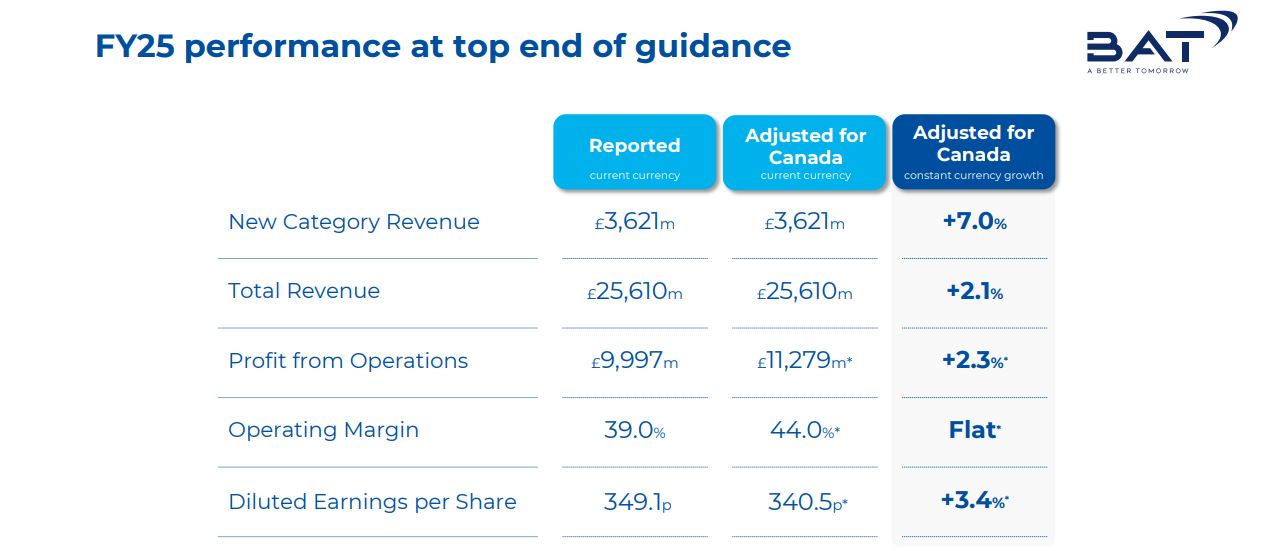

BAT delivered revenue of £25,610 million for the year ended 31 December 2025, down -1% year-on-year amid currency headwinds but rising +2.1% at constant exchange rates.

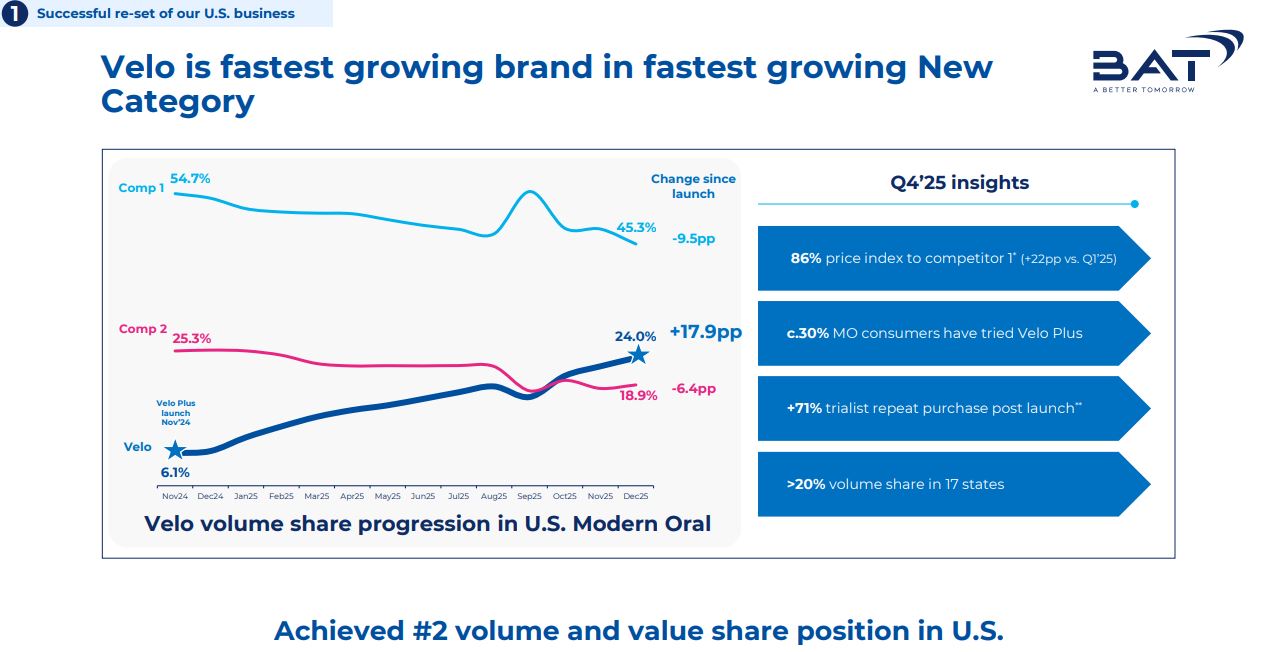

Growth was largely attributable to the company’s US business, which returned to profit growth for the first time since 2022. The performance was largely fuelled by sustained strength in Combustibles, while Modern Oral also soared following the Velo Plus launch, rising +310% to £327 million.

AME was another key growth driver, with its multi-category portfolio delivering strong performance, with reported revenue slightly up +0.7% (+3.3% at constant rates), on the back of sustained momentum across its multi-category portfolio

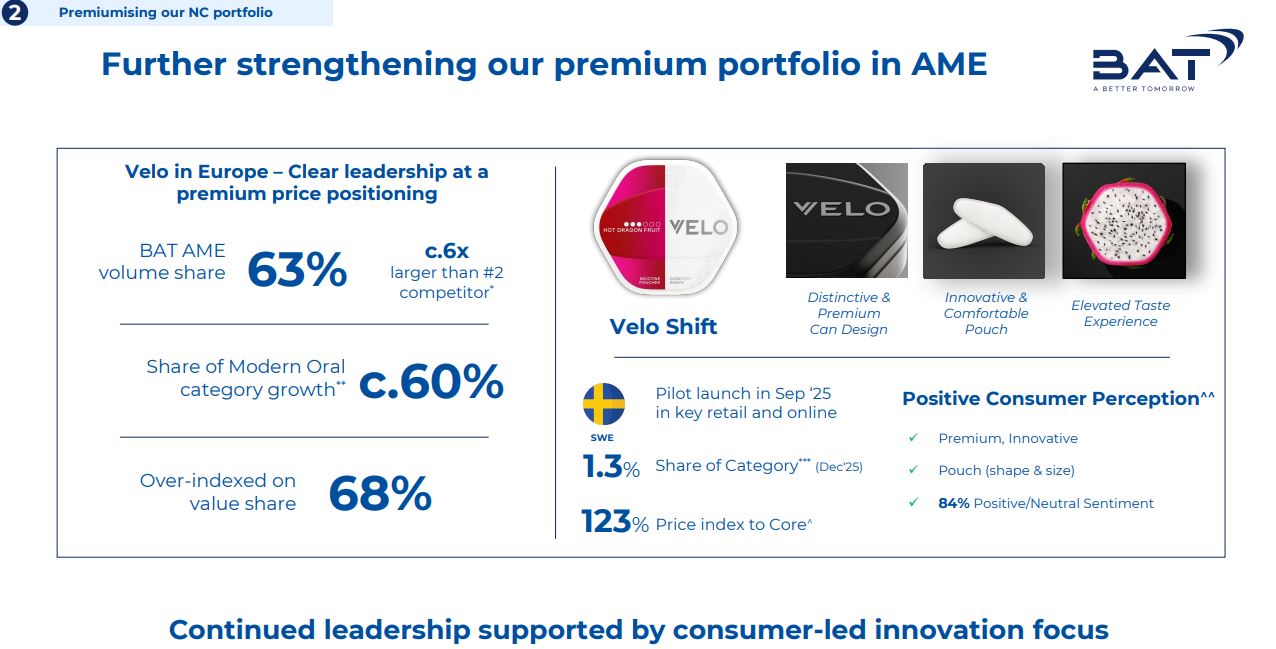

Modern Oral delivered another standout performance, with Velo’s revenue surging +47.4% (+48% at constant rates) and volume rising +47.1%. Growth was driven by established markets across Scandinavia, newer adopters including the UK, Switzerland and Austria, and strong contributions from global travel retail, Pakistan and Japan.

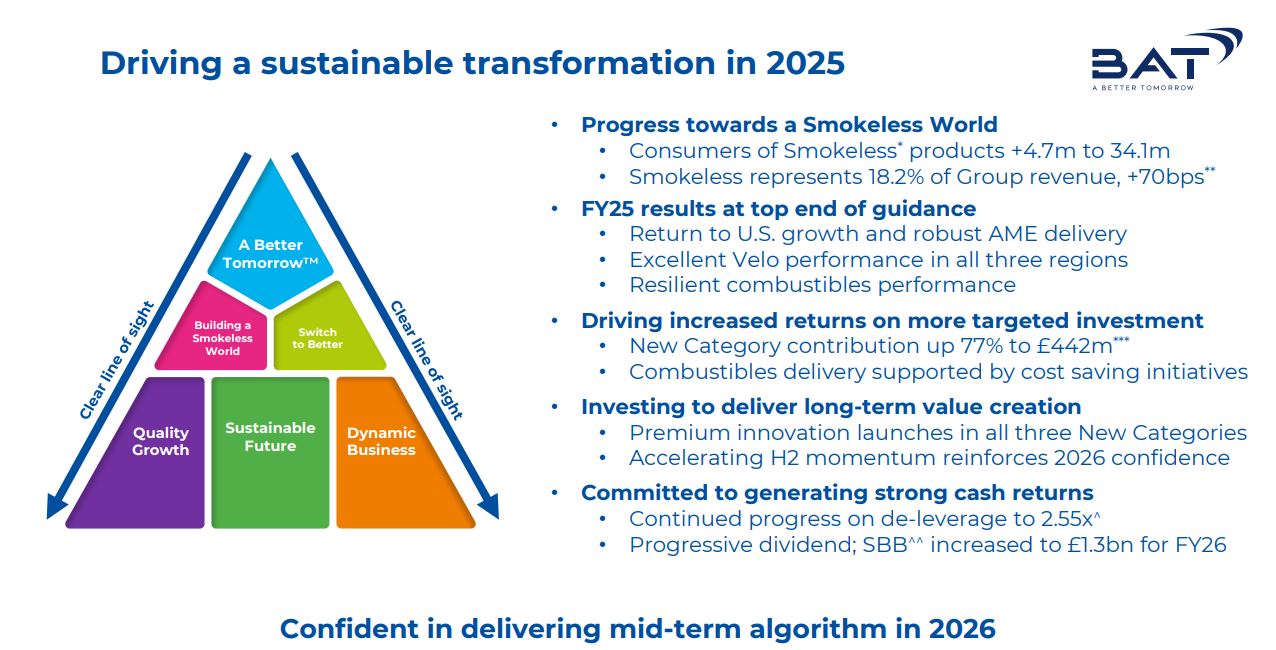

As the group advances towards its ambition of becoming a predominantly smoke-free business by 2035, smokeless products now account for 18.2% of group revenue, an increase of 70 basis points compared to FY24.

New Categories full-year growth was up +7%, accelerating to double digits in the second half, driven by strong Velo growth in all regions. Contribution increased +77.1% to £442 million, reflecting the effectiveness of the company’s Quality Growth strategy.

On an earnings call, BAT Chief Executive Tadeu Marroco said: “We continue to deliver quality growth, with gross profit up over £200 million and category contribution reaching £442 million.

“This reflects our disciplined approach to return-on-investment, targeted investments in high‑value markets, and increasing scale benefits across our portfolio.

“I’m proud of the progress we’re making, and I am particularly pleased with our accelerated H2 momentum, where we returned to double‑digit New Category revenue growth.”

Reported operating profit increased +265% year-on-year, driving a 28.4 percentage point uplift in operating margin to 39%, primarily due to changes in the Canadian settlement provision. Adjusted operating profit grew +2.3%, with adjusted margin steady at 44%.

Performance by region

Performance in the USA reflected continued strategic momentum across the portfolio, with reported revenue up +2.3% year-on-year (+5.5% at constant currency).

Modern Oral recorded the largest revenue, up sharply +297% (+310% at constant rates) as Velo Plus drove category volume share up 11.6 percentage points to 18%.

Vuse maintained its leadership in value share, despite a -6.4% revenue decline (-3.4% at constant rates), reflecting ongoing pressure from illicit single-use vapour products.

In combustibles, revenue increased +1.4% (+4.6% at constant rates), as favourable price/mix (including the excise duty drawback) offset a -7.7% drop in volume. Volume share declined 10 basis points, while value share rose 30 basis points.

Smokeless products now contribute 19.6% of total US revenue.

The Americas and Europe (AME) region reported modest growth, with revenue up +0.7% (3.3% at constant exchange rates).

The performance was driven by New Category growth of +4.8% (4.3% constant rates) and resilient combustibles performance, where constant-currency revenue rose +2.3% on strong price/mix.

Combustibles volume share increased 10 basis points, while value share declined 70 basis points.

Smokeless products now account for 19.9% of regional revenue.

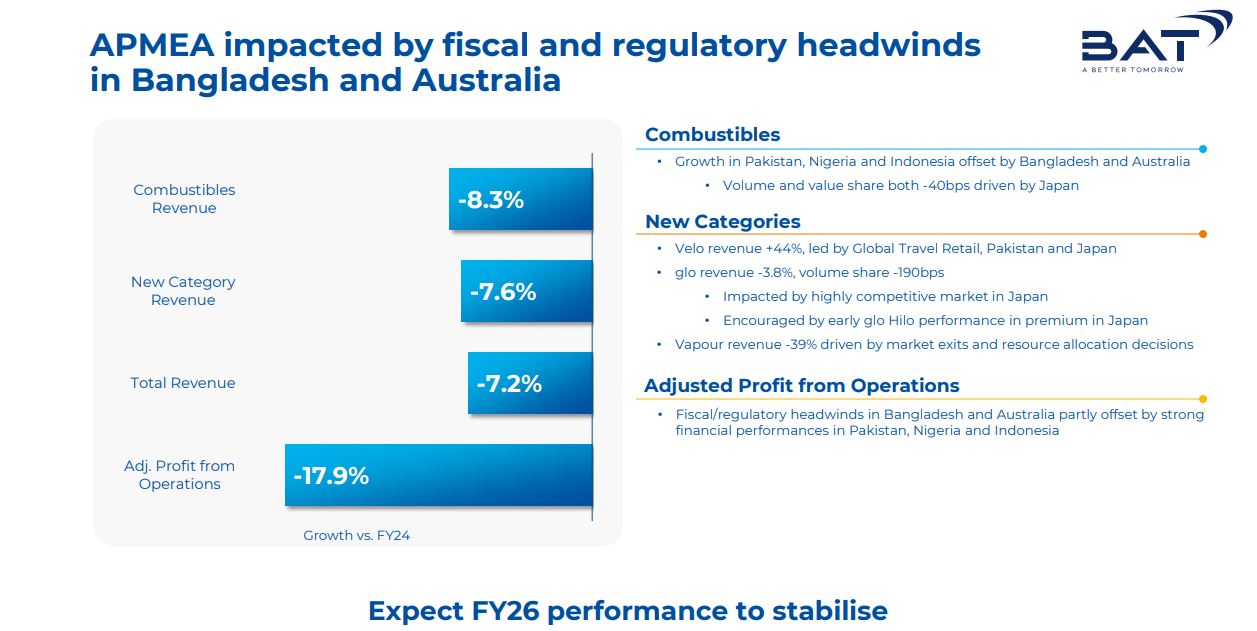

Performance in APMEA reflected the impact of significant regulatory and fiscal challenges, with reported revenue down -10.9% (7.2% at constant rates).

Market-specific pressures in Australia and Bangladesh led to substantial headwinds, affecting both volume and financial results.

In combustibles, value share and volume share each slid by 40 basis points.

New Category performance softened, with revenue down -10.6% (-7.6% at constant rates), largely due to weaker heated product trends in Japan and South Korea.

Smokeless products maintained a presence in the regional mix, representing 11.7% of total revenue.

Performance by category

In 2025, Modern Oral continued to drive strong growth, with Velo Plus revenue reaching £3,234 million, up +47.4% (+48.0% at constant rates).

Travel retail contributed strongly to this momentum, alongside the US national roll-out, where revenue surged +297% (310% constant FX), lifting category volume share to 18% and value share to 13.1%. AME markets also saw robust growth, particularly in Scandinavia, the UK and Switzerland.

Heated Products’ (glo) revenue was down -0.7% (+1.0% constant rates) as competitive pressures and resource allocation ahead of glo Hilo launches impacted volumes.

AME revenue grew +6.2% (+6.2%) at constant rates, while APMEA declined -7%, partially offset by Kazakhstan, with momentum building ahead of the glo Hilo roll-out in key profit pools.

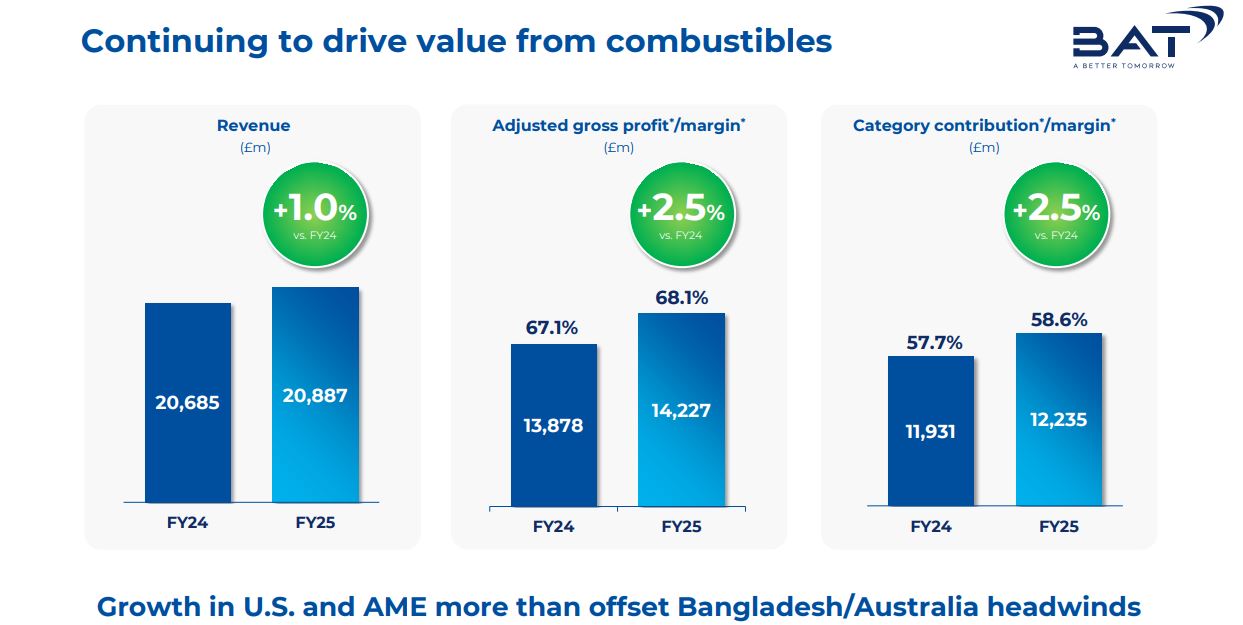

Combustibles revenue totalled £20,201 million, down -2.3% (+1.0% at constant rates), with US revenue rising +4.6% at constant rates driven by price/mix, AME up +2.3%, and APMEA down -8.3%. Group cigarette volume fell -7.9%.

Traditional Oral revenue stood at £1,043 million, down -4.5% (-1.7% constant rates) with volumes falling -9.1% to 5.5 billion sticks. In the USA, revenue fell -5% as volumes declined -8.9%, impacted by the shift to Modern Oral, while value and volume share each dropped 40 basis points. Outside the USA, revenue grew +9.9% +(5.1% constant rates), as pricing offset a -10.3% volume decline.

Looking ahead, Marroco said: “I am confident that we will sustainably deliver our mid-term algorithm, as we are firmly committed to growing revenue sustainably and improving profitability.”

“We are carrying momentum into 2026, underpinned by a robust innovation pipeline, strong strategic partnerships and confidence in our future fit capabilities. We are executing with discipline and delivering against our priorities.

“At the same time, we are enhancing financial flexibility, enabling continued investment in our transformation together with strong cash returns. I am excited about the future for BAT and believe we are well-positioned to deliver long-term, sustainable growth and value for all our stakeholders.” ✈