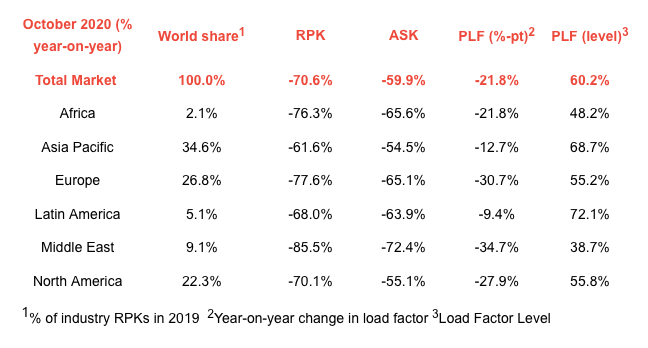

INTERNATIONAL. The International Air Transport Association (IATA) has described the recovery of passenger demand as “disappointingly slow” in October, with revenue passenger kilometres (RPKs) down -70.6% against the same month in 2019.

This represented a modest improvement from the -72.2% year-to-year decline recorded in September. Capacity was down -59.9% compared to a year ago and load factor fell -21.8 percentage points to 60.2%.

The bleak picture for international passenger demand continued in October, down -87.8% against the corresponding month last year. This gave a very slight improvement on the -88.0% year-to-year decline recorded in September. Capacity was -76.9% below previous year levels, and load factor fell by -38.3 percentage points to 42.9%.

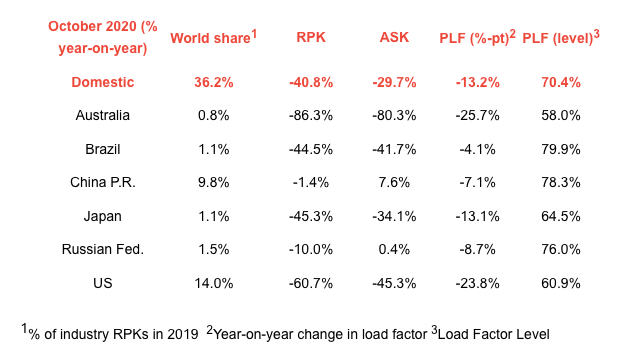

Domestic passenger offered a brighter picture with traffic (in RPKs) down -48% year-on-year in October. This compared to a -43.0% year-on-year decline in September. Capacity was -29.7% below 2019 numbers and the load factor dipped -13.2 percentage points to 70.4%.

IATA Director General and CEO Alexandre de Juniac said: “Fresh outbreaks of COVID-19 and governments’ continued reliance on heavy-handed quarantines resulted in another catastrophic month for air travel demand. While the pace of recovery is faster in some regions than others, the overall picture for international travel is grim.”

He added: “This uneven recovery is more pronounced in domestic markets, with China’s domestic market having nearly recovered, while most others remain deeply depressed.”

On the international front, Asia Pacific airlines were hardest hit, with October traffic collapsing -95.6% compared to the year-ago period. This figure was unchanged from September. Capacity plunged -88.5% and load factor fell away -49.4 percentage points to 30.3%, the lowest among regions.

European carriers’ October demand sank -83.0% versus a year ago, following on from a -81.2% decline in September. For a second consecutive month, Europe was the only region to experience a deterioration in traffic. Capacity fell -70.4% and load factor fell by -36.7 percentage points to 49.5%.

Middle Eastern airlines saw an -86.7% traffic drop for October, improved from a -89.3% fall in demand in September. Capacity plummeted -73.6%, and load factor fell -36.6 percentage points to 37.0%.

North American carriers’ traffic shrank by -88.2% in October, but this did represent a slight improvement from a -91.0% decline in September. Capacity fell -73.1%, and load factor dropped -46.2 percentage points to 36.2%.

In the Latin America market, airlines suffered an -86.0% demand drop in October, compared to the same month last year. The region did, however, show the greatest improvement on September when year-on-year demand was down -92.3%. October capacity was -80.3% down and load factor dropped -23.5 percentage points to 57.7%.

The smallest relative loss among the regions was recorded by African airlines, with traffic sinking -78.6% in October, improving on a -84.9% drop in September. Capacity contracted -67.5%, and load factor fell 23.8 percentage points to 45.5%.

In the domestic air passenger market, China’s traffic was down just -1.4% in October compared to the same period a year ago. IATA partly attributed the encouraging result to low fares and ‘all you can fly’ deals alongside the recovering economy.

Meanwhile, Russia’s domestic traffic slipped back into negative numbers in October, down -10% after two months of growth. IATA observed that COVID-19 cases have taken their toll on travellers’ confidence, despite few domestic travel restrictions being in place.

Describing the current crisis as “unrelenting”, de Juniac said: “Our latest economic outlook is for airlines to lose US$118.5 billion this year, or US$66 for every passenger carried. Assuming borders re-open by mid-2021, the industry will ‘only’ lose US$38.7 billion in 2021.

“Now is the time for governments to step up. The US$173 billion of support provided to date has enabled the industry to survive, but more is required to carry the industry through to next summer. IATA has identified a range of market stimulation options that will support the viability of air routes while encouraging people to travel. Without aviation’s US$3.5 trillion contribution to global GDP, there can be no broader economic recovery.”