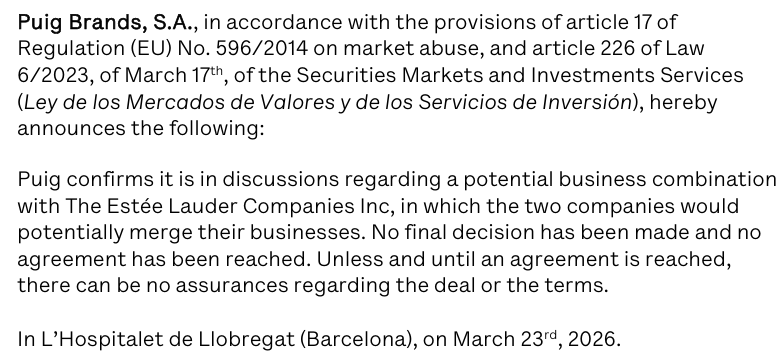

US beauty products powerhouse The Estée Lauder Companies (ELC) yesterday (23 March) confirmed it is in discussions regarding a potential business combination with Spanish fragrances to fashion house Puig, in which the two companies would potentially merge their businesses.

“No final decision has been made, and no agreement has been reached,” ELC said in a statement precisely mirrored by its Spanish counterpart (see below).

“Unless and until an agreement is signed between the companies, there can be no assurances regarding the deal or its terms,” ELC said.

A merger would create a US$40 billion beauty giant, according to Financial Times.

Any deal would have major ramifications for travel retail. The Estée Lauder Companies already offers a star-studded beauty portfolio in the channel, including Estée Lauder, Clinique, Bobbi Brown, Jo Malone London, La Mer, M·A·C, Tom Ford and Aveda.

Barcelona-based Puig, founded in 1914 and still controlled by the Puig family, also boasts an alluring beauty line-up, including Byredo, Carolina Herrera, Charlotte Tilbury (majority share), Nina Ricci, Penhaligon’s and Rabanne.

The group generated revenue of €5,042 million in 2025, up +7.8% like-for-like and adjusted EBITDA of €1,045 million, a +7.8% increase. ✈

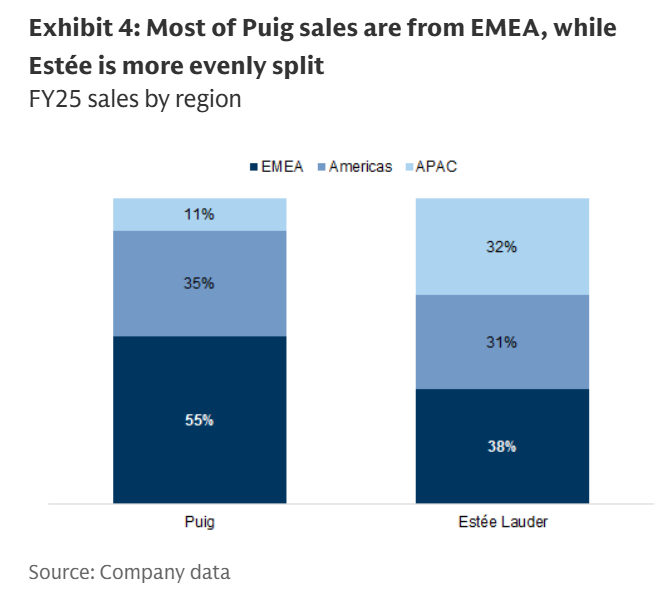

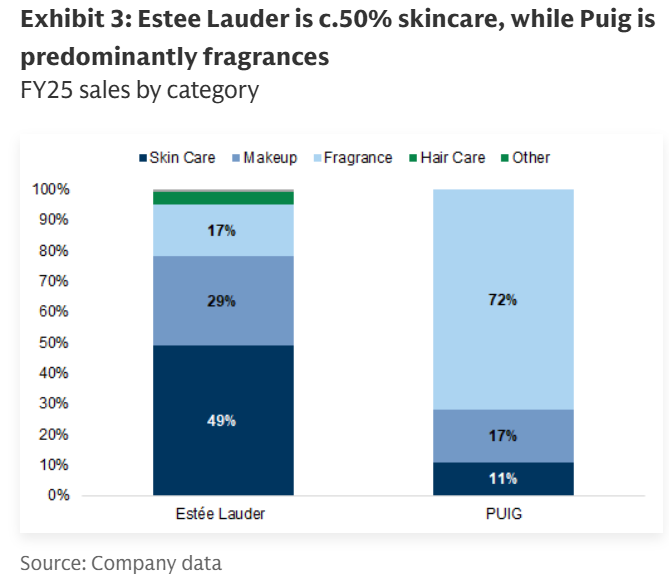

Two family houses offer complimentary strengthsIn a note, Goldman Sachs Research described the potential coming together of two powerful family-owned groups, with the Puig family currently maintaining 93% control of the Spanish company, while the Lauder family holds 82% of ELC voting rights. Puig is a global prestige beauty company, skewed to premium fragrances, with €5 billion of sales and €0.8 billion of EBIT in 2025, implying a 16.1% operating margin vs. ELC at €12.3 billion of sales and €0.95 billion of EBIT in 2025, or an 8.0% operating margin, Goldman Sachs observed. “A potential combination would create the #2 global fragrance player, with 15% combined market share (vs. 16% for L’Oréal, which is #1 in the category),” Goldman Sachs said. “Estée Lauder’s revenue mix is skewed to skincare, which represents 49% of its sales (vs. 11% for Puig), followed by makeup at 29% (vs. 17%) and fragrances at 17% (vs. 72%).”

|