SOUTH KOREA. Further details have emerged of the licence model for the forthcoming duty free tender at Incheon International Airport, likely to be released this week.

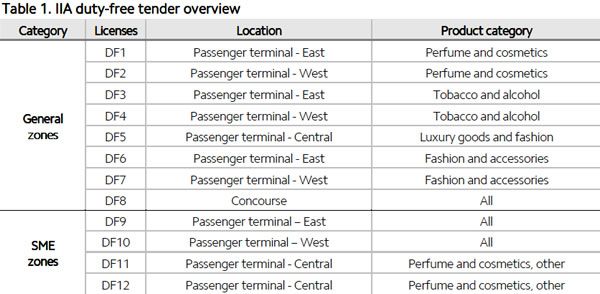

As reported, last week Korea Customs Service announced the licence structure for the long-awaited duty free tender. As anticipated earlier by The Moodie Report, the tender is being split into packages available to major retailers and small & medium enterprises (SMEs), respectively. The seven major licenses, currently held by Lotte Duty Free, The Shilla Duty Free and Korea Tourism Organization (KTO), are being extended to 12.

An additional four licenses will be offered to SMEs with no company being able to win more than one contract. All agreements will run for five years.

|

The number of zones available for bidding will expand from seven to 12 |

The tender, in line with government edict, also requires that a minimum of three major duty free players, either national or international, be awarded contracts, which will mean additional powerhouse competition for Shilla and Lotte (state-owned KTO can bid but, unlike before, is not guaranteed any contracts).

The tender closes by 26 February 2015, meaning that the incumbents are likely to have their contracts extended for some time (current concessions expire at the end of February 2015).

So who might bid for what at Incheon? The five local companies to bid last time around in 2007 were Lotte, Shilla, AK Duty Free, Paradise Duty Free and Walker Hill. AK was subsequently acquired by Lotte in 2010 (giving it back a much-coveted perfumes & cosmetics presence it had lost in the 2007 tender) while Busan-based Paradise was taken out by department store powerhouse Shinsegae in September 2012.

|

Cross reference the map locations with the table above to see where the major and SME retailers respectively will be operating. Click on the above to view the enlarged image (then hover over graphs with your cursor and click for full detail) |

Lotte and Shilla are certainties and so, local sources believe are Shinsegae (which has a strong landside presence at Incheon), and Hanwha Timeworld, a division of prominent Daejeon-based department store retailer Hanwha Galleria, which won the duty free concession at Jeju International Airport in February 2014.

International retailers will also be able to bid for the general zones. But who will? Tendering on such a scale involves a great deal of time, money and management resource and unless international players feel they have a genuine chance of success, their interest is likely to be muted (especially given the fragmentation of the major concessions).

|

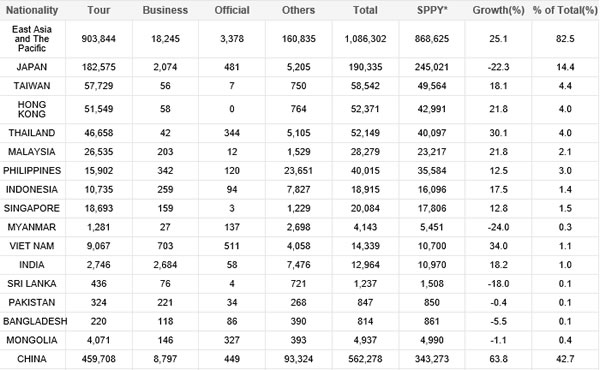

Selected arrivals to South Korea by purpose and nationality in October 2014 underline the continued extraordinary surge in Chinese visitor numbers; Source: KTO |

|

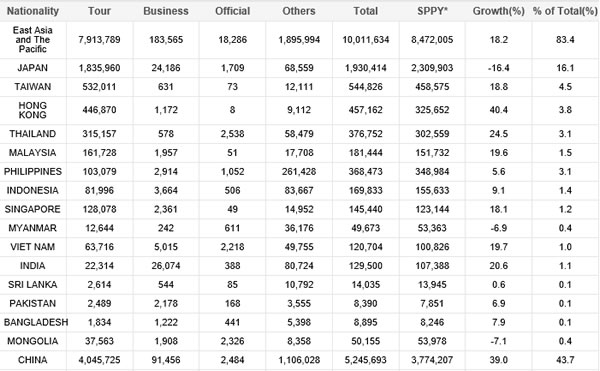

Accumulative figures of selected arrivals to South Korea by purpose and nationality for the ten months to October 2014. Note the relative performance of Japanese to Chinese; Source: KTO |

|

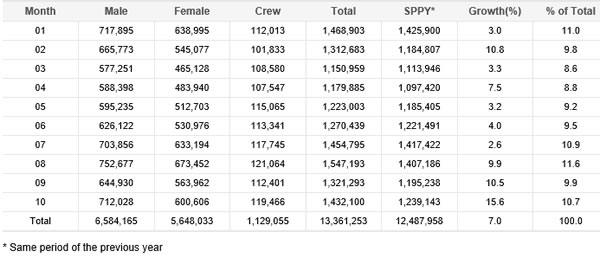

Departures by Koreans for the first ten months of 2014 by gender (above) and by age (below) |  |

DFS ran a highly successful operation at Incheon from the airport’s opening in 2001 to 29 February 2008 but – in common with King Power Group (HK) and Aldeasa (now World Duty Free Group) – was dismayed to witness an all-Korean result in the 2007 bid.

The SME line-up will be interesting. Dongwha, long established in the downtown duty free market, is a likely runner. So is Entas Duty Free, which is poised to open a major downtown duty free store in Incheon city as well as its 740sq m store at Incheon Port’s international passenger terminal 1. Another likely candidate is The Grand Duty Free, exclusive downtown duty free operator in Daegu, the country’s third-largest city, which harbours strong growth ambitions in the airport and e-commerce sectors.

The Korea Economic Daily warned: “The problem is there are not many small companies that are deep-pocketed enough to pay the high lease cost over a five-year rental period. Currently major duty free shop operators like Lotte and Shilla are paying about KW20 million (US$17,900) a year per square meter. With a store space of 1,500sq m, one has to pay KW30 billion ( US$26.9 million) in annual rental costs. In addition, the upfront deposit is as high as half of the first year’s annual rental cost.”

Certainly any SME operator will be faced by daunting big-company competition, sometimes selling identical categories within a few metres. How they can compete is a major dilemma and several seasoned observers of the market fear a lowering of merchandising and service standards across the smaller outlets.

|

The world’s biggest duty free tender has been split up to offer multiple opportunities to the industry giants and small & medium enterprises |

|

|

|

In a note, Regina Hahm, Equity Analyst at KDB Daewoo Securities Co, commented: “The SMEs are unlikely to have the ability to source quality duty free merchandise. They lack bargaining power against the suppliers and will be unable to have the competitive pricing structure of current major players.

“The biggest strength of domestic duty free shop operators is probably merchandising, from product sourcing to sales and inventory management. In Korea, production and sales operations are usually separated; in department store channels, brands, not the department store operator, tend to oversee merchandising activities. Thus, the strong merchandising capability of duty free shop operators is a rarity among Korean retailers. This qualitative strength is not easily attainable, as it requires years of experience and an economy of scale.”

We’ll bring you extensive analysis of the Incheon tender in a special report in this week’s Moodie e-Zine, out Thursday.

INCHEON INTERNATIONAL AIRPORT DUTY FREE TENDER AT A GLANCE

• The number of zones available for bidding will expand from seven to 12.

• Specific zones (DF9-DF12) will be available only to SMEs.

• A single company will not be allowed to operate multiple SME zones. Thus, four separate SME retailers will run duty free operations at IIA.

• Eight zones will be available to non-SMEs. At least three companies will be granted licenses in these zones.

• As a result, the overall number of duty free shop operators will increase to at least seven.