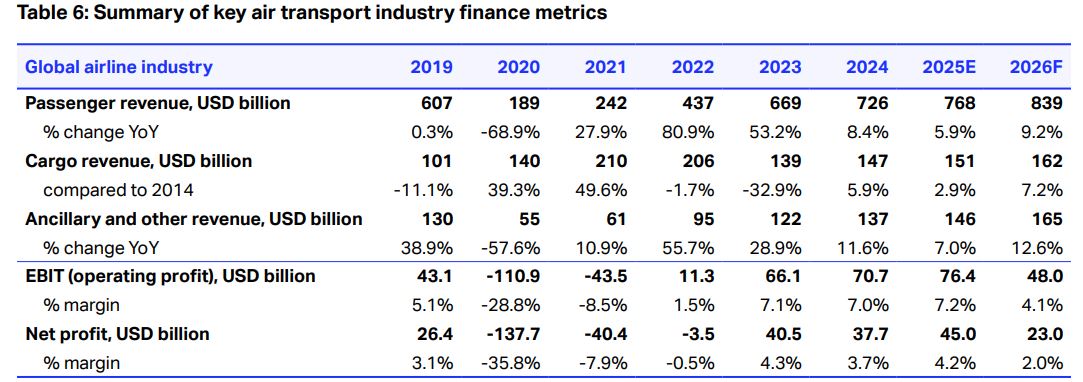

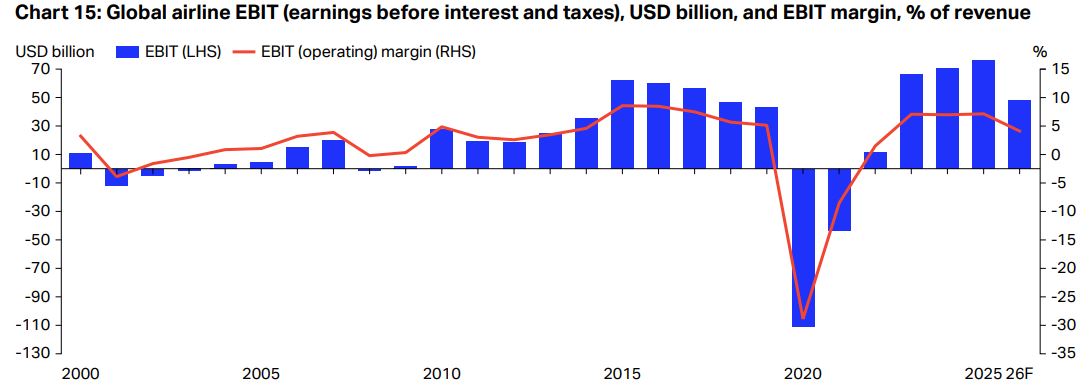

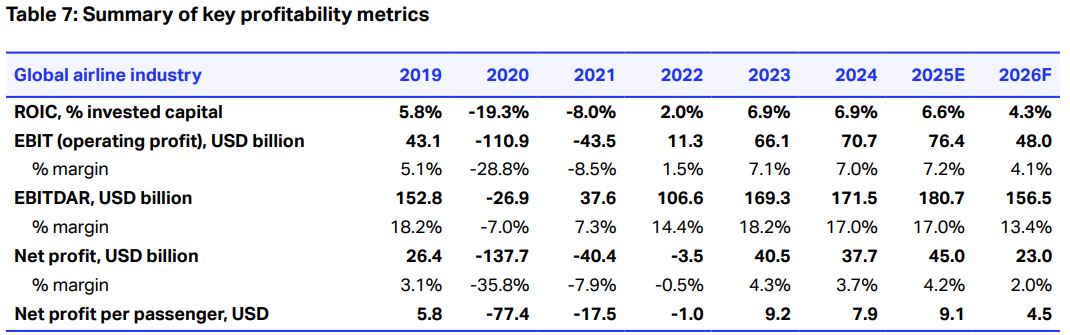

INTERNATIONAL. The global airline industry’s net profit is forecast to fall by approximately -50% year-on-year to US$23 billion, driven by continuing war-related disruption in the Middle East and rising fuel costs, according to the latest financial outlook from the International Air Transport Association (IATA).

The projected collective net profit for airlines is also nearly half the previous forecast of US$41 billion.

While performance varies considerably by region, the association expects Middle East carriers to be among the hardest hit, forecasting a collective loss as weak demand and operational disruption weigh on results.

The latest outlook highlights a sharp decline in airline profitability, even while demand and revenues continue to rise.

Net profit margin is estimated at 2.0% in 2026, around half the previous projection of 3.9% and well below the estimated 4.2% margin for 2025.

Net profit per passenger is forecast to decline to US$4.50, with operating profit plunging -37.2% to US$48 billion for an operating margin of 4.1% (down from -7.2% year-on-year).

Return on invested capital is forecast at 4.3%, well below the estimated 8.5% cost of capital, a gap that underscores the airline industry’s structural weakness.

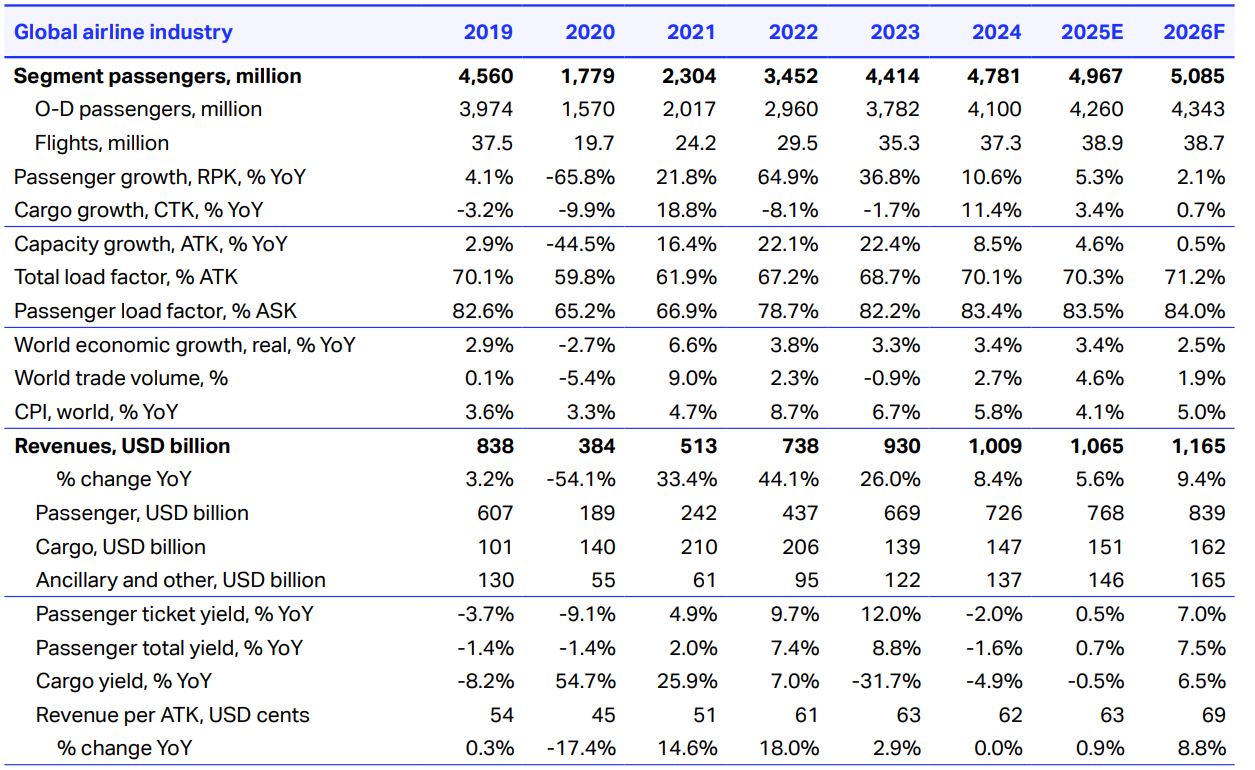

Despite these pressures, total industry revenues are expected to rise +9.4% to US$1.165 trillion, while passenger load factors are forecast to reach a record 84%, up from 83.5% from the previous year. Passenger numbers are projected to grow +2.4% to 5.1 billion.

IATA Director General Willie Walsh said: “War-related disruptions in the Middle East and rising fuel costs have shifted the outlook for airlines to the worse. Globally, airlines are expected to see profitability halve compared to 2025. Profits will shrink from US$45 billion in 2025 to US$23 billion this year.

“And margins will shrink from 4.2% to 2.0%. All airline bottom lines are suffering from the rapid +70% rise in jet fuel prices. Some of the additional cost is being recuperated by adjusting prices and improving efficiency, but it will not be sufficient to maintain profitability at the previous year’s level.

“Smaller carriers that started the year with weak balance sheets are certainly struggling. At the regional level, all are in the black but with sharply reduced financial performance, with the exception of the Middle East.

“The Gulf carriers face operational uncertainty following a near complete shutdown of airspace at the outbreak of the war. These carriers are doing an amazing job maintaining connectivity, but major financial impacts are unavoidable.”

IATA noted that even under favourable conditions, the industry will struggle from low margins and returns below the cost of capital. The surge in oil prices has challenged airline financial strength, narrowing net margins worldwide to just 2% globally.

Walsh added: “Airlines are bearing the brunt of the fuel price shock. While air fares are rising, airlines are still absorbing part of the hike in their bottom lines. Net profit per passenger is expected to fall to $4.50, half of what it was last year.

“Under the circumstances, that shows resilience. But it won’t even buy you a hot dog at most of the FIFA World Cup venues and it does not leave much of a buffer should other costs or taxes start rising.”

Outlook drivers

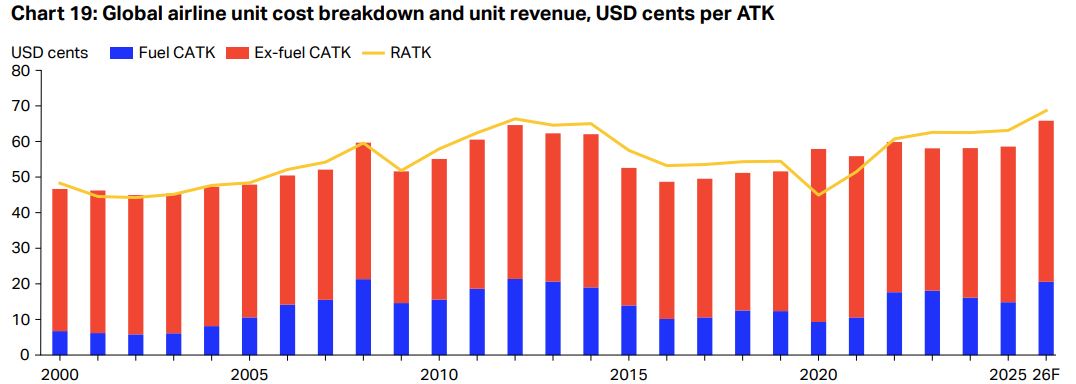

Revenue growth is expected to remain strong in 2026, with revenue per available tonne kilometre (ATK) forecast to climb +8.8%, a notable increase comparable only to 2008 and 2010, when airlines faced significant fuel price shocks.

Despite the revenue rise, operating expenses are expected to outpace revenue growth, rising +13% to US$1.117 trillion, and slashing net profit by almost half to US$23 billion.

The outlook is further weighed down by weaker macroeconomic conditions, including slower GDP growth, higher inflation and reduced global trade growth.

Revenue

Passenger ticket revenues are expected to generate US$839 billion, up +9.2% in 2026, outpacing demand growth of just +2.1% as airlines raise fares to offset higher fuel costs.

Passenger ticket yields are projected to grow +7%, while load factors soar to an all-time high of 84.0%.

Ancillary and other revenues are forecast to grow +12.6% to US$165 billion, surpassing air cargo as a source of revenue for the first time since 2019.

Costs

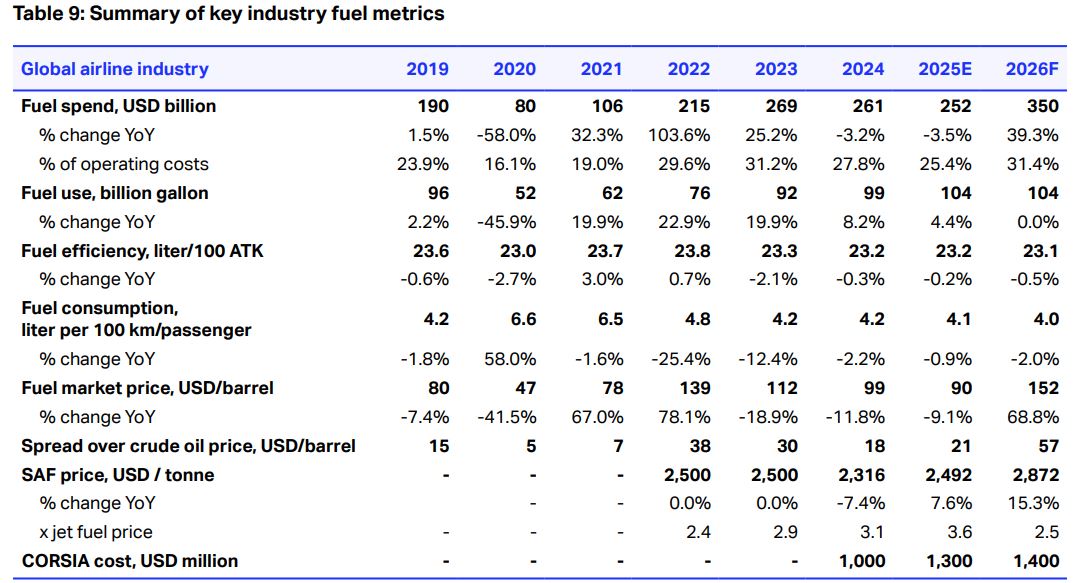

A sharp rise in fuel prices is projected to be the main driver of airline cost inflation in 2026, with fuel expenditure forecast to jump +40% to US$350 billion from a year earlier.

Although fuel consumption is expected to remain unchanged from the previous year, higher jet fuel prices will increase fuel’s share of operating costs to 31.4%.

Additional costs include Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) compliance at US$1.2-1.6 billion to offset 28.8-81.5 Mt of carbon emissions. Sustainable Aviation Fuel (SAF) procurement is projected at US$4.3 billion for 2.4 million tonnes (0.8% of total fuel use), slightly lower than prior estimates due to a reduced price spread versus jet fuel.

Airlines’ non-fuel costs are forecast to rise +4% to US$767 billion, with labour accounting for US$271 billion and a total workforce of 3.33 million, up +1% year-on-year.

Productivity per employee (measured in ATK/employee) slid -0.4%, as operational resilience remained the priority amid disruptions.

Additional cost pressures are also attributed to record aircraft lease rates and higher maintenance needs linked to ageing fleets.

Also weighing on the outlook, the US dollar is expected to weaken around -5% in 2026 (after a -10% drop in 2025), partially offsetting costs for non-US carriers by lowering dollar-denominated fuel and debt.

Risks and constraints

Supply chain challenges: Aircraft supply remains structurally constrained, with the backlog rising to 18,100 aircraft in May 2026 from 17,000 in 2024, more than 50% of the active fleet.

Deliveries remain below pre-COVID peaks despite gradual recovery in production. Airlines are compensating through higher utilisation and extended aircraft lifecycles, but the shortage is now limiting capacity growth and halting fuel-efficiency and carbon reduction gains in 2024-2025.

Elections and geopolitical uncertainty: Over 40 countries representing more than 1.5 billion people will hold elections during the year, including the US midterms, Brazil and Israel. Outcomes are expected to affect responses to inflation, trade tensions and fiscal and monetary policy, as the energy crisis is shifting government focus worldwide.

Stagflation risk: Slower growth and higher inflation are expected to weigh on the industry’s strength. While IATA’s latest survey reveals that 49% intend to spend more on travel over the next 12 months, and 43% about the same.

83% remain highly cost-conscious even as 86% expect transport prices to fluctuate with oil prices, highlighting sensitivity to sustained fare increases.

Infrastructure constraints: These constraints continue to drive up costs and restrain growth, according to IATA. With capacity insufficient to meet demand, the Middle East war has become a particular concern for slot allocation.

Flexible rules are needed to avoid penalising airlines when closures limit slot usage, while economic regulators must respond to any demand weakness with efficiency gains, instead of rate hikes.

Regional roundup

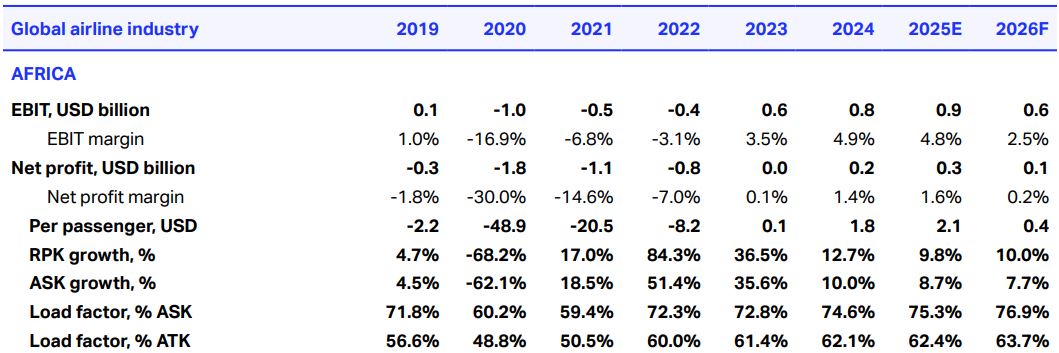

Africa: While Africa’s hub carriers are benefitting from increased traffic as airlines reroute from the Middle East, profitability is expected to decline in 2026 due to high fuel costs, lower utilisation and weaker balance sheets.

This limits the revenue upside, but benefits are likely to be concentrated among a few major hub carriers with established connectivity linking Africa to Europe and Asia.

The challenging operating environment is expected to hit smaller, more fragmented airlines the hardest. Ongoing structural issues, including weak infrastructure, fragmented airspace and limited financing capacity, continue to limit growth and expansion.

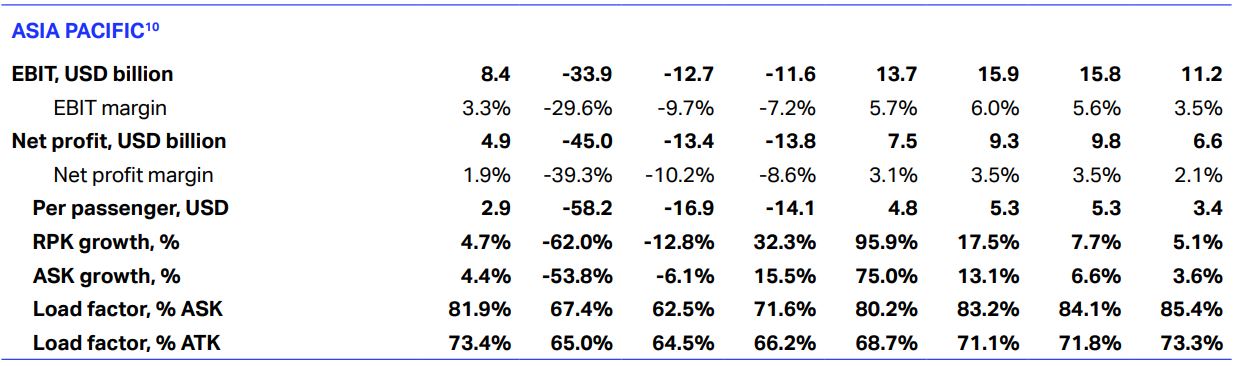

Asia Pacific: Elevated cost pressures are impacting the region due to fuel supply constraints from Gulf crude imports, which are restricting jet fuel availability and inflating prices.

Longer flight routings due to airspace restrictions are further increasing fuel burn and unit costs.

Despite this, passenger demand continues to increase, and some airlines are benefitting from rerouted Europe-Asia traffic flows linked to Middle Eastern hub disruptions.

However, currency depreciation across parts of Asia is increasing US dollar-denominated expenses, most notably fuel.

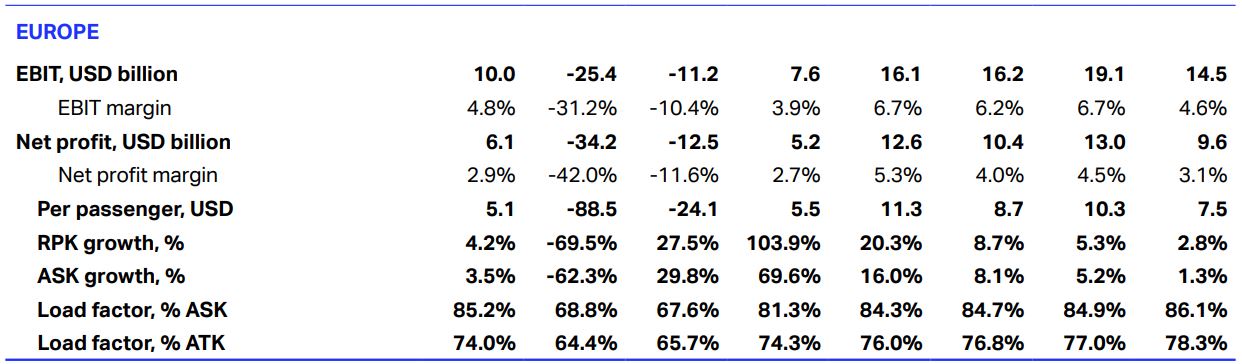

Europe: Airlines in the region face rising cost pressures from Gulf-linked jet fuel imports, partially offset by a 70% pre-crisis hedging ratio, although higher costs will feed through as hedges expire.

Some traffic gains have come from Europe-Asia direct connectivity, but airspace restrictions over Russia and weaker macroeconomic conditions are limiting demand.

High regulatory costs, including SAF mandates, airport charges and labour disruption, continue to weigh on competitiveness across the region.

Latin America: Currency depreciation linked to the energy crisis has been weighing down Latin America’s performance, as well as more demand-sensitive markets due to lower incomes and a smaller business travel base.

Limited balance sheet flexibility and higher funding costs constrain airlines’ ability to absorb shocks or invest, with an EBIT-to-net margin ratio around four times the global average highlighting this constraint. Overall, the region is expected to see a sharper growth decline despite sustained demand.

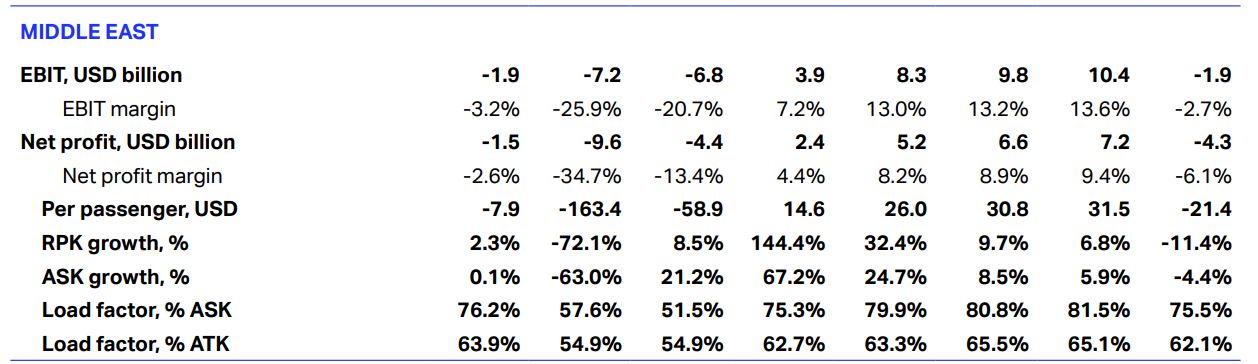

Middle East: The region is projected to record a net loss in 2026 as the Middle East conflict drives capacity reductions, operational disruption and higher fuel costs, while the loss of transfer traffic is affecting load factors and unit costs.

Recovery is expected to be pricing-led rather than volume-driven, with longer-term structural advantages supporting a traffic rebound but at potentially lower margins, reshaping hub-based economics.

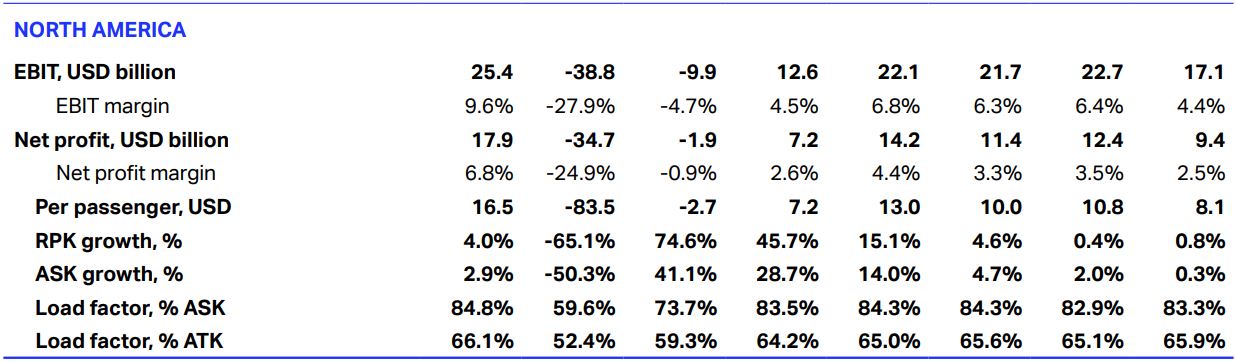

North America: With limited fuel hedging, North American are more directly exposed to rising jet fuel costs, prompting faster pricing responses to offset higher expenses.

Network carriers are relatively better placed than low-cost operators, which remain more exposed to domestic demand downturn and have limited ability to offset cost pressures through upselling and fare segmentation.

Despite strong recent profitability and limited exposure to Middle East disruptions, higher leverage and elevated labour costs increase sensitivity to cost shocks.

The region is therefore expected to see a price-driven adjustment and growing performance gap between resilient network carriers and more constrained low-cost operators. ✈

Traveller’s viewpointIATA’s survey highlights strong and resilient passenger sentiment toward air travel, which continues to deliver exceptional value to consumers. Despite higher fares driven by elevated fuel prices, average real return airfares (including ancillaries) are expected to reach US$462 in 2026, -26.3% lower than in 2016. In a poll of 6,500 travellers across 15 countries, 97% of respondents said they were satisfied with their last trip, while 79% agreed that flying offers good value for money. The survey also found that 81% of respondents believe they have lots of options when purchasing air travel, and 88% said their ability to fly in the future matters to them. Among respondents, 89% believe air connectivity is vital to the economy, and 88% say air travel positively impacts societies. A further 83% view the global air transport network as a key contributor to the UN Sustainable Development Goals, while 90% hope future generations will be able to travel more by air. Despite widespread conflicts, traveller confidence remains high, with the survey indicating that 41% plan to travel more over the next year and 52% at the same level. While 91% believe flying is safe (and 85% say it is safer than ever), travellers are taking more precautions, with 86% checking government advisories, 84% researching more before travel, 81% concerned about disruptions, and 71% booking closer to departure. Still, 68% say their travel habits have not changed at all. |