The inter-related but contrasting fortunes of North Asian travel retail and the Mainland China local market were the subject of discussion on L’Oréal’s earnings call yesterday (21 October) following the French beauty house’s Q3 and nine-month results announced earlier (click here for our story).

CEO and Director Nicolas Hieronimus described the North Asia market in its entirety as “a mix of different situations”.

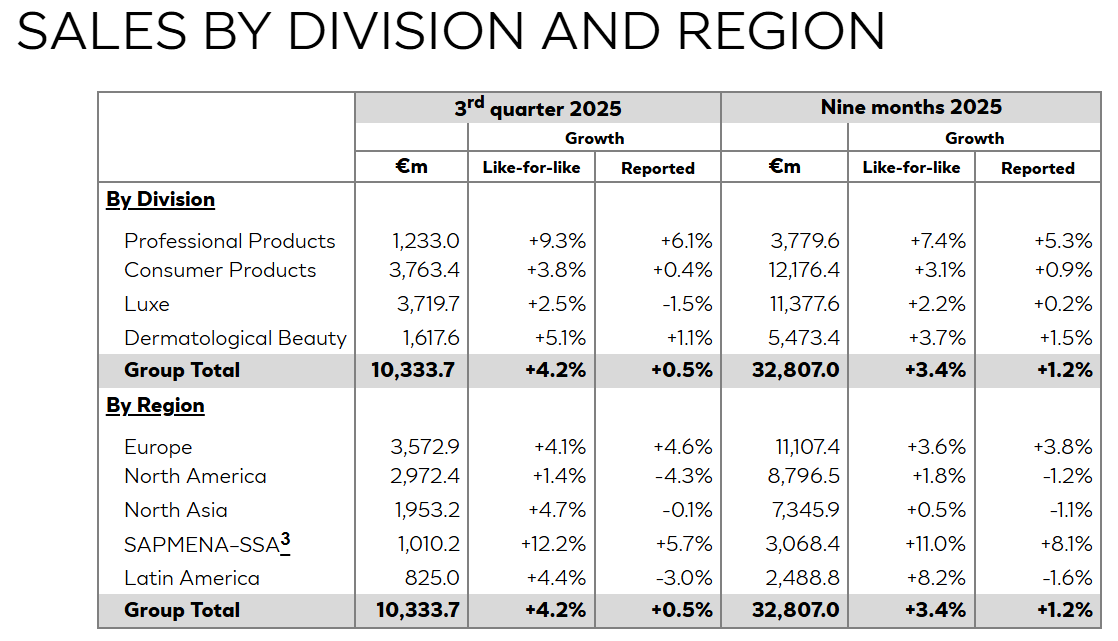

He said Mainland China (domestic) is “going in the right direction” with the market at +1% year-to-date after a flattish first half. L’Oréal’s Q3 performance was around +3%.

“I’m always very careful about China because one quarter doesn’t make a trend but overall, the market has gone into positive territory,” he commented, noting the best performance was coming from the group’s luxury beauty brands.

“We see slight uptick in consumer confidence. We see a stock market that has come back to the 2019 level, which is good for luxury consumers morale. But I wouldn’t get over excited because there are other macro-employment statistics that are not as positive,” Hieronimus continued.

Downturn doldrums, airport advancement

The Japanese market – boosted by strong Chinese and Korean tourism – was also in positive territory, he noted.

“Travel retail is improving a bit, but it remains in negative territory,” Hieronimus said. While North Asia travel retail was negative in single digits, he explained an important contrast between channels.

“As we commented in our last [H1] call, [there is] a significant difference between the downtown stores, which are double-digit negative and the airports, which are doing better. So travel retail is not positive.”

Soundbites – On the record with Nicolas Hieronimus*

|

Hieronimus highlighted the recent appointment of highly regarded Eva Yu as L’Oréal Travel Retail President, replacing Emmanuel Goulin, who has been appointed to the key role of Europe President. Yu, currently President and Managing Director of L’Oréal Hong Kong, is the first Chinese woman to head the group’s travel retail business, he said.

Talking of groupwide performance, Hieronimus said the contribution from the company’s Beauty Stimulus plan had accelerated during the reporting period. New products included the latest fragrances, Paradigme by Prada and Miutine by Miu Miu, with both off to a good start (see panel above).

He said the group’s highlights included the gradual recovery in L’Oréal’s two largest markets, Mainland China (“where we clearly outpaced the market”) and the USA, where the Consumer Products Division gained market share in each of its categories for the first time since 2021, proving that innovation really is a “game changer in beauty”.

Hair Care & Fragrances, collectively representing 30% of group sales performed well as, encouragingly, did makeup, where L’Oréal grew almost 3x above the market.

Continued dynamism in ecommerce plays to L’Oréal’s strength, enabling the company to outperform what Hieronimus described as the fastest-growing channel (story continues below the panel that follows).

(Kering) Beauté is in the eyes of the beholder

Unsurprisingly, Hieronimus dedicated much attention to L’Oréal’s acquisition, announced Sunday night, of Kering Beauté, including the Creed niche fragrance brand as well as the beauty & fragrances licences of Balenciaga, Bottega Veneta and, “when available”, Gucci.

“I’m extremely excited about this transaction. Not only does it cement our existing leadership in luxury beauty, I also see enormous potential for each one of these four brands and we have proved our ability to turn licences into billionaires,” he commented.

“Today, YSL is as big in beauty as it is in fashion. Prada crossed the €500 million mark just four years after joining the L’Oréal Luxe family. The future is now good, and I look forward to writing this new chapter. And I’m truly delighted to do it with Kering, a trusted partner for more than a decade and a half.” ✈