revenue during the period, up +3% as reported (-4% like-for-like). The reported increase was supported by a 7% FX benefit, while weaker performance in Prestige fragrance and Consumer Beauty colour cosmetics offset gains.

In Asia Pacific, net revenue stood at US$189.9 million in net revenue in Q2, declining -1% on a reported basis (-2% like-for-like).

The result was weighed down by the slow growth in Southeast Asia, but strong results in China, including Hainan, and Japan drove positive growth.

Strobel concluded: “To step-change our performance and channel our strengths, we are initiating our ‘Coty. Curated’ strategic framework, encompassing sharper priorities, more focused investments, improved execution, and increased support behind our core businesses. These actions are anchored in consumer demand and a relentless focus on sell-out and market share.

“In parallel, we are continuing our portfolio review to identify opportunities to unlock shareholder value in both the near and long term, complemented by other value-driving opportunities, such as our recent divestiture of our remaining stake in Wella at the end of CY25, delivering on our commitment.

“With greater focus and discipline, I believe Coty is well positioned to deliver consistent, profitable growth and realise its full potential.”

Coty also noted it is withdrawing its full-year FY26 outlook for EBITDA and free cash flow, citing a complex market environment and its ongoing leadership transition, and will provide guidance only for Q3.

Like-for-like revenue in Q3 is expected to decline by a mid-single-digit percentage, reflecting continued weakness in Consumer Beauty trends. ✈