Global consulting firm Oliver Wyman has outlined three key trends set to shape the next decade of growth in Asia Pacific travel retail as the industry moves beyond “years of turbulence”.

Findings from the consultancy’s latest research were presented at TFWA Asia Pacific Exhibition & Conference in Singapore.

Tax Free World Association Managing Director Franck Waechter said, “The findings of this joint TFWA and Oliver Wyman study arrive at a defining moment for travel retail in Asia Pacific.

“While recovery is clearly underway, the report also highlights a more fundamental reality: the industry is no longer navigating a temporary disruption, but adapting to a structural reset in how consumers travel, shop, and engage with brands.

“Volatility is no longer an exception to manage around – it has become a permanent operating environment. Geopolitical tensions, shifting aviation dynamics, changing tourism patterns, and evolving consumer expectations are reshaping the foundations of the sector.

“In this context, growth cannot rely solely on the return of historical traveller flows or the gradual normalisation of demand. One of the most important conclusions of this study is that travel retail now faces a strategic choice.”

The study identified the next set of travellers that will fuel the region’s travel retail growth; the reasons behind this, and what brands and operators need to do to unlock these missing opportunities; and the role of AI and innovation to fuel the next decade of growth in Asia Pacific.

Drawing on ten years of research into Asian traveller and luxury shopper behaviour and spending, the report consolidates travel retail experience, proprietary consumer research and executive perspectives.

These are complemented by the latest 2026 survey of 2,250 consumers in Mainland China and India, insights from more than 40 senior executives, and learnings from ten luxury client projects across APAC over the past 12 months.

Chinese, Indian and Korean travellers: Driving the next decade of travel retail growth

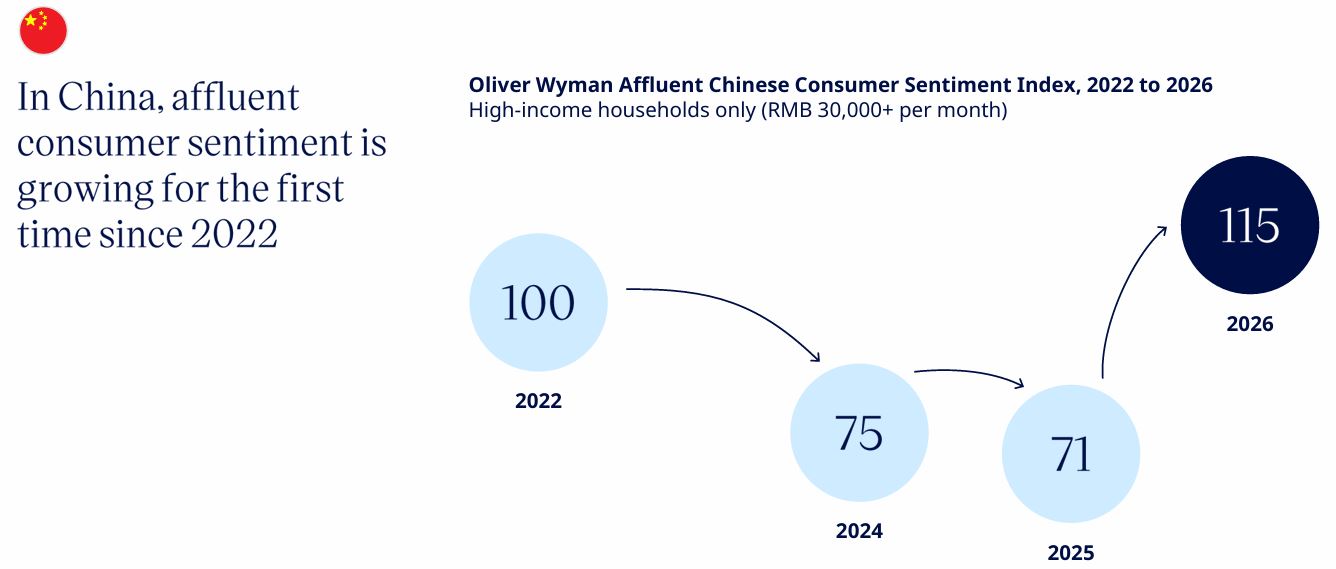

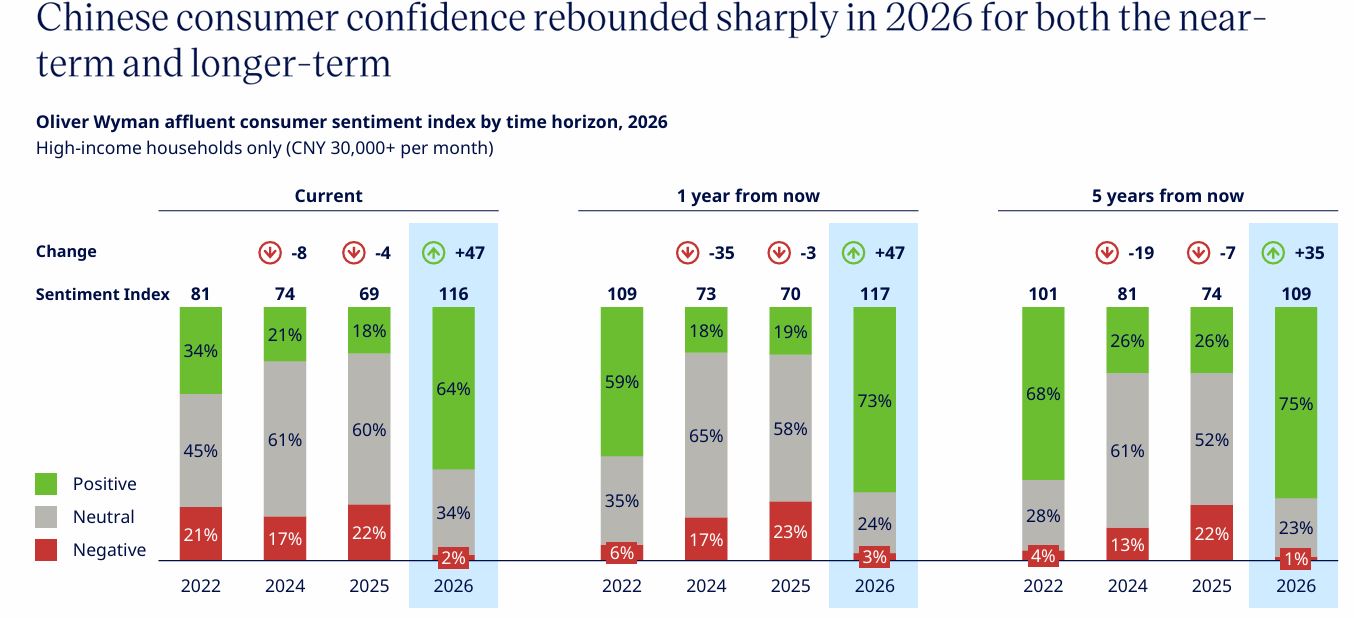

A clear inflection point in affluent consumer sentiment in China has emerged for the first time since 2022, with the index rebounding from 71 in 2025 to 115 in 2026.

This rebound signals more than a psychological recovery, translating into measurable gains in spending and travel intent.

Overseas travel demand is on a rise, with a net 44% of affluent households expecting to travel more internationally, up 47 percentage points from the previous year. Luxury spending intentions are also improving, with a net 31% planning to spend more on luxury, up 37 percentage points year-on-year.

The findings point to a heterogeneous growth pattern, marked by structural divergence across categories and cohorts.

Beauty & fashion are gaining momentum, but watches & jewellery remain soft.

Across age groups, baby boomers, rather than younger consumers, have been identified as the primary drivers of growth, raising questions about the long-term sustainability of Chinese luxury travel spend.

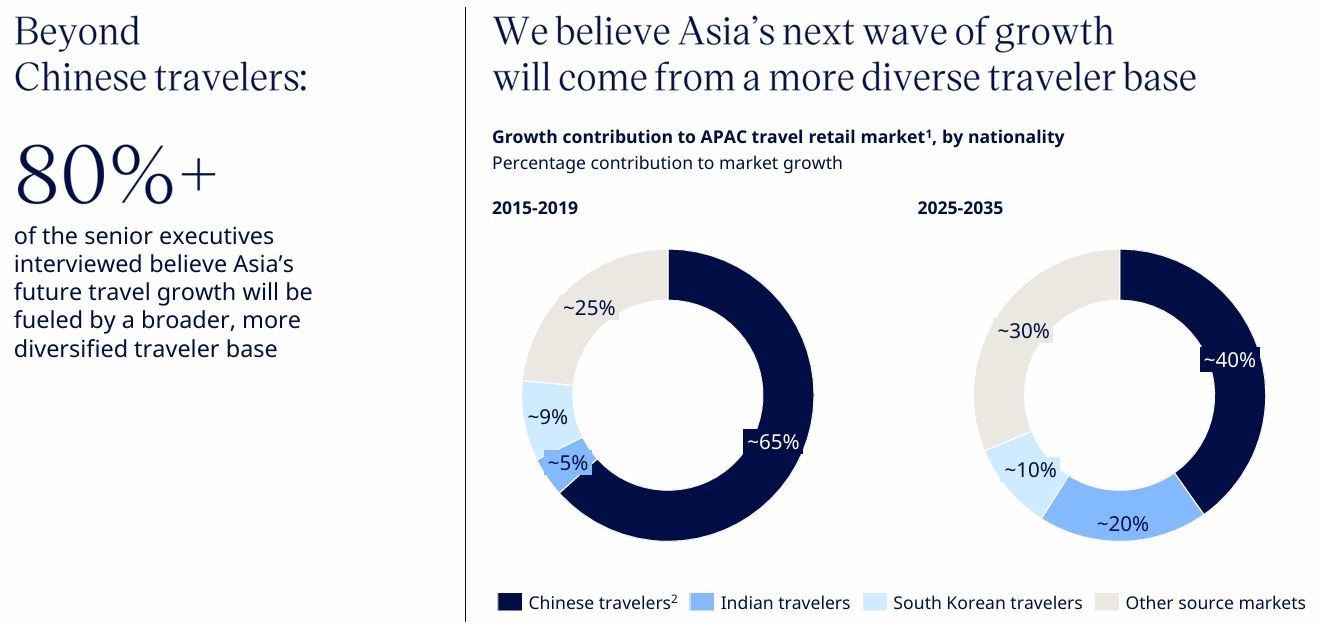

The research highlights a shift in the regional growth engine over the next decade, with Chinese travellers continuing to play a key role in growth, even as their market share is forecast to ease from around 65% historically to approximately 40%.

Indian and Korean travellers are expected to emerge as the next important growth drivers, accounting for a larger share of future expansion at 20% and 10%, respectively. Both segments demonstrate diverse needs, spending patterns, category preferences and service expectations.

This evolution prompts the need for brands and operators to adopt a hyper-dynamic model that moves beyond a China-led approach and adapts propositions, ranging from assortment and activation to service and operations, to a more diverse and rapidly evolving traveller base.

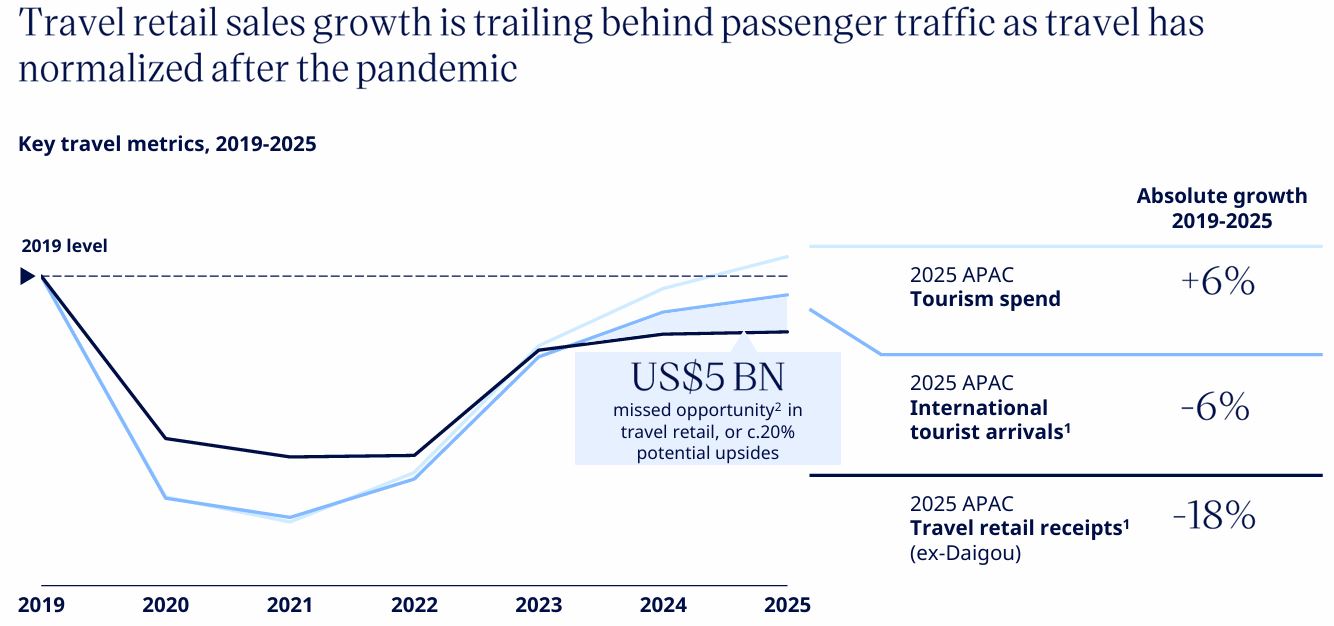

Turning US$5 billion in lost potential into growth

The study highlights the need for brands and operators to radically transform their propositions and operating models to stay competitive.

This is evident in APAC travel retail, capturing only around 71% of footfall growth and 67% of tourism spend growth since border reopening, resulting in an estimated US$5 billion in untapped value.

The report identifies two primary catalysts for the performance shortfall.

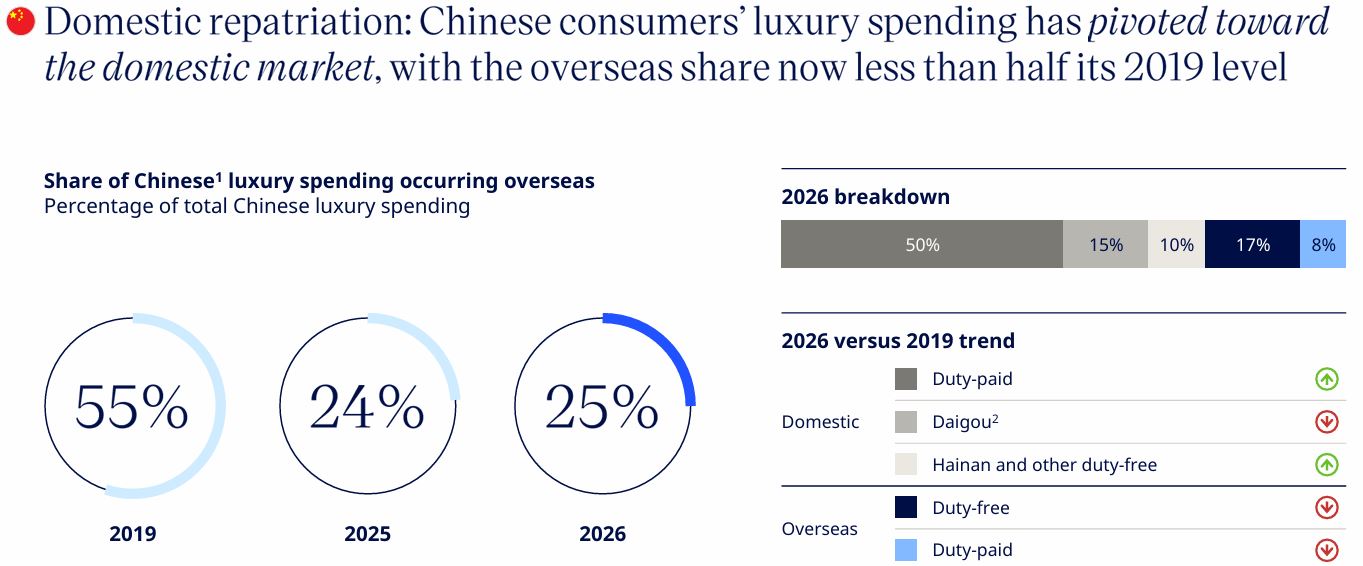

The first is domestic repatriation, as luxury spend continues to shift into domestic channels. The overseas share of Chinese consumers’ luxury spend has more than halved since 2019, driven by stronger domestic retail propositions, the rise of Hainan and changing travel purposes.

On the other hand, stagnant value propositions mean airport retail is simply “not compelling enough” to convert footfall into spend growth.

While conversion and spend growth in Asia’s airports has trailed global peers, the research highlights opportunities for brands and operators to maximise quality time with travellers, evolve beyond price-led propositions, and respond with greater flexibility to diverse traveller needs.

Successful brands are already demonstrating a clear approach to capturing opportunities.

This is built on localised exclusivity, offering region-specific purchase drivers that domestic markets cannot replicate.

End-to-end engagement ensures brand presence across the full traveller journey beyond the store.

It is underpinned by collaborative intelligence, where structured data-sharing between brands, retailers and airports drives precision conversion and operational synergy.

Innovation and AI

AI and innovation are set to redefine travel retail over the next decade.

Among senior executives, 76% view them as critical to sustaining growth, particularly in improving traveller experience, conversion and operational efficiency.

Yet there is a disconnect, as only 40% rank AI innovation as a top investment priority, despite recognising its importance.

AI adoption remains early and largely focused on back-of-house use cases, although customer-facing applications are approaching an inflection point, particularly in personalisation, CRM and targeted offers.

Currently, just 7% of executives have deployed these solutions, but 53% plan to do so within 12 months.

The broader strategic shift is that AI will play an increasing role in shaping traveller decisions before and during the journey, influencing trip planning, brand discovery, product recommendations and spend allocation.

To remain competitive, travel retailers and brands are urged to start becoming AI-ready. This requires accuracy and consistency across product information, pricing, availability and brand positioning, ensuring these elements are delivered in real time across digital and AI-enabled touchpoints. ✈