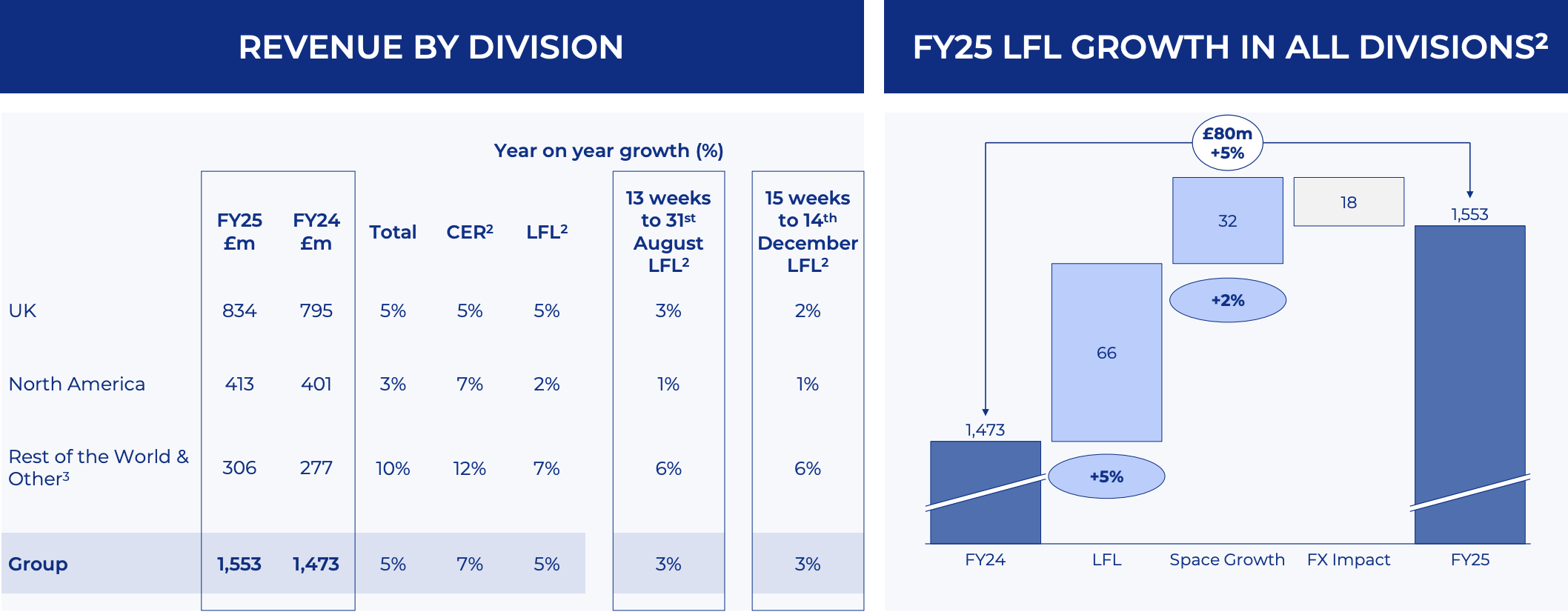

UK. Leading travel retailer WHSmith today (19 December) reported results for the year ended 31 August, with group revenue climbing +5% year-on-year to £1,553 million, and headline group trading profit of £159 million, down from £170 million a year earlier.

The results announcement follows a review into an accounting error related to the travel retailer’s profitability in North America, which led to CEO Carl Cowling stepping down last month.

The company also noted that following the findings of the Deloitte Review into its North American accounts, “a comprehensive remediation plan is in place and progressing at pace”. The Financial Conduct Authority has also begun an investigation into the company.

WHSmith also set out a set of priorities for each division with a “more focused strategy” aimed at delivering profitable growth and enhanced return on capital.

This includes:

*An enhanced focus on the North America travel essentials business, a plan to exit fashion and speciality stores in the region, and a review of its InMotion portfolio through H1 2026;

*A drive to strengthen category leadership in UK travel essentials, scaling health and beauty and the food-to-go offer;

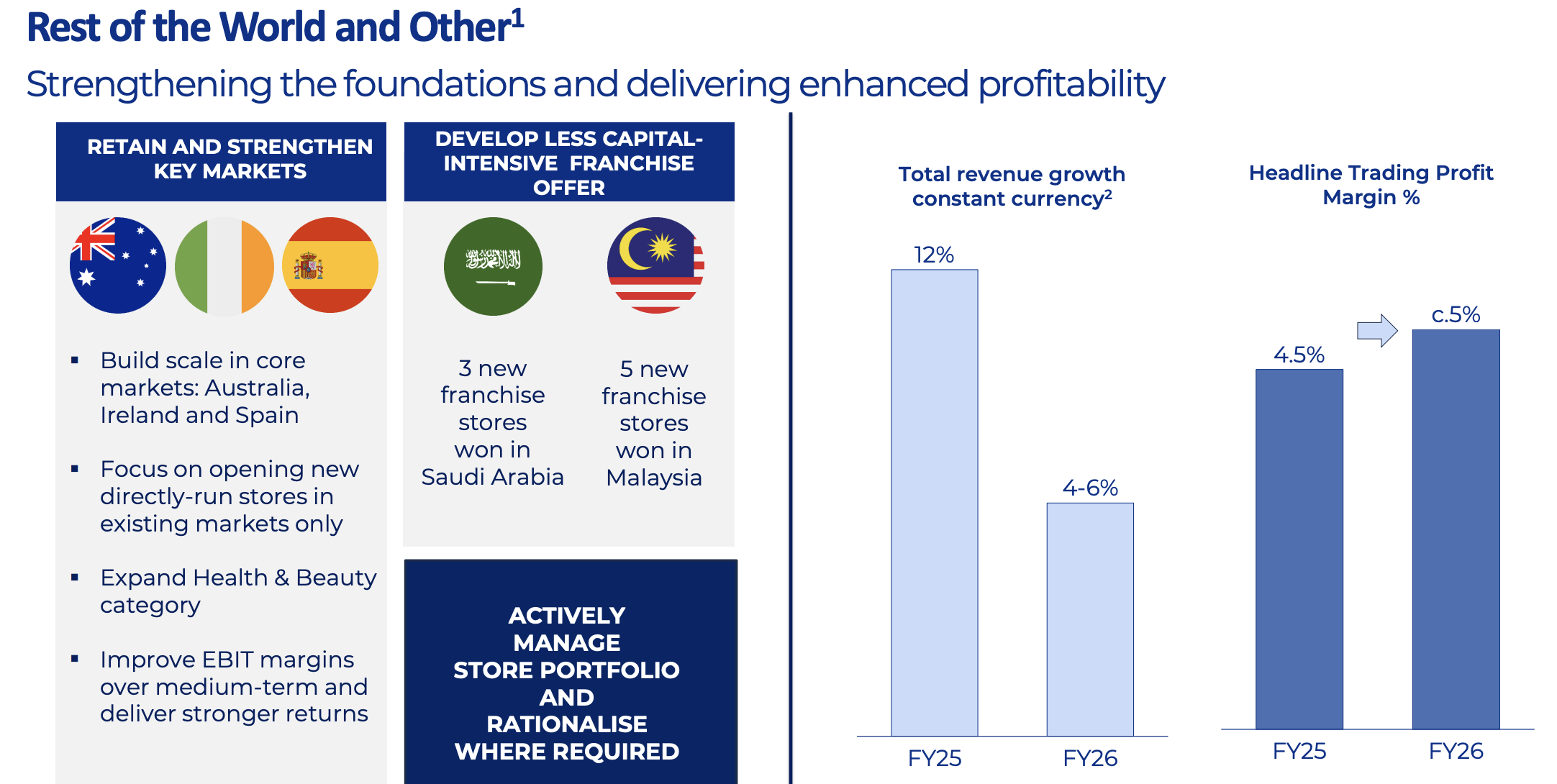

*Strengthen core Rest of the World markets, with new growth driven through a franchise model, plus a review and possible exit from non-core markets.

Elaborating on this in its year-end statement, the company said: “In North America, we will focus on improving and investing in our core travel essentials business. Following a review of our Resorts business, we are in the process of exiting a number of unprofitable fashion and speciality stores.

“We are also undertaking a review of our North America InMotion business and the breadth of the portfolio. Across the business, we have put in place a more rigorous approach to any future store openings with new InMotion stores only being considered as part of a strategically important tender package.” The company stated that it expects InMotion store numbers to reduce over time, with those in the portfolio operating at a higher trading profit margin.

In the UK, the focus lies on retaining category leadership in travel essentials through the one-stop-shop format.

In the ROW division, WHSmith said: “We will focus our investment in our core, strategically important markets, including Australia, Ireland and Spain, resulting in reducing our presence in or exiting sub-scale markets and using a less capital-intensive franchise model for future openings.”

Trading outlook

In the 13 weeks to 31 August 2025, the company delivered like-for-like (LFL) revenue growth of +3%. By division, the UK delivered LFL revenue growth of +3% reflecting softer passenger numbers through the summer period and a reduced level of spend per passenger growth.

In North America, WHSmith delivered LFL revenue growth of +1%. The core Travel Essentials business showed revenue growth of +8% with InMotion down -7% and Resorts down -6%. Rest of the World delivered LFL revenue growth of +6%.

These sales trends have continued into the first 15 weeks of the current financial year, noted the company.

In the first 15 weeks of FY26, the Group delivered LFL growth of +3%, with the UK softening slightly to +2%, largely reflecting a softening in rail. North America revenue trends were in line with the last 13 weeks of FY25 with LFL growth of +1%, and Rest of the World showed growth of +6%.

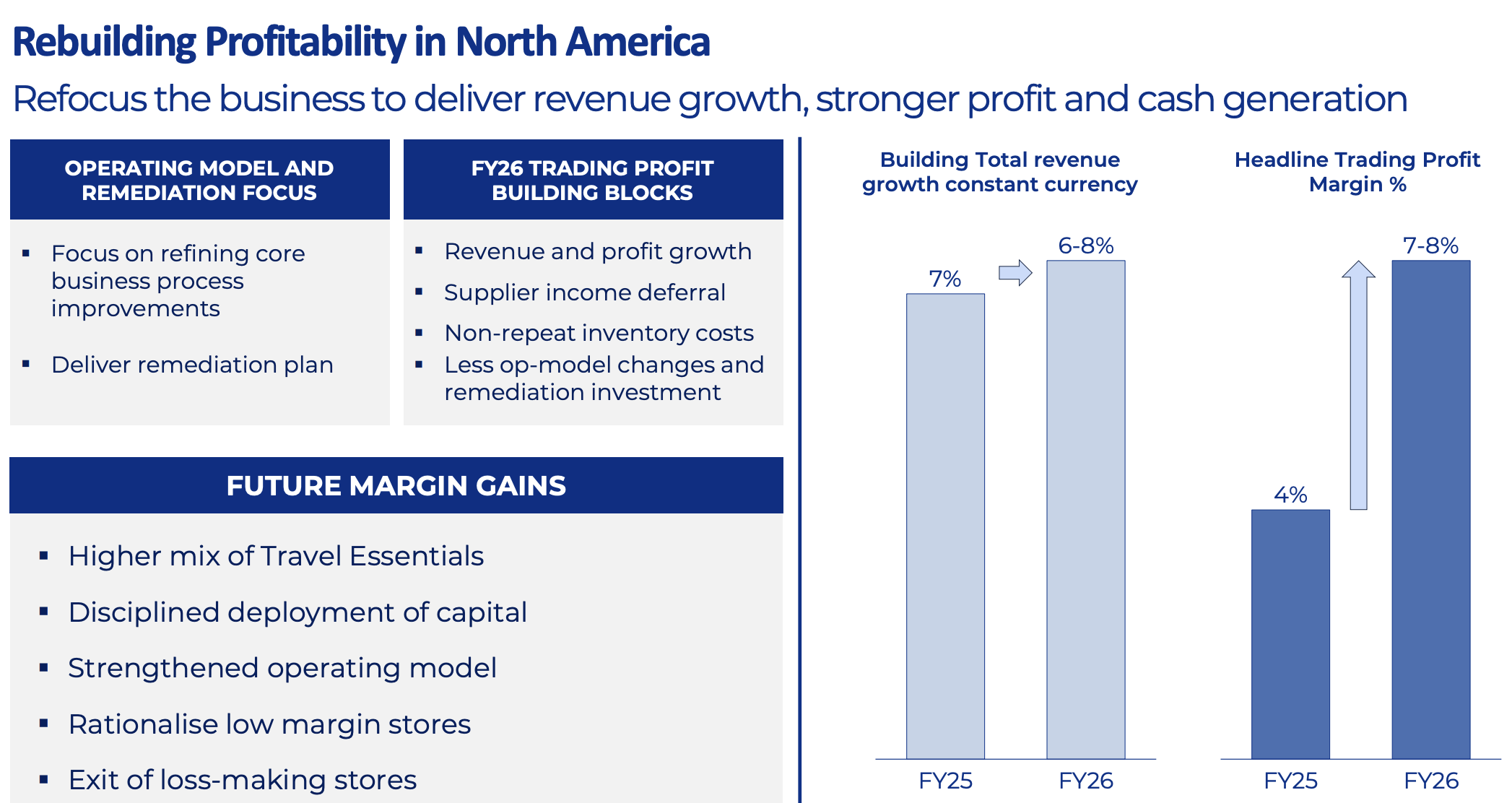

For the full year ending 31 August 2026, total revenue growth of +4-6% is expected.

In the UK, total revenue growth is expected to be around +3-5%, in North America +6-8%, and in the Rest of the World division +4-6%.

Headline trading profit margin in the UK is expected to be at around 14-15%, North America 7-8% and 5% in the Rest of the World.

“This reflects the different dynamics in each market: a year of investment in the UK, a focus on rebuilding profitability in North America and strengthening our foundations internationally,” said a statement.

Interim Group Chief Executive Andrew Harrison commented: “It has been a difficult end to the year for the Group. The Board and I are acutely aware that we have much to do to rebuild confidence in WHSmith and deliver stronger returns as we move forward. We are acting at pace progressing our remediation plan and are committed to ensuring that we strengthen our financial controls and governance as we move forward.

“Following the sale of our UK High Street business and Funky Pigeon during the year, we are now a pure-play global travel retailer. Travel retail is a high growth market, and we have attractive market positions in the UK, North America and our international markets from which we are well-positioned to grow.

“I would like to thank our colleagues who have shown the utmost commitment and professionalism during an uncertain and busy period for the business.

“As Interim CEO, my focus is to provide stability and to lead the Group with transparency and discipline. WHSmith is a business with an exciting future and I look forward to executing against our clear priorities to ensure we capitalise on the attractive opportunities ahead.”

Region-by-region picture in detail

In the UK market, revenue in the year was £834 million, up +5% year-on-year with improved margins, and a headline trading profit of £130 million, slightly below 2024 numbers.

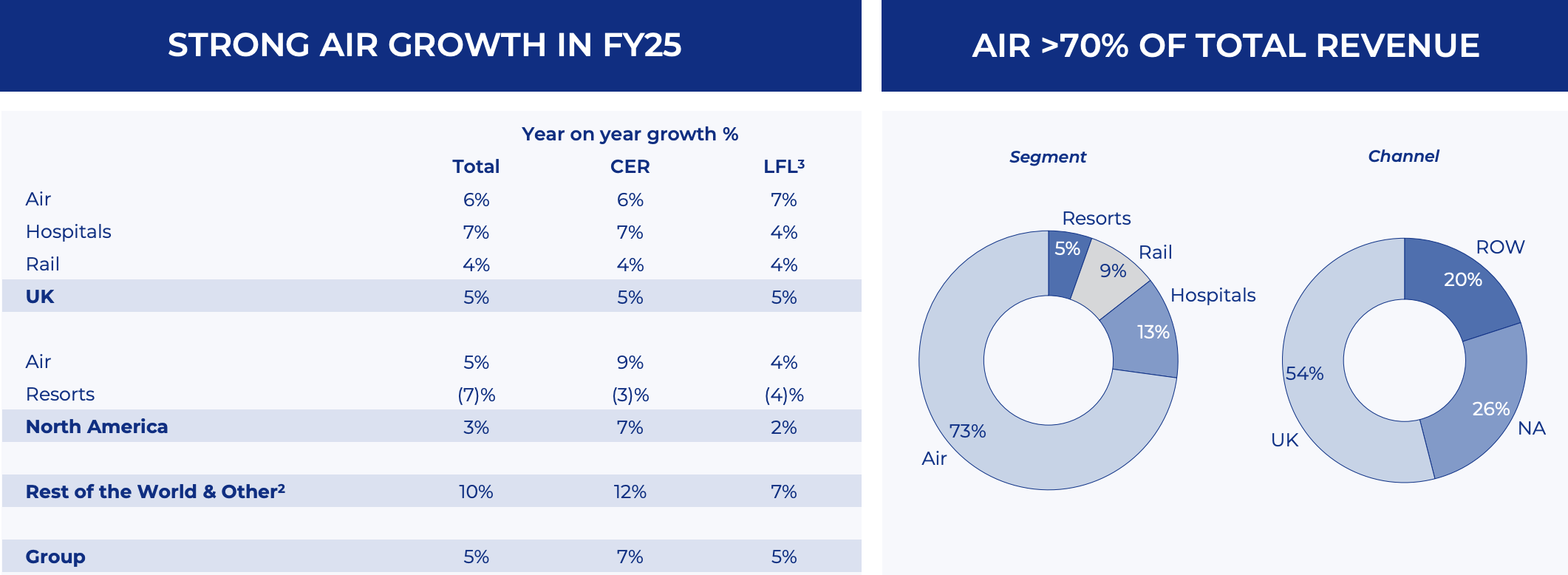

Total revenue in the Air channel was up +6%, supported by spend per passenger growth of +4% on the prior year in travel essentials.

In UK Air, the company added, “2026 will be a year of investment. We will execute our largest-ever store development programme, rolling out our one-stop-shop strategy across six more UK airport terminals, including at London Heathrow, laying the foundations for future growth and long-term success. With this, brings short-term disruption as we reformat our existing stores.

“These new formats will deliver greater convenience for customers and they will be central to our future growth. We are clear that this model works following the success of our store opening at Birmingham Airport in 2023. This is a good example of our strategy in action.

“Following its refit to the one-stop-shop format in 2023, our Birmingham store is our best-performing store in our UK Air estate. With everything under one roof, a full health and beauty offer and an in-store pharmacy, it is driving ATV growth of circa +20% and sales per square foot up over +30%. This success gives us confidence as we scale the format further.”

Revenue in North America increased by +7% on a constant currency basis, with total revenue up +3% to £413 million. Further to the investigation undertaken by Deloitte, headline trading profit was £15 million, down from £34 million in FY2024.

In the region, WHSmith’s travel essentials business grew +19% on a constant currency basis in FY25.

The company noted, “In 2022, travel essentials represented 37% of the overall North America business. Over the past three years, we have invested and grown this business and it now represents 55% of total North America revenue. The segment is our most profitable and, on a fully allocated basis, generates around a 10% headline trading profit margin.

“As we scale our business and enhance our operations, we expect to grow margins further, which will support the overall profitability of our North America division. Given our priority to deliver strong returns, we expect the proportion of travel essentials to increase to over 70% in the medium term.”

Of the InMotion consumer technology business in the region, WHSmith said, “InMotion remains highly regarded by landlords as part of tender packages where it adds value to the overall retail offer in airports and its strong reputation gives us a competitive advantage in securing attractive space within key airports. Our InMotion estate is profitable, however it is in like for like decline and the portfolio is large with 123 stores. During the year, InMotion LFL revenue declined by -3% year on year.

“As we move forward, our approach to operating InMotion will be highly focused. We will limit new store openings with new stores being considered only as part of strategically important tender packages. Where appropriate, we will also move the InMotion proposition into the large marketplace stores, where we offer customers the convenience of everything under one roof, providing flexibility on space use over time.

“In parallel, we will undertake a review of the existing store portfolio. It is imperative that we improve the profitability and revenue performance of this business. As a result, our focus will include undertaking a deeper diagnostic of the estate to determine the factors that need to be in place for these stores to succeed.

“We expect to complete this in the first half of 2026 and we will then be in a position to reshape the portfolio to improve profitability and allow us to better target where we can open new stores that payback with strong returns. We will also focus on our commercial proposition reducing the number of product lines, improving availability and reducing working capital.

“Over time, we expect the number of InMotion stores to decline as we focus on our travel essentials business and integrating more tech accessories into these stores, as well as the impact of landlord redevelopment. In the years ahead, we would expect the InMotion estate to contract by around 20-30% with store numbers reducing below 100 in the medium term.”

Another key focus in North America is the Resorts business in Las Vegas.

WHSmith noted, “There are four primary store formats that make up our Resorts business: hotel convenience and gift stores; ‘Welcome to Las Vegas’ stores; fashion stores and speciality stores.

“Our hotel convenience and gift stores, of which we operate c.20, sell consumables and souvenirs. Our ‘Welcome to Las Vegas’ stores primarily sell souvenirs with some consumables and we operate c.20 of these. We see a good contribution from our hotel convenience and ‘Welcome to Las Vegas’ stores. Despite a decline in LFL revenue in the last year, we continue to benefit from attractive margins and these stores contribute cash.

“Our fashion stores deliver c.25% of Resort revenue and, on a comparable basis, have declined c.-10% year on year. At an aggregated level, these stores are unprofitable and do not generate cash.

“Our speciality stores sell categories such as confectionery and represent c.10% of Resort revenue. LFL revenue also declined around -7% in the year and these stores are marginally unprofitable.

“Following our review, we are exiting a number of Resort fashion and speciality stores, where the leases are short, and we are reviewing further format and other controlled exit route options where the arrangements run over the medium term. While this will take some time, we have initiated the work and the margin and cash benefits, along with growth benefits, already support our FY26 plans.”

In the Rest of the World division, revenue was up +12%, largely driven by new store openings. Headline trading profit was broadly flat year on year with operating investment in the new store openings and gross margin headwinds driven by location mix.

Alongside a focus on “strategically important markets” particularly Australia, Ireland and Spain, WHSmith plans to take a “disciplined approach” to expansion. In the near term, new directly-run stores will be opened only within existing core markets allowing WHSmith “to leverage operational synergies, local market knowledge and established infrastructure”.

It added, “We are sharpening our focus on a franchise-led model, an area in which we already have considerable experience. By working in partnership with experienced local operators, we can leverage their local expertise alongside our space and promotional management to optimise performance. This shift will take time, but it offers several clear advantages and will therefore drive stronger returns. It also provides the ability to grow while reducing operational complexity.” ✈