INDIA. A new report from the Centre for Aviation (CAPA) underlines the surge in non-aeronautical revenues at India’s airports, and especially those operated under the public-private partnership (PPP) model, over the past five years. The Moodie Report works closely with CAPA, which provides analysis and research into the global aviation market.

India embarked upon a multi-billion dollar airport modernisation programme in 2005. One of the key pillars of this programme was the introduction of the public-private partnership (PPP) model to upgrade and develop the two primary gateways at Delhi and Mumbai, and to construct greenfield facilities in Bangalore and Hyderabad. Prior to this, all airports in the country, with the exception of Cochin Airport, were operated by the state-owned Airports Authority of India (AAI).

Private capital was attracted to the Indian airport opportunity because of fast-growing passenger and freight traffic, and because there was seen to be significant upside potential in non-aeronautical revenue. In FY2006, the last year in which all metro airports were operated by the AAI, non-aeronautical activities generated just 15.1% of total revenue, compared with around 50% or more being achieved by commercially driven airports in other parts of the world.

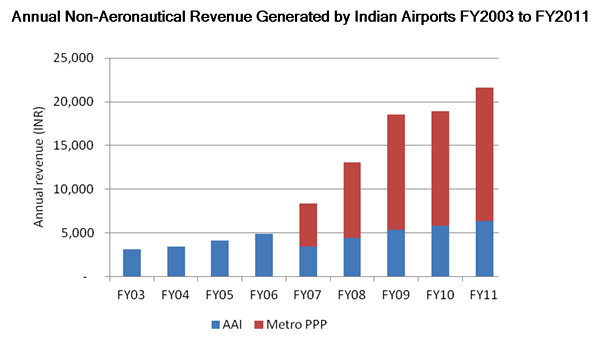

The results since then indicate that the optimism about the revenue growth potential was well-placed, said CAPA. In the last five years total non-aeronautical revenue generated across all airports in the country (excluding Cochin) has grown by more than +340% from INR4.9 billion to INR21.6 billion. The vast majority of this growth (91%) has been driven by the four metro PPP airports at Delhi, Mumbai, Bangalore and Hyderabad.

|

Source: CAPA, company filings |

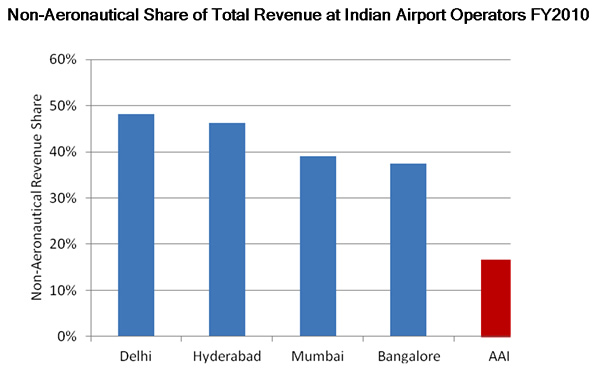

The difference in the commercial approaches of the AAI and the four PPP airports is starkly visible from an analysis of the non-aeronautical share of total revenue. All of the PPP airports have grown their non-aeronautical revenues to at least 35% of total revenue, and more than 45% in the case of Delhi and Hyderabad airports. However, in the case of the AAI it has risen by less than a couple of percentage points over the last five years to reach just 17%. There exists huge but unrealised potential for non-aeronautical revenue growth at the AAI airports, particularly at Chennai and Kolkata, CAPA notes.

|

Source: CAPA, company filings |

Airport Retail Drives Revenue Growth since 2006

The impressive growth that PPP airports have achieved in non-aeronautical revenue has largely been driven by a focus on developing retail and duty free. International standard retail formats were entirely absent from Indian airports, even the metro gateways, prior to 2006.

Retail represents a major opportunity because more Indians are travelling, they are travelling more often and they have more money to spend when they do, CAPA noted.

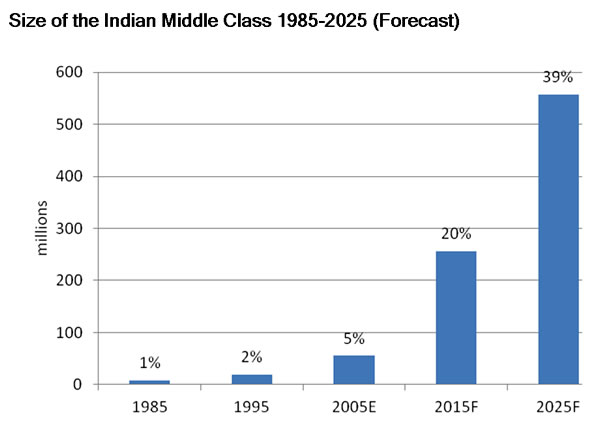

McKinsey forecasts that the size of the Indian middle class will grow from 55 million in 2005 to 256 million in 2015 and 557 million in 2025, by which time it will represent 39% of the population. Total consumption by middle and high income groups is forecast to grow 14 times from INR4 trillion to INR56 trillion over this 20 year period.

|

Number above bar indicates percentage of total population. Source: McKinsey |

Furthermore, CAPA research has highlighted shopping as the favourite activity of Indian travellers indicating that the retail potential can be exploited by encouraging an existing behaviour rather than having to try and forge new attitudes. Indians have always wanted to shop, but until recently the country’s airports did not present them with an opportunity to spend their money at home.

As PPP airports have introduced more attractive retail environments, with a greater choice of products at competitive prices, passengers have responded. For example, in the five years from 2006 to 2011, international passenger movements at Indian airports increased by +70%, but the sales of whisky grew by +290%, and of other spirits by +660%.

But if airports are to effectively mine this potential it is important to dig deeper to better understand the Indian consumer, CAPA added. A research based approach to the planning, design and development of retail formats in India will be essential because:

• The Indian consumer is not homogenous – there are significant variations by reason for travel (from corporate travellers to expatriate labour); region of the country, age, income and travel experience;

• This diversity is further complicated by change, with each individual customer segment rapidly evolving due to strong socio-economic forces from the impact of growing wealth on behaviour and expectations; influence of media and communications on taste and aspirations; societal and inter-generational changes in attitudes towards consumption; the growth of wealth and retail in non-metro cities and the number of first time travelers entering the market. Brands and retailers must begin to understand India’s massive youth population which will drive the retail trends of tomorrow.

These changes will accelerate over time and the airport retail offer must be flexible, CAPA said. Despite the recent rapid growth, international airport retail in India is estimated to turnover around US$250 million per annum across all airports combined, which compares with close to over US$1.5 billion at Dubai Airport alone.

|

Click here to download the India Travel Retail Report and special readers’ offer |

India’s largest airport retail survey identifies huge demand

To understand the Indian retail story in greater depth, CAPA conducted the largest research study carried out in India, involving interviewing 8,000 passengers across the ten largest Indian airports, together with more qualitative focus group involving almost frequent flyers and premium travellers.

The physical retail environment at airports is improving rapidly and will continue to do so, and the onus is now on the retailers and brands to tailor their offer to the tastes of the passenger. As identified below, there are several areas for improvement. But the key overall finding of CAPA’s research is that Indian travellers are willing and keen to spend. However, consumer behaviour is changing rapidly and as a result retail formats cannot be cast in stone and must instead remain dynamic in response to evolving trends.

Some of the key findings of the research included the following:

Promotion: Passengers have limited awareness of the products and services available in the retail area, resulting in missed sales opportunities;

Product: Passengers feel that the range of products is limited (there is a view that alcohol, fragrances and books predominate) and the following categories could be expanded:

• Children’s products;

• Affordable brands and not just premium products;

• Indian products e.g. souvenirs, clothing, spices, tea, incense, sweets, foodstuffs, mangos, jewellery, handicrafts, for foreign tourists as well as Indian travellers purchasing gifts for friends and family overseas;

• Lifestyle, travel accessories and sports goods;

• Mobile sim cards on arrival for visitors.

Market Segments: The following traveller categories are expected to be strong growth markets and perceive that they are not well catered for, namely female travellers and young independent business travellers;

Sense of Place: Foreign tourists expressed disappointment that the retail precincts in the new Indian airports are largely undifferentiated from airports around the world. This relates not only to the product offer as mentioned above, but also the overall ambience and physical environment, an opportunity exists to create a unique feature and interest by introducing an “˜Indian bazaar’ theme;

Price: Greater visibility of discounts and promotions would make shopping more attractive;

Service: Staff were found to be poorly trained in product knowledge, sales techniques and overall service engagement.

Distractions: Lengthy immigration and security queues impact the overall experience, increasing stress, and therefore the mood of the passenger when they reach the retail area, and reducing the time available for shopping;

Peace of Mind: Customers worried about after sales service and redressal related to products purchased at airports;

Business: Corporate travellers would be willing to pay for access to premium lounges (where their class of travel does not permit automatic access) but facilities and space are limited;

Seniors: Elderly travellers and those with disabilities – often with significant ability to spend – are not able to take advantage of retail offer due to assistance services taking them direct to the gate.

Domestic: Passengers would be interested in purchasing duty paid products such as alcohol in domestic terminals due to the convenience factor.

Food & beverage: There has been a dramatic improvement in the range and quality of food and beverage outlets at Indian airports in recent years. However in some cases the offer at the domestic terminals has been neglected and can be very crowded during peak hours, especially at Mumbai.

Further growth potential in developing land banks

While retail formats have received attention, to date there has been limited focus and innovation with respect to land and property development, which reflects a further growth opportunity that has not yet been aggressively pursued. Greenfield airports at Hyderabad, Bangalore and Cochin have the largest land banks and the greatest potential to monetise these assets.

Hyderabad has arguably been the most successful in developing a broad range of commercial activities including an airport hotel, an aviation training centre, an MRO, a special economic zone and specialist infrastructure for pharmaceutical shipments. Future plans include the establishment of an entertainment park and a hospital complex to support medical and wellness tourism. Hyderabad has the advantage of a large land bank of up to 1500 cares available for commercial development, compared with just 250 acres at Delhi and 200 acres at Mumbai.

However, in developing commercial and property activities it is important that airports pursue a thoughtful and differentiated strategy with respect to the market segments that they target, CAPA noted. If all airports develop similar competing strategies to each develop for example an MRO, a training centre and an aerospace manufacturing park, this may lead to overcapacity and may make it challenging to leverage the value in the land banks.

Non-Aeronautical Revenue will be essential to support investment

CAPA projects that Indian airport traffic will triple to 450 million by 2020 requiring US$30 billion of investment in airport infrastructure. It will be necessary to develop revenue models that will make such investments viable and aeronautical revenue alone will not be sufficient.

Over the last five years PPP airports have been successful in driving sharp increases in non-aeronautical revenue and the indications are that there remains further growth potential in both retail and commercial activities. With a new commercially focused approach, the AAI would also be in a position to replicate this growth.

To maximise non-aeronautical revenue, airports must carefully segment their retail and commercial customer base and develop appropriate strategies for each of them based on extensive research of their complex, differentiated and evolving requirements.

Advertisement | |