UK. Leading travel retailer WHSmith today (10 June) announced a trading update for the 14-week period to 6 June, with revenue climbing +5% year-on-year on a constant currency and +2% like-for-like.

The company has however revised down its outlook for the full year to reflect “the observed and anticipated decline in passenger numbers and weakening consumer demand across all divisions and a reduction in brand marketing, increased promotional activity and inflation headwinds across the group”.

Citing continuing uncertainty from the Middle East conflict and pressure on gross margins, including recent deterioration in the North America division, the company said in a statement that it expects to deliver headline group profit before tax and non-underlying items of £75 million to £90 million (US$100-120 million) in the full year. This compared to £110 million (US$147 million) in the last financial year.

The statement added: “The Group assumes no near-term improvement in consumer confidence and that jet fuel supplies can be maintained. Consistent with prior years, the Group’s trading profit is heavily weighted to the final quarter of the financial year.”

North America planning assumptions for FY26 include revenue growth of +4% to +6% and headline trading profit margin of around 5%. All other divisional trading assumptions are unchanged.

As a result of the previously announced North America InMotion review, store exit programme and Rest of the World restructuring, a non-underlying non-cash impairment charge of up to £150 million (US$201 million) for the full year relating to goodwill and store impairments is expected.

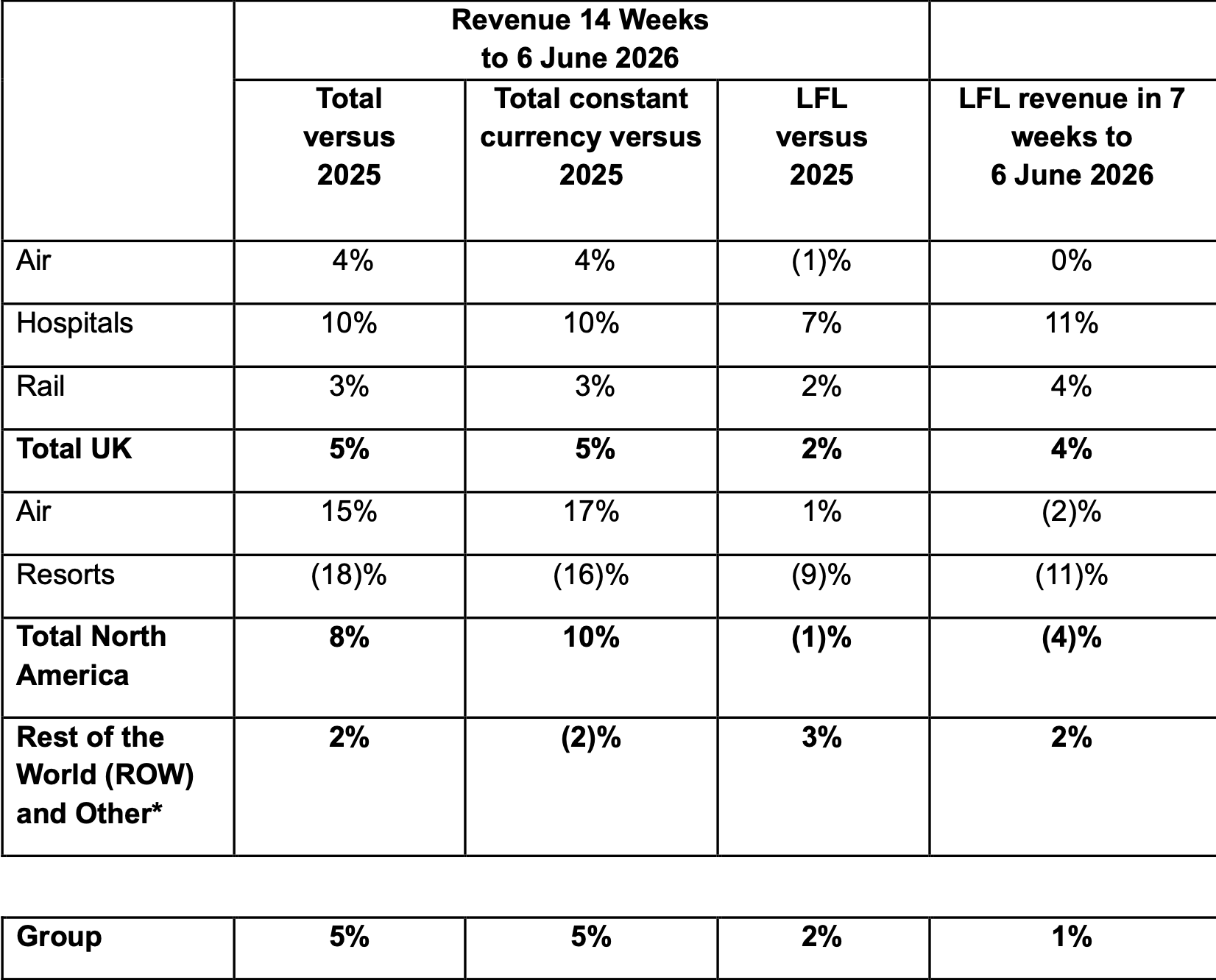

Revenue by division

In the key UK market, total revenue for the 14-week period increased +5% year-on-year, with like-for-like revenue up +2%.

WHSmith said, “Air passenger numbers continue to be impacted by disruption to Middle East flight schedules and weaker consumer confidence has impacted spend per passenger, resulting in a lower level of growth during the period.”

Like-for-like revenue in Air was down -1%, while the Hospital channel grew +7% and Rail increased +2% with a slightly improved trend in the last seven weeks, supported by softer comparatives in Hospitals last year.

The division’s one-stop-shop openings across Belfast, East Midlands, Heathrow and Liverpool airports are delivering good year-on-year growth with positive landlord and customer feedback, said the company.

Revenue in North America for the 14-week period increased +10% compared to the prior year on a constant currency basis. Like-for-like revenue in the same period was down -1%. Over the last seven weeks, like-for-like revenue declined -4%.

In Air, in the last seven weeks, like-for-like revenue decreased -2%, reflecting reduced passenger numbers following recent air fare inflation and a reduction in airline capacity linked to the Middle East conflict. This drove lower store footfall while softer consumer demand led to lower spend per passenger growth.

- Travel essentials like-for-like revenue decreased -1% over the last seven weeks;

- InMotion like-for-like revenue decreased -5% over the last seven weeks with a sharp decline in store footfall over the period. The InMotion store portfolio review continues.

WHSmith stated: “As a result of a softening in consumer demand, further promotional activity has been and will be required, while brand marketing investment is reducing and inflation headwinds continue. Together, these have resulted in gross margin pressure.”

In Resorts, like-for-like revenue decreased -11% in the last seven weeks, driven by the continued reduction in Las Vegas visitor numbers.

Further action has been taken in the Resorts segment to address underperformance, with 14 uneconomic fashion stores now either closed or with agreed closure dates. The remaining 12 fashion stores are likely to be exited in the balance of the year. The company said it is also considering strategic options for its Welcome to Las Vegas business.

In the Rest of the World, revenue for the 14-week period slipped -2% on last year on a constant currency basis and increased +3% on a like-for-like basis, reflecting the softening in passenger growth over recent weeks.

In the period, five uneconomic stores were closed in Norway. “Further landlord discussions are advancing to either exit or transition stores to a franchise model,” said WHSmith.

Proposed share placement

WHSmith also announced its intention to conduct a non-pre-emptive placing of new ordinary shares in the group. This capital raise will involve placing around 26 million new ordinary shares, which represent around 20% of the company’s existing share capital.

The Board stated that the capital raise is “in the best interests of shareholders and that raising equity is a prudent and proactive step which will strengthen the balance sheet, enable continued execution of the group’s growth and transformation agenda, provide greater confidence around the group’s leverage position, and reduce reliance on debt funding as it executes its long-term growth strategy.

“Accordingly, the capital raise is expected to reduce leverage from the current higher than targeted leverage levels to around 2x by the end of the 2026 financial year.”

The placing will be conducted through an accelerated bookbuild process to be launched immediately.

WHSmith Executive Chair Leo Quinn commented: “Early in April, we launched a far-reaching self-help programme across WHSmith. Our goal is to greatly strengthen the group’s operations while driving more effective implementation of value creation.

“The business has a strong core and operates in attractive markets with ample scope for profit expansion, particularly in North America. However, we need much greater capital discipline and a laser focus on returns. In recent years, the outcomes from certain acquired businesses and contract obligations have been very disappointing.

“Our priorities are to build an efficient and effective foundation for WHSmith and use this to drive a growth strategy managed for profitability.

“In particular, we are now taking action to sell, exit or renegotiate loss-making or low-return situations and, where appropriate, we are replacing directly-run operations with franchises in sub-scale markets. While we make meaningful progress in these areas, we must continue to invest in our core business to drive more productivity.”

He continued: “Our underlying processes and systems need upgrading to provide the data for stronger management of risk, working capital and speed of response. We are hiring the right people to deliver these changes.

“The impact of these actions will both require investment and result in a substantial non-cash write-off; but the returns to be had are clear.

“There is no doubt that current economic uncertainty and its effect on consumer appetite for spending has created headwinds. In this environment, sorting legacy issues while investing in the core model requires the financial flexibility of a stronger balance sheet in lock-step with self-help. This placing is a prudent and proactive step to accelerate our transformation of what is, at heart, a good business with some great people and clear opportunity for profitable growth.

“The consequent reduction in leverage nearer to our stated ambition of leverage below 2x will enable us to take the right actions at pace and strengthen the Group’s platform for future profit growth, all with the intention of delivering significant value upside.” ✈