|

“The overall scenario for the industry continues to be positive despite some complex geopolitical situations and increased FX volatility in selected markets.“ |

Julián Díaz CEO Dufry |

INTERNATIONAL. Dufry Group’s turnover climbed by +9% year-on-year in the first nine months of 2014 (+12.4% at constant exchange rates) to CHF2,930.9 million (US$3 billion). The increase came through a combination of organic growth and the consolidation of The Nuance Group since September 2014.

EBITDA rose by +7.4% (+10.6% at constant rates) to reach CHF414.4 million (US$429 million) for the first nine months, generating an EBITDA margin of 14.1%. Free cash flow grew by +17.2% and reached CHF273.8 million (US$284 million).

CEO Julián Díaz said: “Performance in the third quarter has been in line with our expectations and as we communicated. The geopolitical situations and the currency volatility have weighed on the performance, especially in Russia and Africa. This has been balanced with the performance of the US business which continued to grow strongly and also the ramp-up of Terminal 3 in São Paulo has been very positive. Furthermore, the Latin American operations saw a good development in profitability.

“We successfully concluded the acquisition of the Nuance Group on 9 September, with the financial consolidation starting already in that month. We have also completed the first stage of the integration process, having secured the financial and operational control of the operations and we have since started a detailed analysis in the different areas as a basis for a detailed action plan to generate the expected synergies.

“The integration opens the doors for efficiency gains for both Dufry and Nuance, and we are confident that the targeted CHF70 million of synergies will be fully reflected in the financials until the end of 2016, with part of the results already being shown in 2015. The process is very complex, as it is the largest acquisition Dufry has ever done and it will require all our attention and energy. Having said this, we are confident that the project teams for this integration consisting of Dufry, Nuance and PwC executives are up to the challenge and we will manage a successful integration.

“In terms of outlook, we do not expect the trends to materially change in the short term and the overall scenario for the industry continues to be positive despite some complex geopolitical situations and increased FX volatility in selected markets. International passenger numbers, the leading indicator for our business, are expected to grow +5.1% in 2014 and +5.8% in 2015. On the macroeconomic environment, we expect to continue seeing some divergence in the regional development. Our diversified concession portfolio, which has been further strengthened with the Nuance acquisition, will support the development of the group, as will our flexible cost structure, which allows adapting quickly in situations of passenger traffic changes.

“2014 has been so far a year of many challenges and great achievements. Having executed well in many of the projects, we now focus our efforts in the integration and generation of synergies in the Nuance acquisition.”

Turnover

Organic growth in the third quarter was +4.3% resulting in an organic growth for the nine months of +3.9%, based on a contribution of 2.0% from like-for-like growth and 1.9% from new concessions, net. Acquisitions added 8.5% to the turnover growth year-to-date. The translation impact to the Swiss Franc was negative in 3.4%, which results in a reported growth of 9.0% for the first nine months of 2014.

Turnover in Region EMEA & Asia grew by +7.2% in constant exchange rates and reached CHF941.2 million in the first nine months of 2014 versus CHF894.9 million in the previous year. The region benefited from the consolidation of Hellenic Duty Free Shops, acquired in April 2013. In the third quarter organic growth for the region was stable.

• In Europe, France, Italy, and Switzerland continued to show good performances, said Dufry. In Greece, performance in the third quarter remained unchanged when compared to the second quarter. After a record year in 2013, the Greek business continued to be impacted by a lower number of Russian and Turkish passengers as well as the volatility of the Russian and Turkish currencies.

• In Eastern Europe, Serbia and Armenia continued to delivery good results, while in Russia, the Russian Rouble and the political situation in the Ukraine continue to impact the business.

• Performance in Africa continued to be challenging due to the political situation in several countries in the region. Almost all operations in the region had softer performance, whereby Egypt and Tunisia continued to be most affected.

• In Middle East and Asia, existing operations performed well, and the new openings in China, Indonesia, Kazakhstan, South Korea and Sri Lanka contributed to the results as expected.

|

|

Turnover in Region America I stood flat at constant rates and reached CHF546.2 million in the first nine months of 2014 versus CHF569.6 million in the same period in 2013. Mexico continued to perform well and operations in the British Caribbean accelerated organic growth. Businesses in Argentina and Uruguay performed in line with the first half of the year.

Turnover in Region America II reached at CHF511.3 million in the first nine months of 2014 compared to CHF519.8 million in the same period in 2013. In the third quarter, turnover growth at constant rates continued to accelerate to +7%, compared to -9% and 4% in the first and second quarters. At Guarulhos International airport in São Paulo, traffic at Terminal 3 has been ramped up significantly with about 75% of international flights, from October, being operated through Terminal 3 and 25% through Terminal 2.

Turnover in Region United States & Canada surged by +13.0% at constant FX rates. In Swiss Franc terms, turnover came to CHF713.6 million in the first nine months of 2014 from CHF659.0 million in the same period in 2013. This is the fourth consecutive quarter of double digit turnover growth in the region. The strong performance, said Dufry, continues to be a result of a steady increase in passenger numbers and increase in spend per passenger. Additionally, Dufry has been active in the expansion of the Hudson franchise, as well as diversifying into other concepts like duty free shops, brand boutiques and specialised shops, the group noted.

|

Nuance generated a consolidated turnover of CHF177.7 million in September 2014, which means a flat performance compared to the same period last year. Good growth in the US and Canada combined with the opening of new retail space was compensated with a softer performance in Turkey and Russia on the back of fewer Russian passengers and the weaker Russian Rouble.

|

|

|

|

Gross profit grew by +9.3% and reached CHF1,725.8 million in the first nine months of 2014. Gross profit margin expanded by 20 basis points to 58.9% from 58.7% in the respective period. In like-for-like retail operations, gross profit margin improved by 30 basis points, which excludes the effects of the acquisition in Greece and Nuance. The improvement is mainly a result of the internal procurement organisation and the centralisation of the supply chain, said Dufry.

Selling expenses reached CHF703.1 million in the year to September, compared to CHF619.4 million in the first nine months of 2013. As a percentage of turnover selling expenses went to 24.0% from 23.0% in 2013. The increase was mainly a result of the consolidation of Nuance, which has higher concession fees on average.

As noted, EBITDA at constant FX rates grew by +10.6%. In Swiss Francs it increased by +7.4% with EBITDA margin reaching 14.1% in the period. Excluding the consolidation impact from Nuance, EBITDA margin would have improved 10 basis points to 14.5% compared to 14.4% last year.

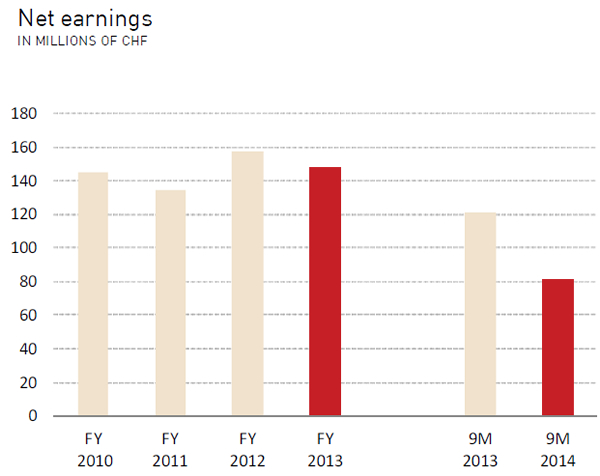

EBIT stood at CHF208.5 million in the year to September from CHF218.4 million one year earlier. Pro forma net earnings attributable to equity holders, which exclude non-recurring transaction and financing cost of Nuance, stood at CHF91.1 million for the first nine months 2014. Reported net earnings to equity holders for the year to September reached CHF55.5 million versus CHF73.0 million in 2013. Net earnings for the first nine months of 2014 reached CHF81.0 million versus CHF121.5 million in the same period of 2013.

Cash flow generated from operations grew by +21.8% and reached CHF444.8 million in the first nine months. Free cash flow also grew and reached CHF273.8 million, +17.2% higher than the respective period in 2013. In the year to September, Capital Expenditure stood at CHF132.9 million compared to CHF113.0 million in the first nine months of 2013 and is mainly a consequence of several projects in Brazil, USA and Asia.

Net debt at the end of September 2014, was CHF2,181.3 million compared to the CHF1,753.3 million at the end of December 2013. The main covenant at group level, Net Debt/adjusted EBITDA, stood at 3.27x as of 30 September 2014.

|

Nuance transaction

As noted, Dufry concluded the acquisition of Nuance on 9 September and has started to consolidate the business since then.

Dufry has already launched the integration process and taken financial and operational control of the business. It said it was now focusing on analysis of different business aspects, aiming to define the future operating model and prepare a detailed action plan to generate synergies. Dufry expects to conclude this phase during the first quarter of 2015.

In terms of synergies, the expected CHF70 million will start to materialise in 2015, with the full impact to be reached by 2016. Dufry expects to see an improvement in the gross margin through increased purchasing power and the integration of Nuance’s purchasing into its supply chain and logistics platform. Also, Dufry expects that the combination of the global and regional organisations, as well as global support functions, will create added value.

|