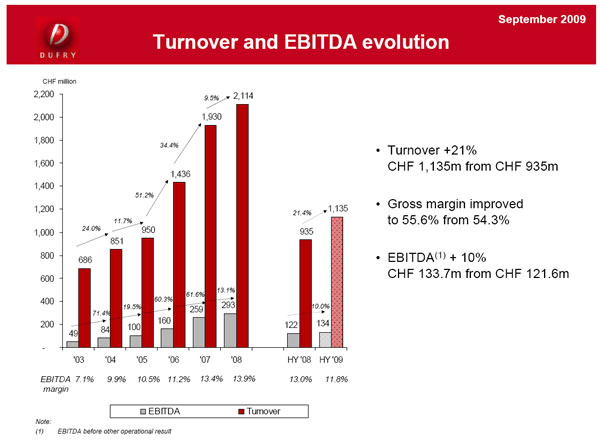

SWITZERLAND. Cash generation and a related reduction in debt were key themes as Dufry this morning posted a +10% rise in first-half EBITDA on sales that rose +21.4% to CHF1,135.1 million (US$1063.9 million) but in organic terms fell by -16.3%. [We’ll update this story throughout the morning with more comment, plus company and investor reaction – Ed].

|

“Visibility remains very limited,” Dufry noted in a cautious assessment of a future clouded by the lingering financial crisis and the impact of the H1N1 flu virus.

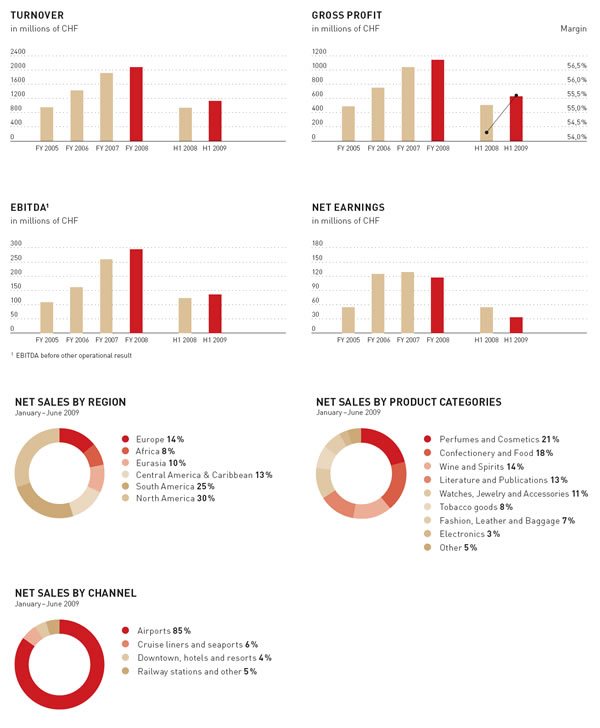

EBITDA (before other operational result) reached CHF133.7 million (US$114 million) compared to CHF121.6 million for the same period in 2008.

|

Click here to view the enlarged image (then hover over graphs with your cursor and click for full detail) |

Dufry said that the negative impact of the current economic environment on passenger numbers together with some specific effects, such as the H1N1 flu virus in Mexico, had driven the -16.3% organic decline.

The foreign exchange translation effect added 2.2 percentage points, while the consolidation of the Hudson Group acquisition together with new projects contributed 35.5%.

Gross profit reached CHF631.5 million (US$581.9 million) for the first half, an increase of +24.4% year-on-year.

|

Click here to view the enlarged image (then hover over graphs with your cursor and click for full detail) [Source: Dufry] |

Importantly, gross margin improved by 1.3 percentage points to 55.6% in the first half of 2009 from 54.3% in the first half of 2008. That increase, Dufry said, is the result of various initiatives it has carried out in past years and was mainly generated in the first quarter of 2009.

Even so, the company was able to improve the gross margin in the second quarter as well, in line with the targets defined in its efficiency plan, it said.

|  |

Source: Dufry | |

The EBITDA margin was 11.8% compared to 13.0% for the relevant period in 2008 and was impacted by the consolidation of Hudson Group due to the different seasonality in that company’s cost structure.

However, thanks to its efficiency plan, Dufry reduced its overall fixed cost base by CHF27 million (US$25.3 million) allowing it to partially mitigate the impact of the sales reduction on profitability.

Dufry noted that it has a distinct seasonality with the second half being more important in terms of sales. It said that due to the fixed cost element, the seasonality factor is even more pronounced at EBITDA level.

EBIT in the first six month of 2009 reached CHF65.6 (US$61.5 million) compared to CHF78.8 million in the respective period of 2008. Financial expenses increased by CHF17.8 million to CHF23.9 million in the first six months of 2009, due to increased interest expenses resulting from higher debt charges assumed following the Hudson acquisition. This was partially compensated by lower interest rates levels in the market.

Net earnings for the Group stood at CHF33.4 million in the first half of 2009 compared to CHF55.5 million in the same period of 2008.

Excluding minority interests, net earnings to equity holders in the first half of 2009 were CHF10.4 million compared to CHF 28.0 million in the respective period of 2008.

|

Click here to view the enlarged image (then hover over graphs with your cursor and click for full detail) [Source: Dufry] |

|

Click here to view the enlarged image (then hover over graphs with your cursor and click for full detail) [Source: Dufry] |

CASH GENERATION, DEBT REDUCTION CRITICAL

The focus on cash generation has been one of the key themes for 2009, the company said.

Dufry reduced net debt by CHF101.7 million (US$95.3 million) in the first half of 2009. This compares to an increase in net debt of CHF11.2 million in the same period of 2008, excluding the investment in Hudson in the respective period.

|

Source: Dufry |

As of June 30, 2009, net debt amounted to CHF722.5 (US$677.2 million) compared to CHF824.2 million at December 31, 2008 and CHF942.6 million at October 31, 2008, just after the closing of the Hudson transaction.

|

“We have been able to demonstrate that Dufry can adjust quickly to the challenges and the new circumstances. With the implementation of the efficiency plan, we have been able to safeguard our profitability and to drive cash generation“ |

Julián Díaz Chief Executive Officer Dufry Group |

Dufry said: “The strong cash flow generation was due to the improvements in net working capital, contained capital expenditure as well as a cost reduction programme, all of which have been implemented as part of the efficiency plan.

“With adjusted EBITDA/Net Debt at 2.9x, Dufry was well below the respective debt threshold of 3.5x. As for interest expense/adjusted EBITDA, the headroom was even bigger with the ratio being 6.1x, 53% above the threshold of 4.0x.”

Putting Dufry’s results into the perspective of a challenging first-half environment when both passenger numbers and spending power declined globally on the back of the global recession, the group claimed to have delivered a “solid performance”.

Thanks to its efficiency plan, which was introduced rapidly at the end of 2008, the company was able to reduce fixed costs across the board and to deliver an EBITDA margin of 11.8% in the first half of 2009, it emphasised.

Going forward, Dufry said, “visibility remains very limited”. In the past six months, international passenger numbers seem to have stabilized at about -8% below last year’s levels, and forecasts indicate a gradual improvement going forward.

Dufry Group Chief Executive Officer Julián Díaz commented: “We have been very demanding on our business during the first six months of the year given such an exigent and difficult environment.

“We have been able to demonstrate that Dufry can adjust quickly to the challenges and the new circumstances. With the implementation of the efficiency plan, we have been able to safeguard our profitability and to drive cash generation.

“Equally, the Hudson business has proven resilient despite the fact that it was also impacted by the recession. The integration and the business development have started to generate synergies and this has further supported Hudson’s performance.

“As such, the transaction has met our expectations and we will continue to realize the potential Hudson has contributed to our group. Last but not least, we have continued to develop our concession portfolio and we have more than 10,000sq m of retail space, which we will open throughout 2009.

“Looking beyond 2009, our growth strategy remains unchanged and a significant number of interesting opportunities are coming to the market. We will assess them carefully and some of them might materialize. We believe that the consolidation in our industry will continue in the longer term and Dufry will remain at the forefront as one of the leading operators.”

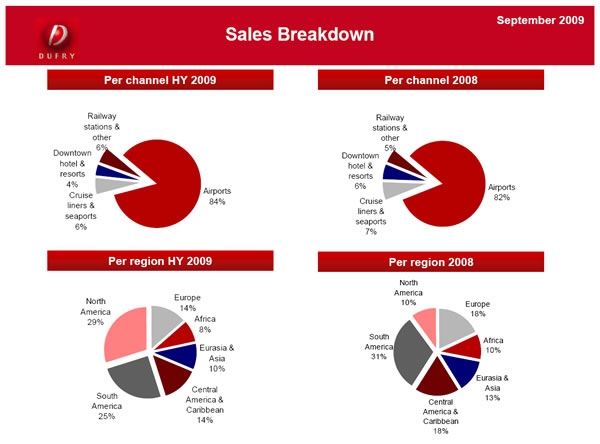

DEVELOPMENT BY REGION

Turnover of Region Europe decreased by -19.4% to CHF 160.6 million (US$150.5 million). Dufry said that the more pronounced decrease in Italy compared to the rest of the region – driven mainly by Alitalia’s flight reallocation in the second quarter last year – will “peter out” in the second half of 2009. However, all operations performed below last year levels, it cautioned.

Region Africa’s turnover eased slightly when measured in local currencies. After translation into Swiss Frances, Africa’s turnover decreased by -5.4% to CHF87.6 million (US$82.1 million) compared to CHF92.6 million last year. Whereas Tunisia posted a modest decrease, Morocco and most other locations achieved single-digit growth, the group said. Egypt performed “particularly well” and posted double-digit growth.

Region Eurasia’s turnover fell by -13.0% year-on-year to CHF109.0 million (US$102.2 million). Some Russian operations experienced a strong decrease in sales as did the operations in South East Asia. This was partially balanced by the growth in Sharjah as well as selected Russian operations.

[Note: Following the acquisition of Hudson, Dufry proceeded with a regrouping of its operations in North America and the Caribbean in order to reflect the geographical presence of the Group more accurately. The new regions formed are presented below along with the respective comparison of the previous year’s figures.]

|

Source: Dufry |

Turnover of Region Central America & Caribbean which comprises all the business of the former Region North America & Caribbean except the US business, decreased by -8.8% to CHF150.5 million (US$141.1 million). The Mexican operations were negatively affected by H1N1 while the Caribbean business also saw a decrease as passengers reduced discretionary spending on larger tickets, notably watches and jewellery. Cruise lines attracted a higher proportion of customers with a lower purchasing power on average, Dufry said

In the newly formed Region North America which comprises Hudson as well as Dufry’s original US business, turnover reached CHF343.5 million (US$322 million) in the first half of 2008 due to the consolidation of Hudson. “On a pro forma comparison, Hudson’s business model has proven to be resilient, even if it also suffered a decrease in passenger numbers in the US,” Dufry said.

Region South America decreased by -8.4% to CHF284.0 million (US$266.2 million). “The global economic crisis continued to weigh on the performance of the South American operations as well,” Dufry noted.

|

The ACI Airport Business & Trinity Forum, Macau, China, 23-25 September |

MORE STORIES ON DUFRY

Dufry captures fashion concessions at Nice Airport T2 – 31/07/09

Hudson opens first Victoria’s Secret US airport store – 28/07/09

[comments]