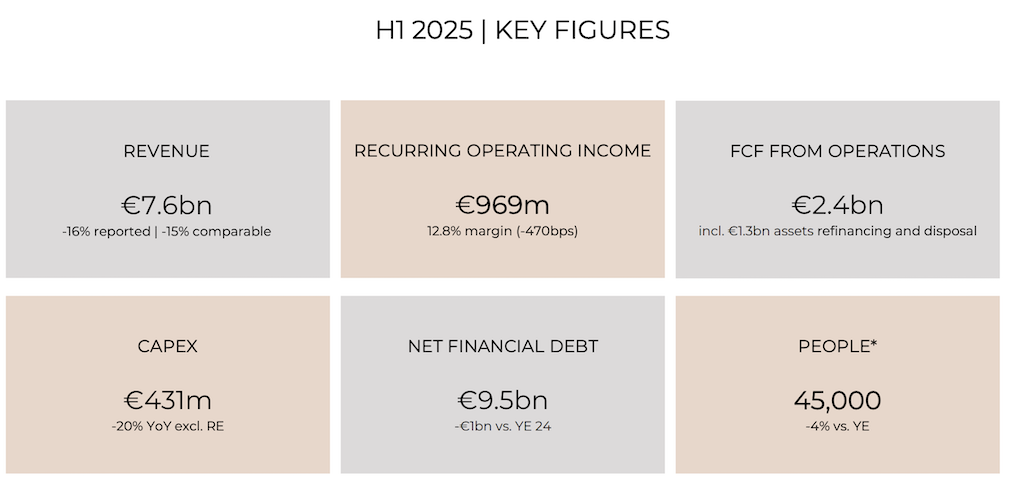

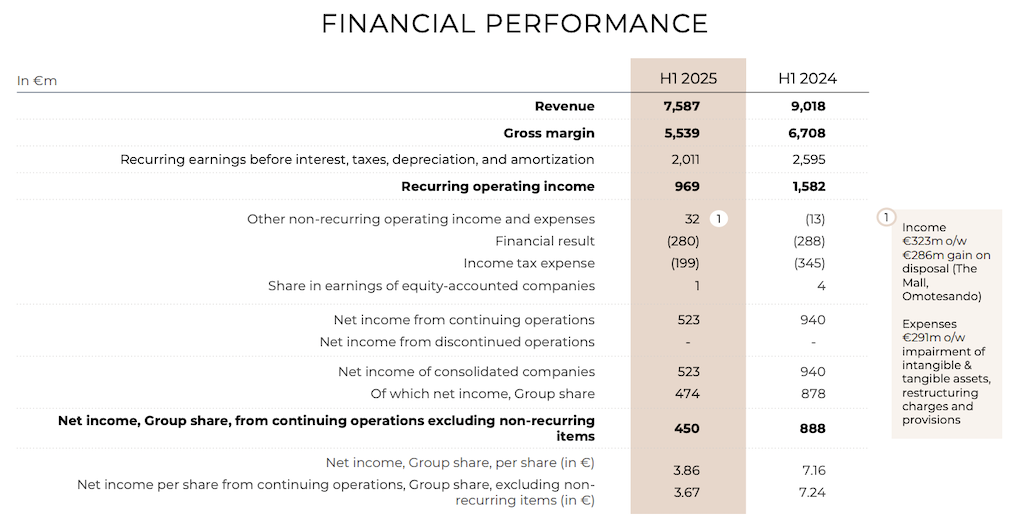

Luxury group Kering has posted a -16% decline in reported revenues (-15% comparable) for the first half ended 30 June, reflecting continued headwinds across its luxury brand portfolio.

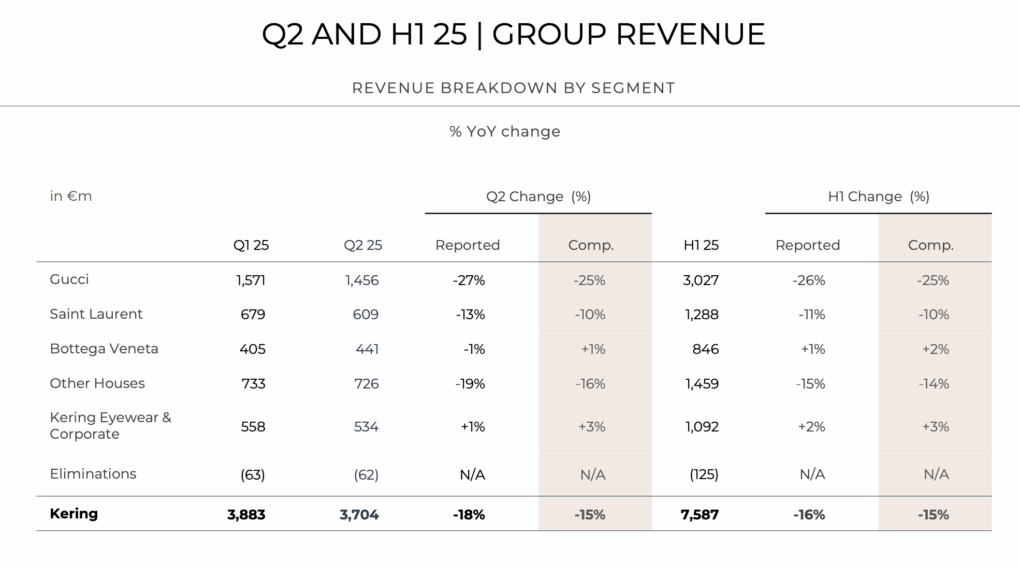

Second-quarter revenue was €3.7 billion, an -18% decrease as reported and -15% on a comparable basis, with adverse currency effects accounting for a -3% impact.

The contraction in Q2 and H1 is attributed to continued weak footfall in directly operated stores and a sustained decline in tourist activity – both within the Asia Pacific region and from long-haul travellers to Western Europe.

Kering reported recurring operating income of €969 million for the first half of 2025, representing a -39% year-on-year decrease.

The Group’s recurring operating margin contracted by 470 basis points year-on-year to 12.8% due to negative operational leverage. Gross margin was €5.54 billion, down -17% compared to the first half of 2024. Net income attributable to the Group (excluding non-recurring items) was €450 million.

Kering Group Chairman and CEO François-Henri Pinault commented, “The first half of 2025 has been a period of momentous decisions for Kering. On the governance front, I recommended to the Board of Directors, which has agreed, that we entrust the role of Kering CEO to Luca de Meo, while I will retain the chairmanship.

“On the creative front, reinforced teams, headed by new designers at three of our largest houses, are hard at work, with passion and determination, intensifying the desirability and drawing on the heritage of all our brands.

“On the operational and financial fronts, in a particularly tough market environment, we continued to streamline our distribution and cost base and, executing on our roadmap, we took decisive steps to strengthen our financial structure.

“Though the numbers we are reporting remain well below our potential, we are certain that our comprehensive efforts of the past two years have set healthy foundations for the next stages in Kering’s development.”

All change for Kering The first half of 2025 marked a period of leadership transition across Kering and its houses. At Group level, Kering’s Board of Directors approved the appointment of Luca de Meo as Chief Executive Officer in June. The move introduced a separation of powers at the highest level of governance, with François-Henri Pinault remaining as Chairman. Pending shareholder approval at the General Meeting on 9 September, Luca de Meo will assume the role of CEO on 15 September. Earlier this year, Gucci announced the departure of Sabato De Sarno as Creative Director. This was followed by the appointment of Demna Gvasalia, formerly Artistic Director at Balenciaga, as Gucci’s new Artistic Director. His tenure officially began on 10 July, signalling a new creative chapter for the Italian fashion house. Balenciaga also entered a new era of artistic leadership with the appointment of Pierpaolo Piccioli as Artistic Director. Piccioli, previously at Valentino, brings with him a distinct creative vision that is expected to shape the brand’s evolution in the seasons ahead. |

Regional performance

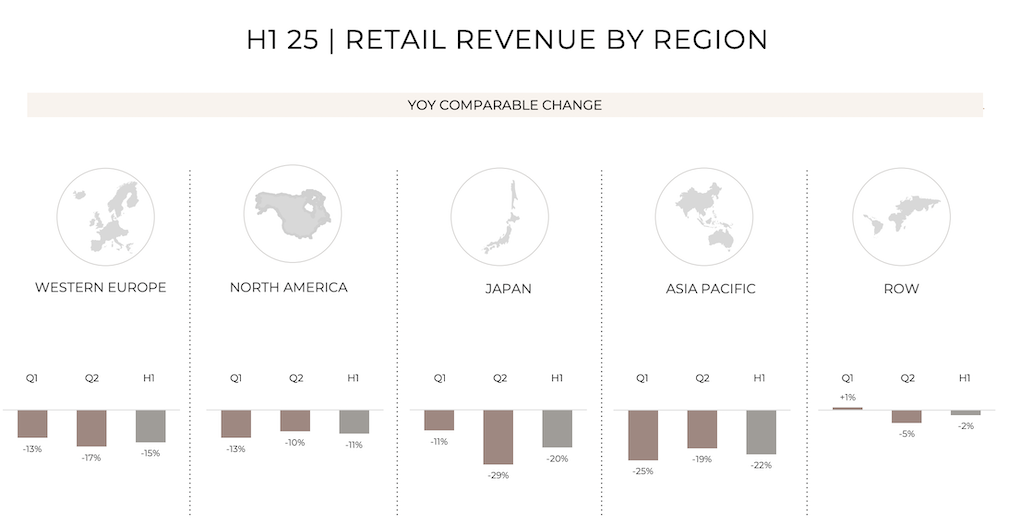

Sales from the directly operated retail network declined -16% on a comparable basis in Q2, consistent with Q1 trends. Regional patterns were mixed. While North America (-10%) and Asia Pacific (-19%) showed comparable improvement compared to Q1, Western Europe (-17%) and Japan (-29%) experienced sharper declines, largely driven by reduced tourist flows. Wholesale and Other revenues fell -12% on a comparable basis.

Western Europe saw revenues fall -15% on a reported and -13% on a comparable basis in the first half. Sales through directly operated stores and ecommerce platforms declined -15%, reflecting lower tourist flows, particularly from Asia, and soft local demand. The recovery in intra-European travel was insufficient to offset this softness.

In North America, sales fell -11% on a reported and -12% on a comparable basis. Store footfall remained subdued, with significant variations in performance by brand and customer segment.

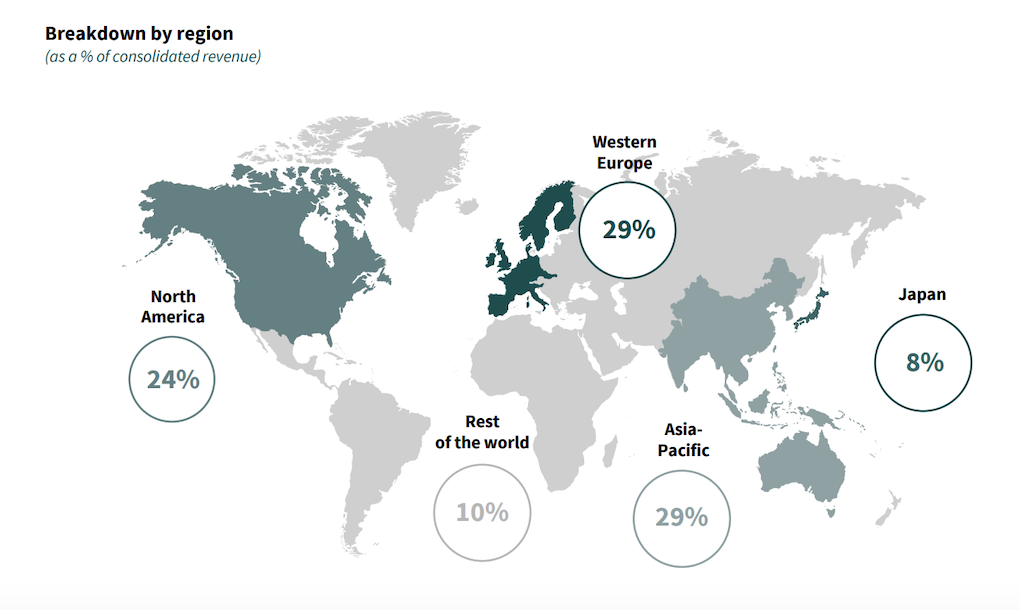

The Asia Pacific region posted a -22% retail revenue decline on a reported and -21% on a comparable basis, with sales down across all major markets. A sluggish recovery in local demand and persistent weakness in store footfall, particularly outside Mainland China, contributed to the downturn. As a result, the region’s share of Group revenue dropped three points to 29%.

Japan experienced a sharp decline, with first-half revenue down -20% on both a reported and comparable basis.

In the Rest of the World, revenue declined -2% as reported and -1% on a comparable basis. While the first quarter was broadly stable, the second quarter saw a slight contraction in sales in the Middle East, contributing to the overall decline.

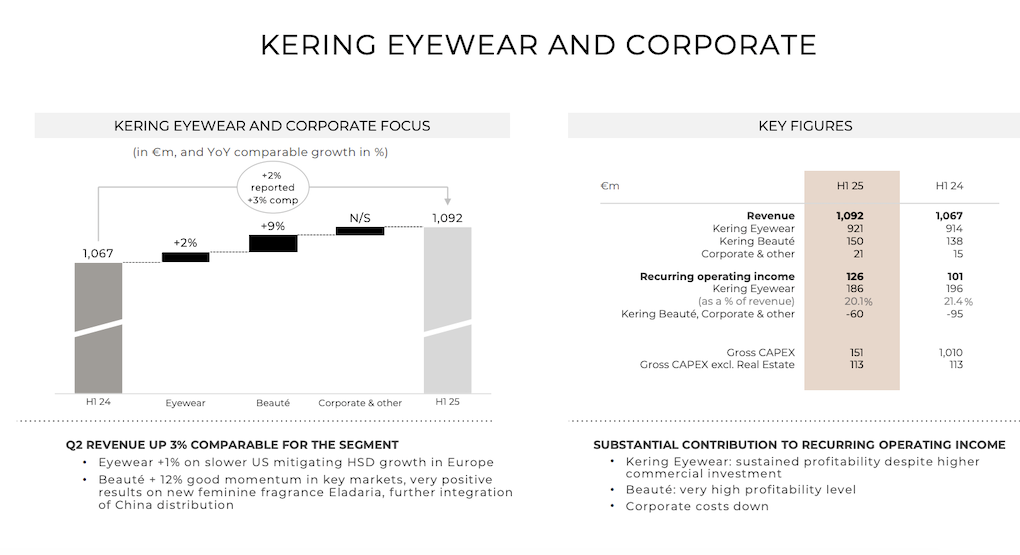

Kering Eyewear and Kering Beauté

Kering Eyewear and Corporate posted revenue of €1.1 billion in H1 2025, up +2% as reported and +3% on a comparable basis. Kering Eyewear accounted for €921 million of this total, up +1% as reported and +2% on a comparable basis. Recurring operating income for Eyewear was €126 million, compared to €196 million in H1 2024.

Kering Beauté, meanwhile, posted revenue of €150 million in H1, up +9% both as reported and on a comparable basis. This was driven by the good performance of Creed and the development of beauty products for the company’s other houses.

Brand performance overview

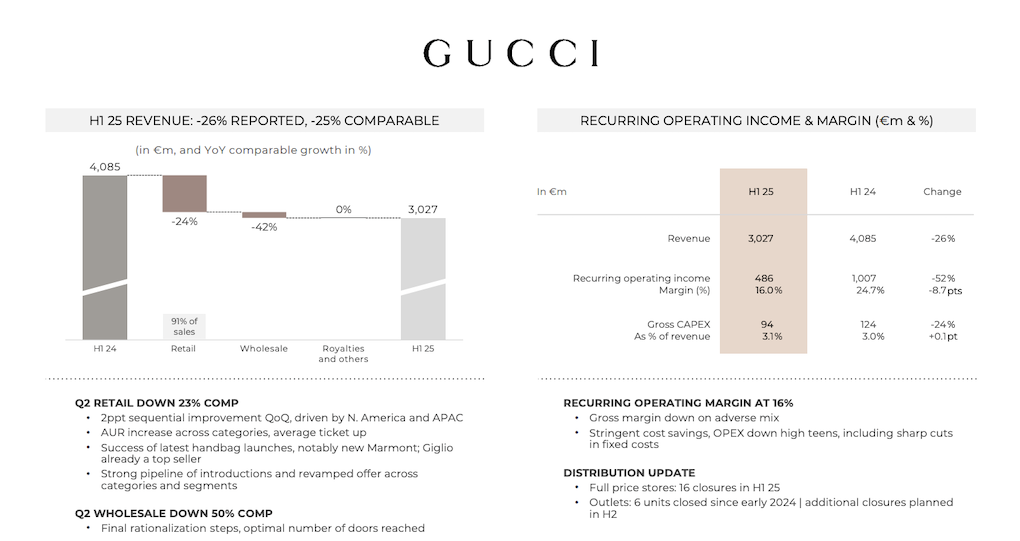

Gucci, the Group’s largest house, reported H1 revenue of €3.03 billion, a drop of -26% as reported and -25% on a comparable basis. Retail sales declined -24%, while wholesale revenue fell -42%. Gucci closed 16 full-priced stores in the first-half.

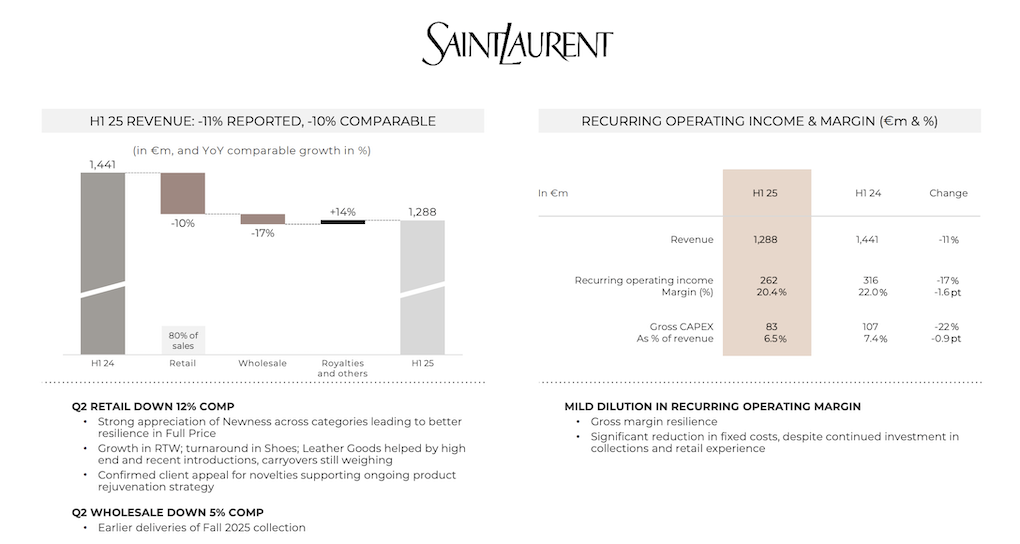

Yves Saint Laurent posted H1 revenue of €1.3 billion, down -11% as reported and -10% on a comparable basis. Direct retail sales fell -10%, while wholesale revenue declined -17%. The brand noted positive reception for new ready-to-wear and footwear ranges.

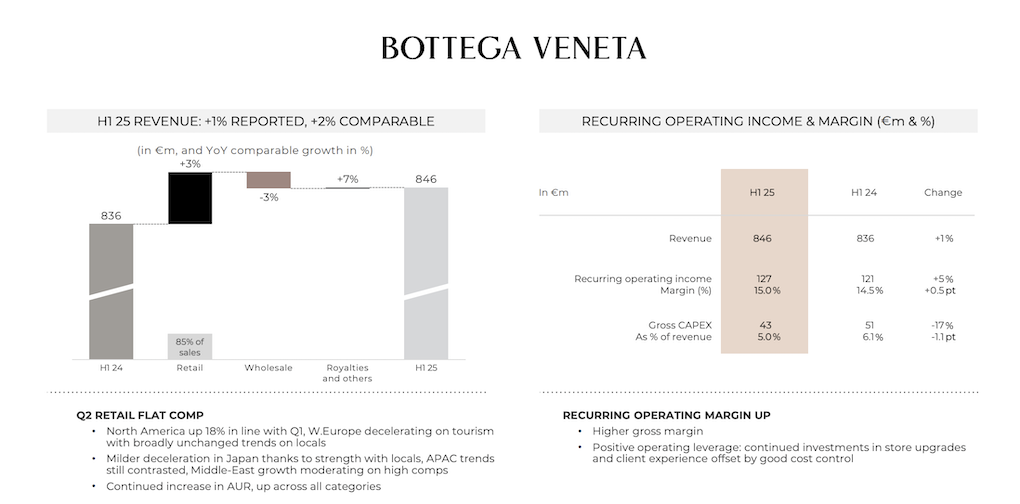

Bottega Veneta delivered a more resilient performance with revenue of €846 million, up +1% as reported and +2% on a comparable basis. Retail sales rose +3%, offsetting a -3% decline in wholesale. Second-quarter retail sales were flat overall but saw growth in North America.

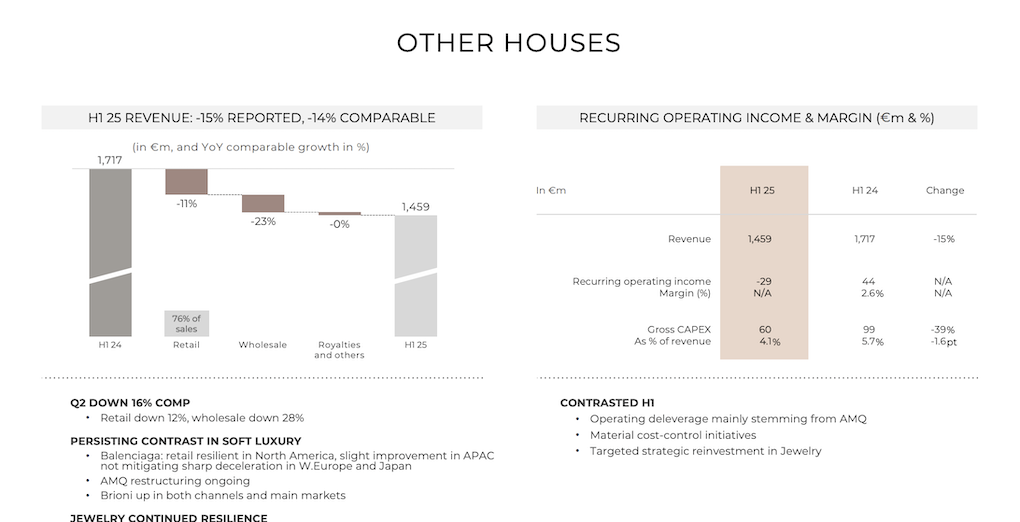

Other Houses, which includes Balenciaga, Alexander McQueen, Brioni and the group’s jewellery brands, generated revenue of €1.5 billion, down -15% as reported and -14% on a comparable basis. Retail sales declined -11% and wholesale revenue fell -23%. Performance was mixed: Balenciaga showed resilience in North America and modest improvement in Asia Pacific, while McQueen’s results were impacted by ongoing store network rationalisation.

Brioni continued to grow in key markets, while the group’s jewellery houses saw solid momentum with strong performances from Qeelin, Boucheron, Dodo and Pomellato.

Outlook

Kering said it remains committed to its long-term strategy of elevating brand equity, reinforcing exclusivity in distribution and balancing creative innovation with heritage. Against a backdrop of macroeconomic and geopolitical uncertainty, the Group reiterated its focus on strengthening operational efficiency and maintaining financial discipline.

The group underlined that key initiatives are being accelerated across the Houses to support future growth, while prioritising selective investment and cost control to protect profitability. ✈