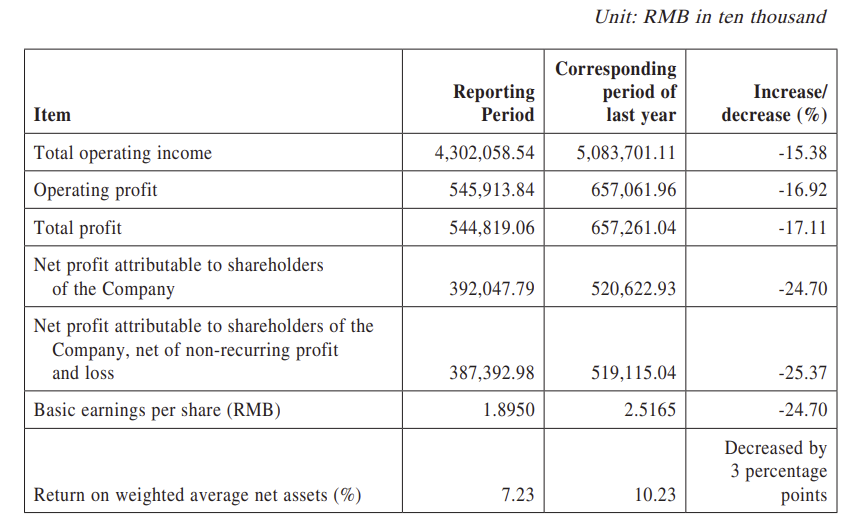

CHINA. China Tourism Group Duty Free Corp (CTGDF) last night posted a -15.38% fall in operating income for the first nine months of 2024 to RMB43,020.5854 million (US$6.04 billion).

Net profit slumped -24.70% to RMB3,920.4779 million (US$550.7 million).

“In a macro-environment of slowdown in domestic consumption growth and low consumer spending enthusiasm, the company faced many difficulties and challenges in its operation,” CTGDF said.

Gross profit margin of the company’s principal business (China Duty Free Group) was 32.57%, representing a year-on-year increase of 1.09 percentage points.

Full revenue and profit information will not be available until the release of Q3 results at the end of this month.

Owing to the continuous expansion of visa-free countries, refinement of visa-free transit policies and a gradual increase in international passenger flights, sales at China Duty Free Group’s departure and arrival duty-free shops increased significantly, the company said. This indicates that performance in the offshore duty-free haven of Hainan island drove the revenue decrease.

Revenue from duty-free shops at Beijing Capital International and Beijing Daxing International airports increased by more than +140% year-on-year while that from Shanghai airports (Shanghai Pudong International and Shanghai Hongqiao International) rose over +60%. During the Reporting Period, the Company continued to enhance the supply of best-selling products and broaden the product boundaries.

In the first three quarters, 165 new brands were introduced, in categories including perfume & cosmetics, luxury goods, food and general merchandise, tobacco and liquor.

Notably, more than 40% were domestic brands, which achieved “significant” sales growth while enhancing recognition and a consumer “sense of belonging” with domestic brands.

In a note downgrading CTG stock to neutral, Goldman Sachs Investment Research highlighted a “lingering weakness” in Hainan duty-free sales (-34% year-on-year) despite a lower comparision base with the lapse of the 2023 daigou crackdown.

“We had been anticipating a better year-on-year sales trend in Hainan since June-July as the base effect should have become more favourable given the lapse of the daigou crackdown which started in mid-FY23,” the firm wrote.H

“However, the data in recent months have remained weak with total duty-free sales reportedly -36%/-33% in July/Aug amid the broader consumption slowdown in China.

“If we assume such momentum continued in September as suggested by the still soft Golden Week holiday duty-free sales (-33% year-on-year) and a steady 80% contribution [to CTG] from duty-free products, we estimate Hainan’s total store sales were steady quarter-on-quarter but dropped -36% year-on-year to RMB7.1 billion (US$997.4 million) in Q324, adding up to RMB30 billion (US$4.2 billion) in the nine months.”

Goldman Sachs lowered its full-year estimate for Hainan to RMB39 billion (US$5.48 billion) and to RMB43/47 billion (US$6.04 billion and US$6.6 billion) in FY25/26E.

xxxxIn common with many travel retailers worldwide, Goldman Sachs said China Duty Free Group had witnessed a healthy airport traffic recovery but revenue dragged by weak per-shopper spending and reduced online sales.

The firm estimated that per-passenger spending in the Shanghai airports ws down -25% year-in-year in the nine months to RMB160-170 (US$22.50-23.90) vs. pre-pandemic RMB360-370 (US$50.60-51.98)

In Beijing Airport per-passenger spending improved slightly to ~RMB150 (US$21,07), still only half of pre-COVID levels, Goldman Sachs observed.

The company’s research suggested China Duty Free Group had refrained from heavy price discounts during the summer. But it added: “The situation has changed somewhat given much weaker consumption sentiment and more intense pricing competition in recent weeks.

“Our channel checks indicate that CTGDF has also stepped up its promotions which continued into the Golden Week holidays.”

The report concluded: “Fundamentally, we still see several headwinds for CTGDF’s earnings trajectory, i.e. weak consumption sentiment, diversion of traffic to overseas countries, competition from online, potential impact from less cost advantage upon Hainan turning islandwide tax free [in 2025].”

The firm expects some modest benefit to CTGDF from the newly announced downtown duty-free shopping policy that came into effect on 1 October. ✈