SWITZERLAND/CHINA. The investment community has reacted favourably to this morning’s big news that Chinese aviation-to-hospitality giant HNA Group has acquired a 16.79% holding of Swiss travel retail giant Dufry.

The stake is believed to have been acquired from Singaporean wealth funds GIC and Temasek. The purchase price included a “low double-digit premium” and was subject to increase “in case of certain events”.

“Ultimately we see a friendly takeover” – Kepler Cheuvreux Equity Research

HNA Group had to make a public disclosure once it reached a 3% holding. However, the Swiss take-over code means that a mandatory offer for the whole company is not triggered unless a stake larger than 33.33% changes hands.

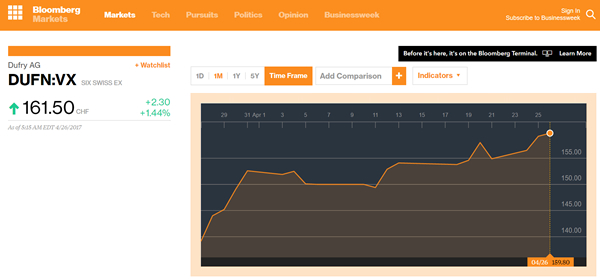

Dufry stock was up +163% to CHF161.80 by 12.30on the Swiss Stock Exchange.

Analyst reaction was generally favourable, with some believing that a full take-over bid would follow.

![]() In a note Kepler Cheuvreux Equity Research said: “We expect HNA to take a board seat and work with Dufry in developing business at its own operations and potentially in the duty free market in China. Ultimately we see a full takeover. Buy.

In a note Kepler Cheuvreux Equity Research said: “We expect HNA to take a board seat and work with Dufry in developing business at its own operations and potentially in the duty free market in China. Ultimately we see a full takeover. Buy.

“We presume that HNA will take a seat on the board and look to work with Dufry on developing retail and duty free within its existing operations. We see it working with Dufry to also open up the China duty free market, currently controlled by China Duty Free and Sunrise, two local companies with close ties to the state.

“However, while HNA has just [sometimes] taken stakes (25% stake in the Hilton group), it has mostly acquired companies and we ultimately believe HNA would look to buy Dufry in a friendly takeover.

“Given Dufry’s shareholder pact (management/board/former owners of companies acquired by Dufry) controls 18.4%, we don’t believe a hostile takeover would be likely. We assume that a price around WDF’s 13.8x EV/EBITDA multiple would be appropriate (CHF200 on 2017E, CHF235 on 2018E, CHF265 on 2019E).”

“With the shares already up 14.5% since the first press reports of an HNA interest on 28 March, and no announcement beyond the minority stake today, we would not get involved here” – JP Morgan Cazenove

![]() JP Morgan Cazenove said: “Recent press reports that HNA aims to become Dufry’s largest shareholder would suggest another c. 2.7% of capital to be acquired, which could support the price. But with the shares already up 14.5% since the first press reports of an HNA interest on 28 March, and no announcement beyond the minority stake today, we would not get involved here.

JP Morgan Cazenove said: “Recent press reports that HNA aims to become Dufry’s largest shareholder would suggest another c. 2.7% of capital to be acquired, which could support the price. But with the shares already up 14.5% since the first press reports of an HNA interest on 28 March, and no announcement beyond the minority stake today, we would not get involved here.

“The same press reports also described HNA’s aim as “to become [Dufry’s] largest shareholder”. With the Travel Retail Investments-led consortium today holding 19.46% of voting rights, this suggests HNA could need to purchase at least another c. 2.7% of capital / 1.46m shares.

“No price disclosed, other than “a low double-digit premium”: The same press reports mentioned HNA was ‘discussing a sizeable premium’ with potential sellers. We note Temasek, GIC, and QIA all entered Dufry’s capital in June 2015 as part of the CHF2.2bn capital increased for the acquisition of World Duty Free, which closed at a price of CHF136.16. Indicatively, the stake acquired today (9.05m shares) and has a market value of c. CHF1,440m at yesterday’s close price of CHF 159.2.

“No indication of a bid for 100% of the company at this stage: Across its other participations in the hotel, travel, and leisure universe that we are aware of, HNA holds a combination of minority stakes and full ownerships: 25% in Hilton Worldwide Holdings, 29.5% in NH Hotels, 100% of gate Group, 100% of Carlsson Hotels, and currently bidding for 100% of Rezidor.”

“HNA holds a strong portfolio of stakes in different companies from the fields of aviation, hospitality, tourism. Therefore, Dufry as the world’s leading duty free retailer… fits to this strategic portfolio ” – Baada Helvea Equity Research

![]() Baada Helvea Equity Research said: “Share price supporting news: HNA could be interested in increasing its stake beyond 17% and could continue to buy shares via the market.

Baada Helvea Equity Research said: “Share price supporting news: HNA could be interested in increasing its stake beyond 17% and could continue to buy shares via the market.

“HNA holds a strong portfolio of stakes in different companies from the fields of aviation, hospitality, tourism. Therefore, Dufry as the world’s leading duty free retailer (24% market share), generating around 90% of its sales at airports, fits to this strategic portfolio in order to benefit from the structural growth (especially in Asia) of passenger and flight traffic, tourism and higher spending power of the growing (Asian) middle-class.”

The firm listed Dufry’s shareholder structure(so far):

– Travel Retail Investments (private family offices), Hudson Media and Folli Follie Group: 20.7%,

– Temasek (Singapore-based investment company): 8.6%

– GIC (Singapore Government): 7.8%

– Qatar Holding: 6.9%,

– BlackRock 3.1%.

Click on image to enlarge

**BACKGROUND

As reported, Chinese aviation-to-leisure giant HNA Group approached Dufry’s sovereign wealth fund shareholder GIC and fellow Singaporean fund Temasek in March regarding an investment in the world’s biggest travel retail company.

Reliable sources in the investment community confirmed that approach to the Moodie Davitt Report. The Wall Street Journal reported news of the approach earlier that week.

The two Singaporean funds collectively held over 16% of Dufry stock.

As reported, HNA Group had to make a public disclosure once it reached a 3% holding.

However, the Swiss take-over code means that a mandatory offer for the whole company is not triggered unless a stake larger than 33.33% changes hands.

Until now Dufry had received no communication from HNA, causing uncertainly in the investment community about the Chinese group’s intentions. A hostile takeover would be extremely difficult to achieve given the structure of Dufry’s shareholding and Chinese limitations on foreign investments, and seems unlikely anyway given HNA’s deal-making history.

Sources believed originally that a likelier scenario was that HNA is seeking to extend its presence in the travel services chain with a position of significant influence in the world’s largest travel retail company. Such a position would have the additional benefit of making it ultra-difficult for any other outside party to gain control of Dufry in future. That spectre has now emerged with today’s big breaking news.

Piecing together a jigsaw puzzle When it reported HNA Group’s US$6.5 billion bid for a 25% stake in the Hilton hotel chain last October, the Financial Times (FT) said the deal “cemented its reputation as one of China’s most acquisitive groups”. In under two years the privately controlled company had announced foreign and domestic transactions worth over US$33 billion (see acquisition trail below), the FT noted — half spent offshore, according to data provider Dealogic — as it forged a global empire with interests spanning aviation, logistics and tourism. The FT commented: “Begun in 1989 as a private airline on the tropical island of Hainan, HNA’s buying spree shows no sign of slowing. Founder Chen Feng, a former employee of China’s state civil aviation administration, has transformed Hainan Airlines, the group’s flagship company, from a two-jet operation into the country’s fourth-largest airline and has built a sprawling conglomerate. “While Mr Chen has largely ceded control of the group’s day-to-day operations to his co-chairman, Wang Jian, and chief executive Adam Tan, the Hilton acquisition is a key piece of his plan to profit from Chinese tourists as they travel around the world.” The FI cited a source close to HNA saying, “The vision is to be a vertically integrated aviation and tourist group. They are buying different pieces and putting it together like a jigsaw puzzle.” Not only is HNA acquiring a large piece of Dufry but also, it appearsa, another key piece of that puzzle. |

From The Moodie Davitt Report May Print Edition, out in coming days I’m not normally one for predictions but I’ll make one here. The acquisitive, Hainan-based conglomerate HNA Group has pulled off a flurry of major acquisitions in recent times and I believe travel retail will be among its next power plays. The Moodie Davitt Report has confirmed that HNA has indeed been in communication (as originally touted by the Wall Street Journal) with Dufry’s two Singaporean wealth funds GIC and Temasek. As we went to press, Dufry had not been contacted by the Chinese group, causing uncertainly in the investment community about HNA’s intentions. A hostile takeover would be extremely difficult given the structure of Dufry’s shareholding and seems unlikely anyway given HNA’s deal-making history. Informed sources believe a likelier scenario is that HNA is seeking to extend its presence in the travel services-to-hospitality chain (it already owns gategroup; Carlson Hotels; a 25% stake in Hilton Worldwide Holdings; CIT Group’s aircraft leasing business; 13% of Virgin Australia; 23.7% of Azul Brazilian Airlines; and airport luggage handler Swissport International). By taking a position of significant influence in the world’s largest travel retailer it would be strongly placed to shape the company and the sector in the future – as well as making it very difficult for any other outside party to gain control of Dufry. Don’t forget either that at its 28 October 2016 board meeting, CDFG parent China International Travel Service voted to create a joint venture with Hainan Duty Free. And Hainan Duty Free (full name HNDF Haikou Meilan Airport Duty Free Shop) is a provincial government and private partnership between Hainan Provincial Duty Free Company Limited and none other than HNA Group. Just think of the possible permutations among that network of relationships. |

*HNA’S ACQUISITION TRAIL

Dufry operates around 2,200 duty free and duty paid shops in airports, cruise lines, seaports, railway stations and downtown tourist areas.

The Swiss retailer employs close to 29,000 people. The company, headquartered in Basel, Switzerland, operates in 64 countries in all five continents.

Chinese conglomerate HNA Group has been very active in recent times in making acquisitions across its fields of interest with aviation and aviation-related services central to the expansion. Here is a selected timeline of some of its main deals:

- December 2016: As reported, HNA completes acquisition of gategroup, the Swiss inflight services provider, in a transaction valued at CHF1.4 billion (US$1.47 billion).

- December 2016: Completes acquisition of IT products and services company Ingram Micro through subsidiary Tianjin Tianhai Investment Company. The all-cash transaction is for US$38.90 per share with an equity value of approximately US$6 billion.

- December 2016: Closes deal to acquire Carlson Hotels through subsidiary HNA Tourism Group. Also acquires Carlson’s 51.3% stake in Brussels-based Rezidor Hotel Group.

- October 2016: China Duty Free Group parent company China International Travel Service votes at its board meeting on 28 October to create a joint venturewith Hainan Duty Free.

- October 2016: Announces intention to purchase a quarter of Hilton Worldwide Holdings Inc. for US$6.5 billion.

- October 2016: Buys CIT Group’s aircraft leasing business for US$10 billion.

- May 2016: Agrees to purchase 13% of Virgin Australia for US$114 million, with plans to raise that stake to about 20%.

- March 2016: Increases stake in Deutsche Bank from 3.04% to 4.76%.

- March 2016: Acquires Manhattan’s 245 Park Avenue skyscraper for US$2.21 billion.

- November 2015: Agrees to buy 23.7% stake in Azul Brazilian Airlines for US$450 million through subsidiary Hainan Airlines.

- July 2015: Agrees to buy airport luggage handler Swissport International from PAI Partners for US$2.81 billion.