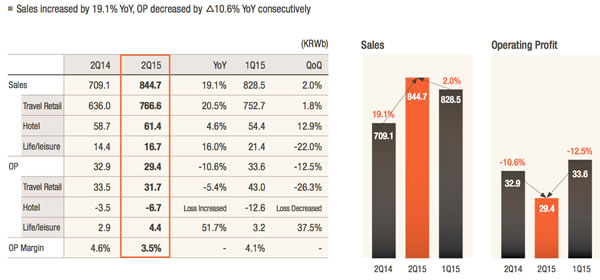

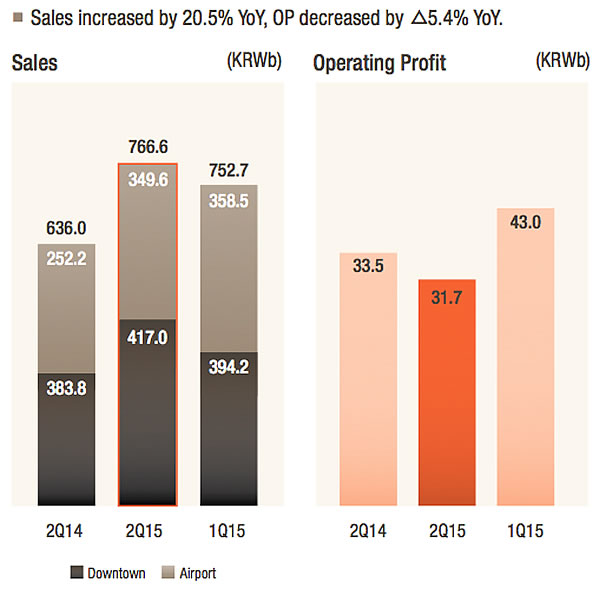

SOUTH KOREA. The Shilla Duty Free posted a +20.5% increase in sales for the second quarter of 2015, however operating profit decreased by -5.4%, mainly due to the MERS health crisis that struck in June.

Sales, including Singapore Changi and Macau, reached KRW766.6 billion (US$ 653.6 million) in the quarter, with KRW417 billion (US$355.8 million) coming from the downtown business and KRW349.6 billion (US$298.3 million) from airports. Operating profit reached KRW31.7 billion (US$27 million).

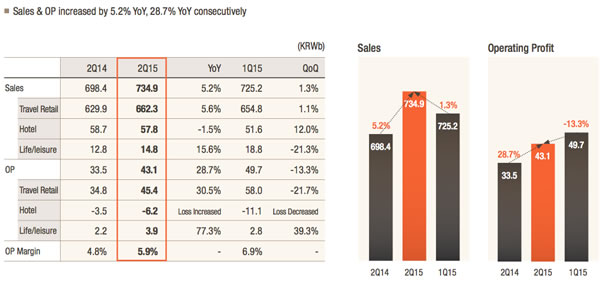

Sales for Korea only climbed +5.6% in the quarter to KRW662.3 billion (US$ 565.1 million) while operating profit shot up by +30.5% to KRW45.4 million (US$38.7 million).

|

Non-consolidated results (South Korea only) show a strong second-quarter performance despite a very difficult June due to MERS; Source: KDB Daewoo Securities Co |

The results underline the heavy costs incurred and difficulties experienced at Shilla’s perfumes & cosmetics concession at Singapore Changi Airport, where it began operations in February 2015. Though the top line has been boosted significantly, Changi accounted for most of the KRW13.7 billion (US$11.7 million) operating loss from overseas activities in the quarter.

Overall though the results will make good reading for Shilla, given the respective challenges in South Korea and Singapore. KDB Daewoo Securities Co Equity Analyst (Cosmetics, Hotel & Leisure, Fashion) Regina Hahm commented: “Due to the MERS effect in June, duty free business revenue recorded +5.6% year-on-year growth, while the company managed to grow on a quarter-on-quarter basis (+1.1%). Favorable performance in the first two months in 2Q seems to have supported the quarterly performance

|

The consolidated results include airport retail operations at Singapore Changi and Macau International, which collectively resulted in a loss of KRW13.7 billion |

|

The consolidated travel retail results show the impact of MERS and Changi on operating profit |

“While the top-line growth of its duty free operations in Korea has been affected by the unexpected external factor [MERS], its profitability continued a year-on-year improvement, posting +30.5% of operating profit growth.

“We have stressed a lot in the past”¦ that Hotel Shilla has shown profitability improvement, mainly originated from GP margin improvement backed by better economies of scale and product mix change. 2Q15 duty free OP margin of 6.9% (similar to our previous estimate of 6.8%) proves that they are well on track to improve margin quality over the long-term going forward.”

On the Changi difficulties, Ms Hahm commented: “Since we are seeing quarter-on-quarter improvement for duty free sales at Changi Airport, we expect to see smaller losses up until the year-end.”

|

Shilla’s debut at Singapore Changi Airport has proved financially and operationally challenging |

|

The Shilla Duty Free’s Incheon International Airport operations (above) and Seoul downtown business (below) drove a +5.6% year-on-year rise in second-quarter revenues and an impressive +30.5% improvement in operating profit |

|