The Moodie Davitt Report introduces the latest feature in The Analyst series, written by The Mercurius Group Founder & President Ivo Favotto*. Here the long-time travel retailer, now Sydney-based consultant, assesses what a forecasted rise in the number of middle class people around the world by 2030 will mean for the travel retail industry.

The Moodie Davitt Report introduces the latest feature in The Analyst series, written by The Mercurius Group Founder & President Ivo Favotto*. Here the long-time travel retailer, now Sydney-based consultant, assesses what a forecasted rise in the number of middle class people around the world by 2030 will mean for the travel retail industry.

The views expressed in this column are not necessarily those of the publisher.

Talk about killer facts – here’s three for you to consider.

First, there are more than three billion people that can be defined as middle class in the world and this group will soon account for more than half the population – the first time in recent human history.

Second, 140 million more people are becoming middle class every year and in five years time, this number will be 170 million (and growing) each and every year.

Third, almost 90% of the growth of the middle class is coming from Asia and almost none of it from the developed world, including Europe and North America.

“If you’re a senior manager in travel retail and you’re not shaping your corporate strategy to this new reality right now, you should be handing back your salary”

If the thought of Donald Trump, Kim Jong-un or global warming causes you to lose faith in humanity, these three killer facts should restore your faith in human endeavour – at no other time in history have so many people been so well off, so we must have done something right.

If ever you were feeling depressed about the state of the travel retail industry and the myriad of challenges we face each day you should stop it, and stop it right now.

If ever there were reasons to rejoice and be glad to be a part of the travel retail industry, it is in these three killer facts. Nothing else happening in our industry right now is even remotely relevant compared to this. And if you’re a senior manager in travel retail and you’re not shaping your corporate strategy to this new reality right now, you should be handing back your salary.

So where do these killer facts come from? They are contained in a new paper, The Unprecedented Expansion of the Global Middle Class by Dr Homi Kharas, Deputy Director in the Global Economy and Development programme at the Brookings Institution. Brookings is a highly respected, Washington D.C.-based not-for-profit organisation dedicated to conducting in-depth research that leads to new ideas for solving problems facing society at the local, national and global level.

Why is this so important to travel retail? Well, travel is what most economists typically refer to as a ‘superior good’. This means it is a good whose consumption rises as a proportion of income the more income rises – particularly as individuals transition from below middle class to middle class to rich. In other words, the more income you have, the more you proportionately spend on travel (more trips, more expenditure). While travel is not unique as a superior good, there aren’t too many of them around.

Sure, travel retail still has a job to do converting growing expenditure on travel into spending in our respective retail channels, but hey – nothing is for free!

Nevertheless, a massive rise in the global middle class means a massive rise in the number of people travelling, which should in turn result in a massive rise in travel retail spend.

And as the only place in our society where relatively rich people congregate on a regular basis, airports, airplanes and cruise ships should be the major beneficiaries. Think about it. Travellers, especially international ones, by definition come from a certain socio-economic stratum. But other places where large volumes of people gather such as train stations, sporting stadia and hospitals don’t have anywhere near as positive a socio-economic profile as airport, airplanes and cruise ships.

So let’s unpack this seminal work by Dr Kharas, beginning with a definition of what middle class is. According to Kharas, it is broadly accepted (by institutions like the World Bank) as being those households with per capita incomes between US$10 and US$100 per person per day (US$ in PPP – purchasing power parity). This implies an annual income for a four-person middle class household of US$14,600 to US$146,000.

It’s a broad definition and a household income of US$14,600 at the low end might not seem much to those of us fortunate enough to live in developed countries – but it has to be defined somehow and this is how most experts define it. Keep in mind that it’s a relative measure of middle class rather than an absolute measure.

So accepting the definition – and this is my favourite part – the numbers are staggering (what else would The Analyst say!).

Since the start of the Industrial Revolution, it took 150 years for there to be one billion middle class people (in 1985 according to Kharas).

It took 21 years to reach two billion middle class people (2006).

It took nine years to reach three billion middle class people (2015).

It is forecast to take seven years to reach four billion middle class people (2022).

And it is forecast to take just six years to reach five billion middle class people (2028).

By 2030, Kharas estimates there will be a mind-blowing 5.4 billion middle class people in the world.

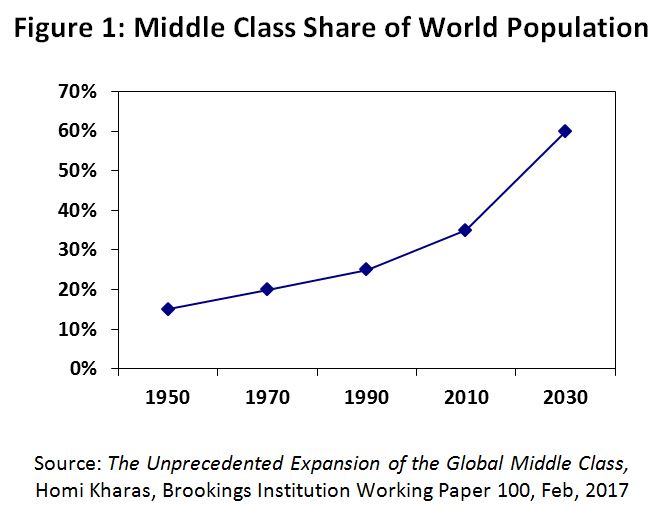

And as a percentage of the population, Kharas estimates that the middle class will surge past 50% of the world’s population by 2020 and reach more than 60% by 2030 as highlighted in Figure 1 below.

The numbers in terms of the consumer goods market are even more staggering. Despite accounting for about 45% of the world’s population in 2015, Kharas estimates that the world’s middle class already accounts for about 65% of consumer goods consumption – around US$35 trillion to be precise, growing to around US$64 trillion in 2030. This near doubling of consumer goods consumption masks what is expected to be a 3-4 times increase in spending on travel (as you will recall, the consumption of this ‘superior good’ rises as a proportion of income as income rises).

In terms of geography, Kharas also measures where the middle class people are and what regions new middle class people will come from in the future.

Asia Pacific, thanks to the recent growth of the world’s two most populous countries (China and India), already accounts for the largest slice of the world’s middle class: 46%. But their share is set to sky rocket to 65% by 2030.

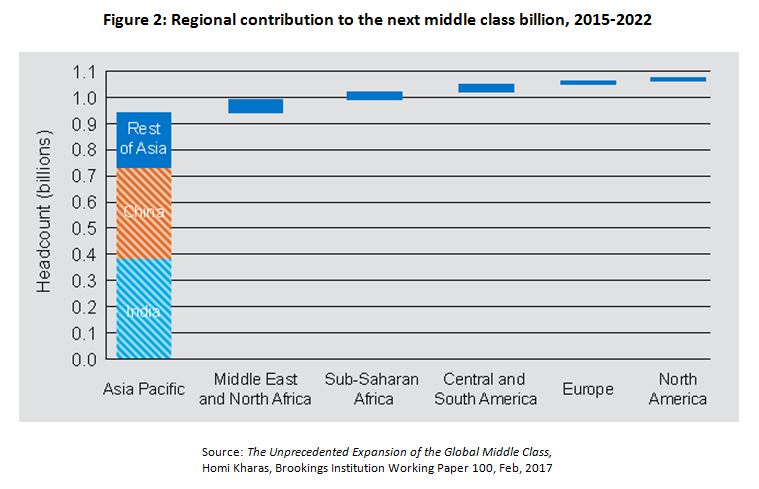

In terms of regional contribution, the most staggering part is highlighted in Figure 2 below. Asia Pacific will account for almost 90% of the world’s next billion middle class people. India and China alone will account for more than 700 million. What implications will this have on travel retail and brand selections?

The developed world (largely Europe and North America) will make relatively miniscule contributions to the growth in the world’s middle classes.

The regional trend in terms of consumption also makes interesting reading. While Europe and North America currently dominate middle class spending (around 49% in 2015), by 2030 Asia Pacific will account for 57% and the combined share of Europe and North America will fall to just 30%.

According to Kharas, in 2015 the top 10 middle class markets in the world were made up from six of the G7 group (France, Germany, Italy, Japan, the United Kingdom and the United States, but not Canada) plus Brazil, Russia, India and China. By 2030, Indonesia and Mexico will enter the top 10 while Italy and France will drop out (mon dieu!). The USA and the UK will still make the top 10 in 2030 according to Kharas but in lower positions (three and ten respectively).

So what does this mean for travel retail? Well, it can’t be bad!

“Can travel retail hold its ground in the face of other competing mega trends – the e-commerce revolution, the growing price transparency of the digital age, and growing sophistication of the distribution system for consumer goods in Asia and the developing world?”

We know from history and economics that newly middle class people take to travel like a starving person to a buffet. International travel has grown at 1.5 to 2 times global GDP for the past 40-50 years. Kharas’ numbers suggest this trend is likely to continue, if not accelerate. Sure, there will be ups and downs along the way, influenced by economic, political and world events, but barring any major catastrophes or the advent of sophisticated virtual reality, the acceleration in the number of the world’s middle class should continue to drive travel.

The challenge for travel retail will be in staying relevant to this heaving mass of newly emerging middle class consumers coming their way.

If the travel retail industry is currently US$62 billion in size (in 2015 according to Generation figures), simple extrapolation of Kharas’ predicted trends suggest an industry of US$150-200 billion by 2030. Many of this newly minted middle class will be first time travellers – perfect for travel retail, especially compared to lower spending, more cynical travel warriors.

“For airports, the challenges are not just about keeping up with the infrastructure requirements of all these extra middle class travellers. They will also need to rethink how their terminals are laid out, their product category assortment, and their brand mix to accommodate particularly Chinese and Indian passengers as the majority.”

But can travel retail hold its ground in the face of other competing mega trends – the e-commerce revolution, the growing price transparency of the digital age, and growing sophistication of the distribution system for consumer goods in Asia and the developing world?

These are big challenges indeed, but Kharas’ work suggests a glittering prize.

For airports, the challenges are not just about keeping up with the infrastructure requirements of all these extra middle class travellers. They will also need to rethink how their terminals are laid out, their product category assortment, and their brand mix to accommodate particularly Chinese and Indian passengers as the majority.

For travel retailers and brands, an in-depth understanding of Chinese and Indian consumers and the different ways you need to sell to these customer groups will be mandatory. These changes will affect all operations from product sourcing to supply chains to staffing.

The Mercurius Group’s experience in working with airports, travel retailers and brands that have understood this massive global trend ahead of time are already profiting. This is no time for them to be meek – even if the meek (or at least the middle class) are inheriting the earth.

Please visit The Mercurius Group website for more information and analysis.

Previous articles by The Analyst:

Is it time to swap airport specialty retail with food & beverage?

A tale of two regions in Australia’s airport development

Does providing a free parking period give you social licence to charge more for car parking?

Car parking spots becoming like airline seats

Australian downtown tax free shopping outstrips airport duty free

‘Brexit’ and the five stages of grief

What does ‘Brexit’ spell for European travel retail?

Australia bucks retailer consolidation trend

*About Ivo Favotto

Ivo Favotto has a long and distinguished record in the airport and travel retail sectors. A trained economist, he entered the airports/infrastructure sector with Australia’s Federal Airports Corporation in 1992 as GM – Planning & Economics.

He later built a highly successful international airports/infrastructure consulting practice, working with three firms – Bach Consulting, Arthur Andersen and URS Corp – and advising many of the world’s leading airports, governments and investors in the areas of retail planning, master planning and privatisation/transaction support.

In 1998 he established the market-leading Airport Retail Study, selling it to Moodie International so he could join The Nuance Group (now owned by Dufry) as Executive Vice President – Strategy & Business Development in Zürich. He later returned to his native Australia as Director – Sydney Airport before being named Executive General Manager of Duty Free & Luxury, Pacific for Lagardère Travel Retail.

![]() He has now formed The Mercurius Group, a Sydney-based consultancy focused on industry research, consultancy and benchmarking studies. The company also assumes responsibility for revamping and relaunching The Airport Commercial Revenues Study (ACRS), which Ivo founded (as The Airport Retail Study) and sold to Moodie International in 2007 as part of an informal alliance between Mercurius and The Moodie Davitt Report.

He has now formed The Mercurius Group, a Sydney-based consultancy focused on industry research, consultancy and benchmarking studies. The company also assumes responsibility for revamping and relaunching The Airport Commercial Revenues Study (ACRS), which Ivo founded (as The Airport Retail Study) and sold to Moodie International in 2007 as part of an informal alliance between Mercurius and The Moodie Davitt Report.

Contact: Tel: +61 423 564 057; E-mail: ifavotto@themercuriusgroup.com; Website:www.themercuriusgroup.com