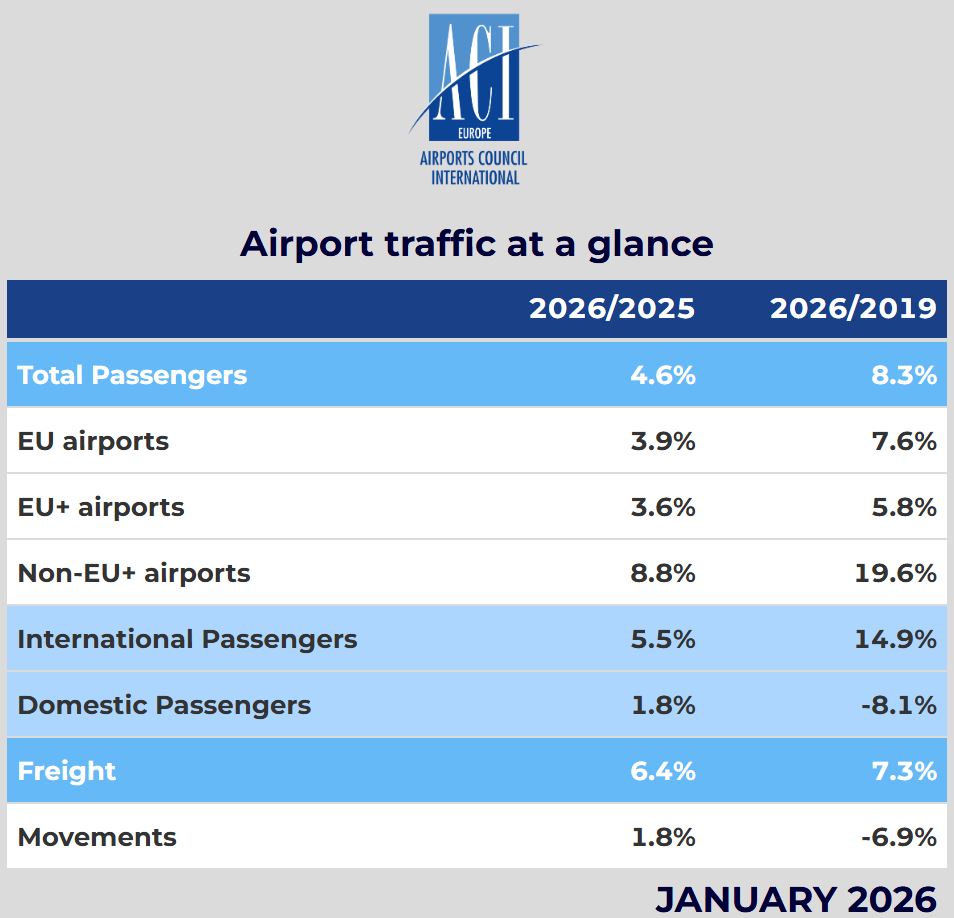

EUROPE. Europe’s airports started the year strongly, with passenger traffic up +4.6% year-on-year, though ongoing Middle East conflicts could disrupt momentum and weigh on positive traffic forecasts.

That’s according to Airports Council International Europe’s latest air traffic report, which highlighted stronger growth at airports in the non-EU+ market (+8.8%), compared with a +3.6% rise in passenger volumes across the EU+ market.

In line with post-COVID aviation market dynamics, growth was mainly fuelled by international passenger traffic (+5.5%), while domestic volumes increased +1.8% yet remained -8.1% below pre-pandemic 2019 levels.

ACI Europe Director General Olivier Jankovec said, “January usually gives us the first indication of traffic performance for the year – and the data we published today would normally be seen as evidence of resilient demand and positive prospects for the months ahead.

“But the conflict which has erupted last week in the Middle East is upending traffic forecasts, making the outlook highly uncertain for now.”

He added, “The Middle East and in particular the Gulf has over the past 20 years become an important part of connectivity and traffic volumes for many European airports – from larger regional ones to major hubs.

“This is not just about direct connectivity and traffic to the Middle East, but also indirect connectivity via that region to Asia Pacific. This means that even if part of the underlying leisure-driven demand could shift to other destinations or other direct and indirect routings to Asia Pacific, that traffic is simply not substitutable.”

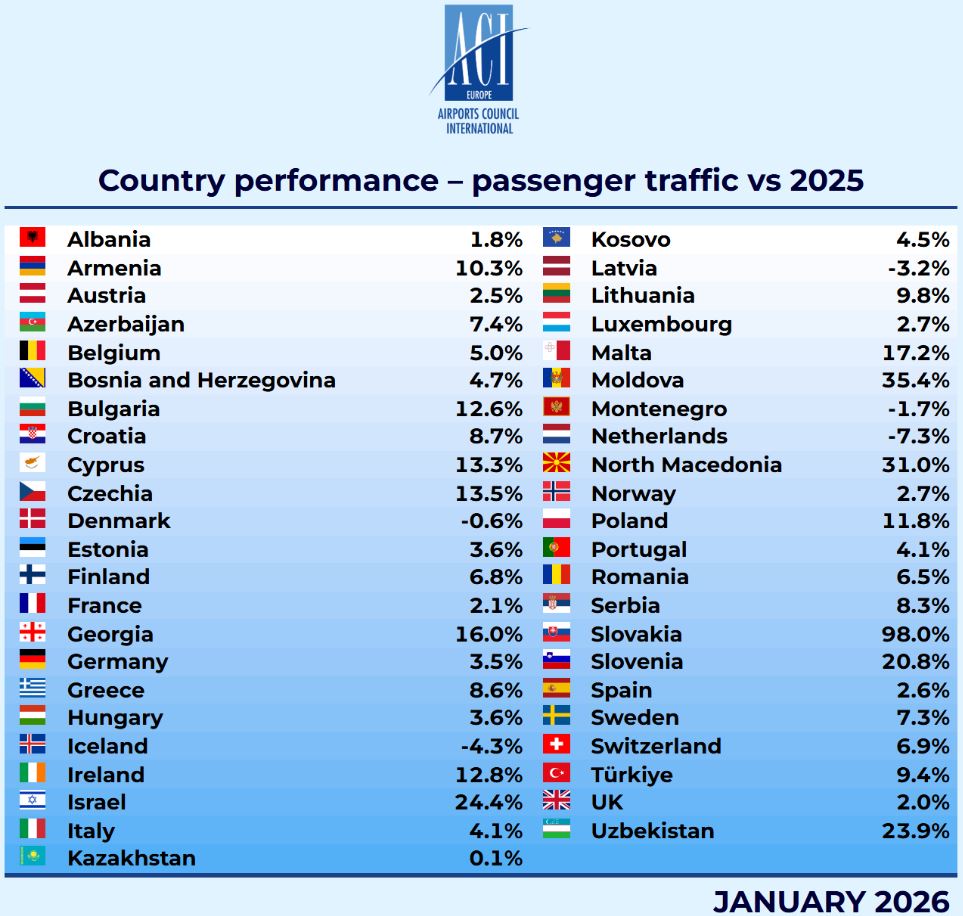

Growth patterns vary widely across national markets

Reflecting patterns seen in January of the previous year, the month was again marked by continued disparities in national and individual airport market performance.

These variations reflect different factors, including the sustained strength of leisure demand, the impact of aviation taxes, geopolitical developments and competitive pressures driven by stronger airline market power, ACI noted.

Double-digit growth was recorded within the EU+ market, led by airports in the eastern and peripheral regions of the bloc. Notable increases include Slovakia (+98.0%), Slovenia (+20.8%), Malta (+17.2%), Czechia (+13.5%), Cyprus (+13.3%), Ireland (+13.8%), Bulgaria (+12.6%) and Poland (+11.8%).

In contrast, airports in the Netherlands (-7.3%) were impacted by adverse weather, while those in Iceland (-4.3%) and Latvia (-3.2%) were hit by airline capacity cuts.

In the EU+ market, Italy (+4.1%) led growth, followed by Germany (+3.5%), Spain (+2.6%), France (+2.1%) and the UK (+2%).

Non-EU+ airports saw sharper gains, with Moldova (+35.4%) ranking first, followed by North Macedonia (+31%), Israel (+24.4%), Uzbekistan (+23.9%), Georgia (+16%), Armenia (+10.3%) and Türkiye (+9.4%).

Airports in Montenegro (-1.7%) and Kazakhstan (+0.1%) lagged well behind.

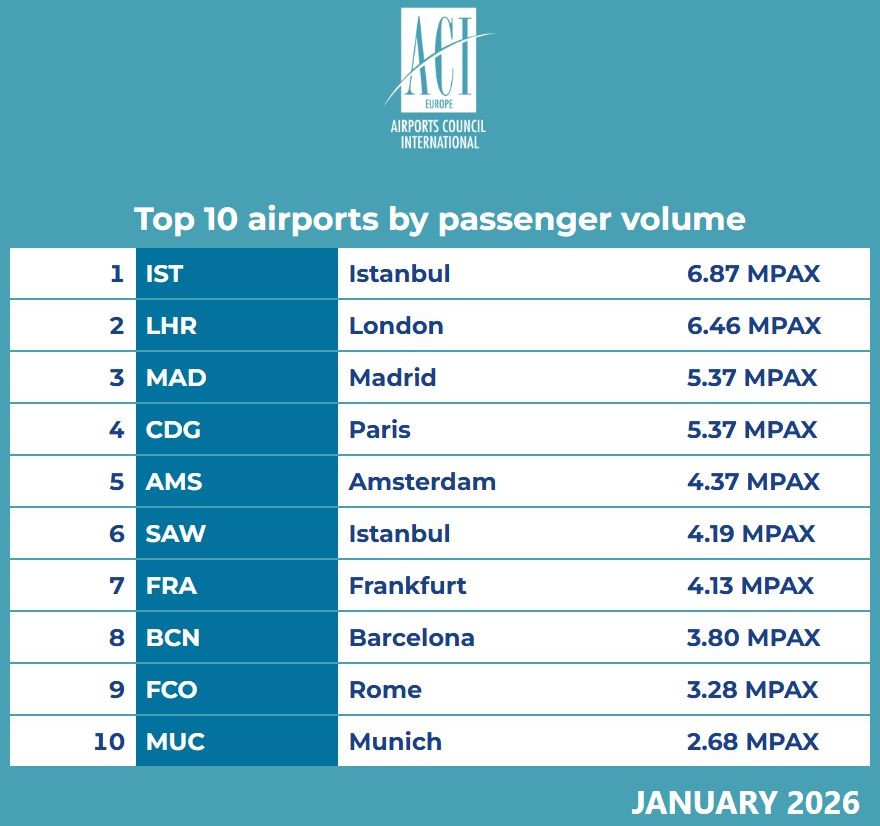

Istanbul leads

Istanbul Airport recorded +6.4% growth, surpassing capacity-constrained London Heathrow Airport (+2.2%) to become the airport with the highest passenger traffic, recording 6.9 million passengers compared with 6.5 million at London Heathrow, averaging more than 220,000 passengers per day.

Passenger traffic in Madrid rose +3.5%, ahead of Paris CDG (+0.7%), while Amsterdam (-9.1%) was hit by severe weather earlier in the month.

Frankfurt posted dynamic passenger growth of +4.9%, securing seventh place, behind Istanbul Sabiha Gökçen (+14.3%), which led the ranking among major airports (over 40 million passengers).

Smaller airports lag in post-COVID recovery

Following the pattern observed throughout 2025, small airports (under 1 million passengers) were slowest to recover from pre-pandemic 2019 volumes (-28.7%) but recorded the highest year-on-year increase at +12.7%.

Small airports remain weak under the post-pandemic aviation trends, with fewer than half (49%) having fully recovered from the COVID-19 pandemic.

Traffic results by airport groups

Passenger traffic in January rose year-on-year across all airport size categories: +2.6% at major airports, +4.7% at mega airports (25-40 million passengers), +6.1% at large airports (10-25 million), +5.1% at medium airports (1-10 million), and +12.7% at small airports (under 1 million).

Top-performing airports in year-on-year passenger growth include the following:

Majors: Istanbul Sabiha Gökçen (+14.3%), Istanbul International (+6.4%), Frankfurt (+4.9%), Munich (+3.9%) and Madrid (+3.5%)

Mega airports: Dublin (+13.8%), Paris (+10.1%), Athens (+8.6%), Zurich (+6.8%) and Antalya (+6.8%)

Large airports: Tel Aviv (+24.4%), Tashkent (+21.6%), Malta (+15.1%), Izmir (+16.4%) and Krakow (+15.7%)

Medium airports: Bratislava (+127%), Trapani (+45%), Varna (+43.1%), Chișinău (+35.4%) and Skopje SKP (+31.4%)

Small airports: Córdoba (+3155.1%), Bucharest (+1020.9%%), Stockholm (+289.3%), Vaxjo (+200.9%) and Stockholm (+193.6%) ✈