INTERNATIONAL. As war in the Middle East constrains global air capacity, passenger flows are shifting, placing pressure on the region’s hubs while Southeast Asia largely benefits from the diverted demand.

That is according to the latest findings from leading travel data provider Official Airline Guide (OAG), presented during a webinar on 25 March.

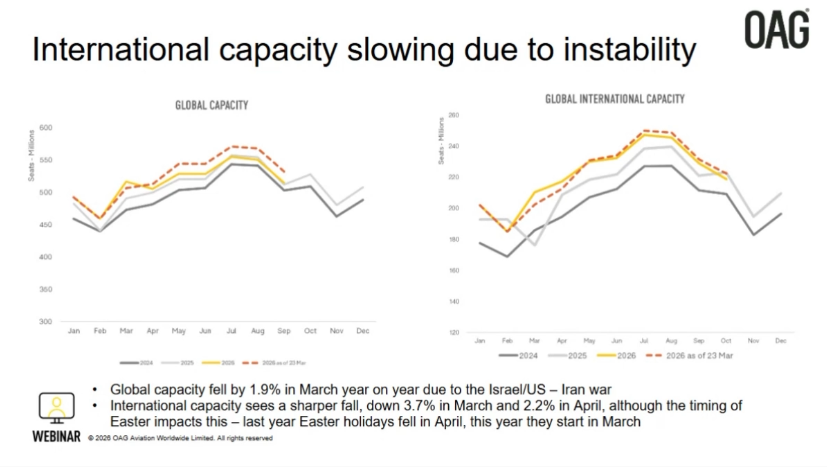

The report highlighted a -1.9%year-on-year drop in global air capacity in March, driven by the escalating Israel/US-Iran conflict.

The latest analysis reveals a deeper decline in international capacity, down -3.7% in March and projected to dip -2.2% in April, with analysts attributing the shift in part to the earlier timing of Easter this year.

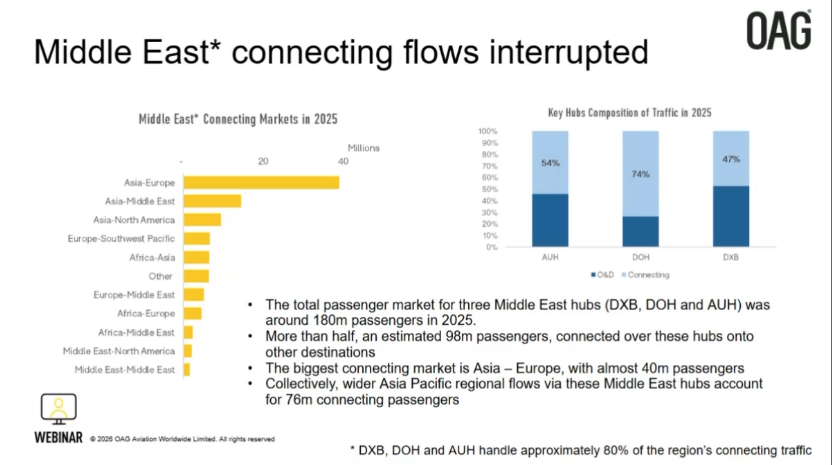

These trends reflect the important role of Middle East hubs in global connectivity.

The three major Middle East airports, Dubai International, Hamad International in Doha and Zayed International in Abu Dhabi, served approximately 180 million passengers in 2025.

Of these, more than half (an estimated 98 million) were connecting travellers, with the Asia-Europe market alone accounting for nearly 40 million.

While major Middle East airlines continue to maintain operations, some international airlines have temporarily suspended their services to the region.

In his latest report, OAG Chief Analyst John Grant noted, “Forty-four airlines that had planned to operate from the Middle East in the last week of February have removed all capacity through to the end of April, collectively accounting for some 245,000 seats a week.

“Looking forward to the end of May, several airlines have dropped significant capacity from the Middle East; Wizz Air has cancelled over 450 flights and British Airways 266 flights that were scheduled to operate and loaded for sale at the end of February.”

The shift to Southeast Asia

Citing a latest survey by Pear Anderson and the Association of Southeast Asian Nations Tourism Associations (ASEANTA), OAG highlighted a significant shift in traveller behaviour and business sentiment.

Business confidence has softened as nearly half (48%) of Southeast Asian travel businesses said their Q2 2026 prospects are worse than expected at the start of the year due to the impact of the Middle East conflict.

Traffic redirection is also emerging as a key trend, with the ASEANTA survey showing that 72% of businesses report postponements or cancellations for Middle East travel, and 70% for Europe – reflecting the region’s role as a major hub between Southeast Asia and Europe.

As a result, travel businesses anticipate demand will move towards travel within Southeast Asia (64%) amid the escalating conflict, while Europe (24%) remains a preferred destination despite flight disruptions.

Cancelled flights, airport closures and other logistical constraints (46%) are seen as the main reasons for cancellations and postponements, with client decisions (40%) also influencing travel patterns.

The disruption does not only affect outbound routes, as inbound travel to Southeast Asia for March and April was also impacted by ongoing tensions. Travel businesses noted that at least some trips were either cancelled or delayed from the Middle East (62%) and Europe (67%).

Amid these conditions, travel businesses report challenges including rising fuel prices and flight connectivity disruptions, but also highlight the resilience of the tourism industry and Southeast Asia’s potential to emerge as an alternative transit hub.

Regional resilience

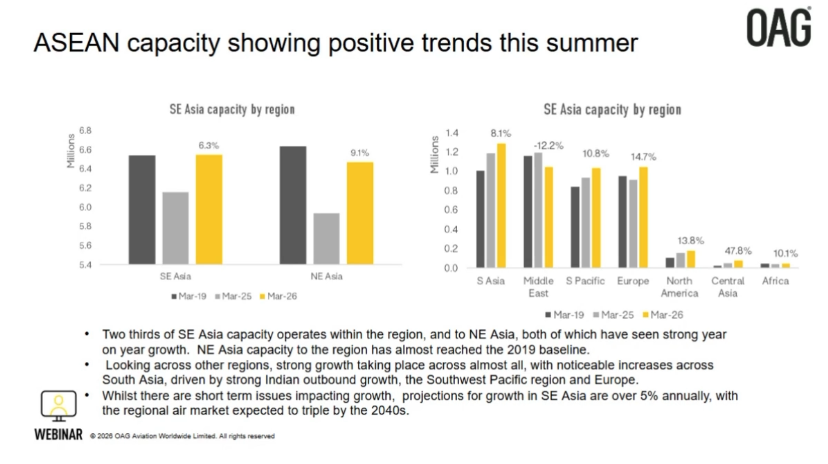

Even with near-term headwinds, Southeast Asia’s aviation sector shows positive trends, with around two-thirds of capacity operating within Southeast Asia or to Northeast Asia. Both segments continue to post strong year-on-year growth, while Northeast Asia capacity is nearing pre-pandemic 2019 levels.

Across other regions, nearly all markets indicate strong growth, led by South Asia on the back of rising Indian outbound demand, as well as Southwest Pacific and Europe.

Despite short-term challenges, Southeast Asia is projected to grow at over +5% annually, with the regional air market expected to triple by the 2040s.

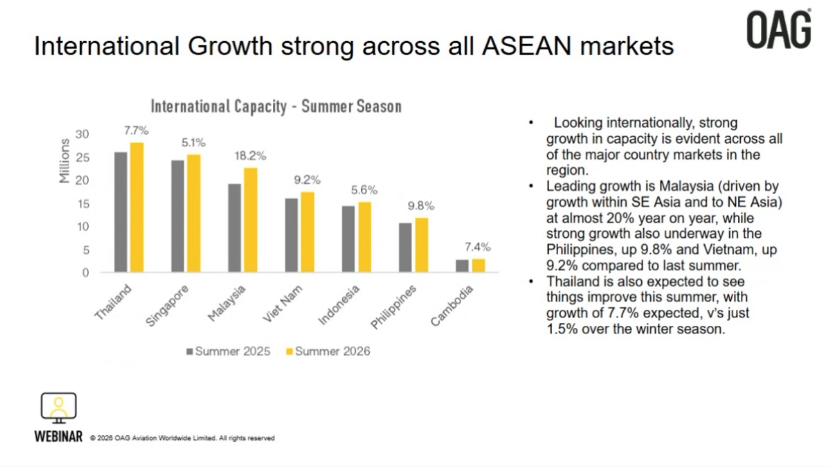

Among individual markets, Malaysia is driving international growth with nearly +20% year-on-year increases, boosted by demand from Southeast Asia and Northeast Asia.

The Philippines and Vietnam continue to show strong momentum, up +9.8% and +9.2% respectively, while Thailand is expected to recover to +7.7% growth following a softer winter performance of 1.5%.

Domestic market results vary, led by the Philippines and Thailand, which posted robust growth of +20.6% and +15.5%, respectively.

Vietnam currently lags in terms of domestic growth, even after posting a +10.4% increase in Winter 2025, suggesting potential uplift as the season progresses.

The region’s largest domestic market, Indonesia, has returned to growth this summer, with a projected +5.2% increase in Summer 2025 following a -1.6% decline during winter.

These five markets comprise 99% of domestic capacity in the region.

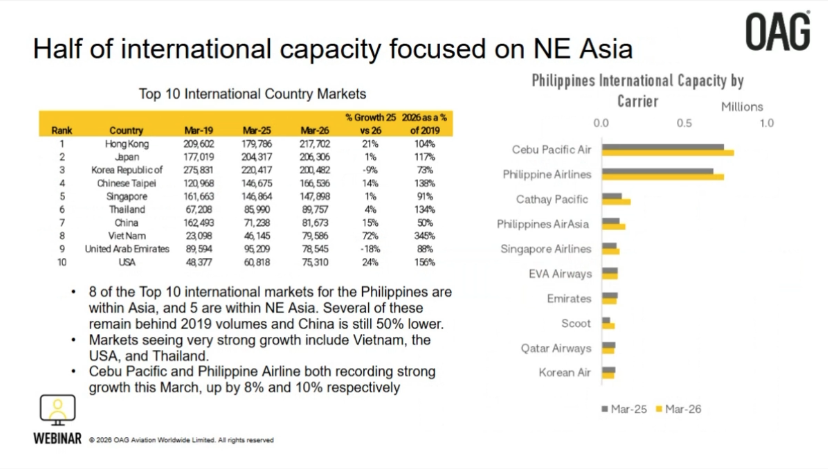

The findings further show that half of international capacity is focused on Northeast Asia.

In the Philippines, eight of the top ten international markets are within Asia, with five in Northeast Asia. But recovery is uneven as several markets remain behind 2019 levels, with China down roughly 50%.

Vietnam, the US and Thailand are among the markets driving strong growth.

Cebu Pacific and Philippine Airlines both recorded improvement in March, rising +8% and +10%, respectively.

Grant concluded, “For the aviation industry, the current situation is, in many respects, a familiar one: challenges that have to be faced with everyone hoping for a swift resolution and a return to normal schedules as quickly as possible.

“For the locally based airlines, once there is any resolution scheduled services will return to normal very quickly and that powerful connectivity once again back in place.

“For the overseas airlines operating to the Middle East, the return might be more cautious; for some, that could mean a period of months rather than weeks before services are reinstated. But return they will.” ✈