INTERNATIONAL. Industry leaders warned of the far-reaching consequences of the Middle East conflict for aviation and travel retail during a webinar hosted today (10 June) by the Duty Free World Council (DFWC) and the Middle East & Africa Duty Free Association (MEADFA).

Airports Council International (ACI) World Senior Director, Economic Policy & Airport Business Slava Cheglatonyev presented data from an ACI Asia Pacific & Middle East assessment covering nine key airports in the dual region.

Passenger traffic across these airports saw a drastic shortfall of 27 million passengers during March and April, representing a -54% year-on-year decline.

“The economic impact is estimated at between US$900 million and US$1 billion in lost revenues, equivalent to a -55% decline compared with budgeted targets,” he said.

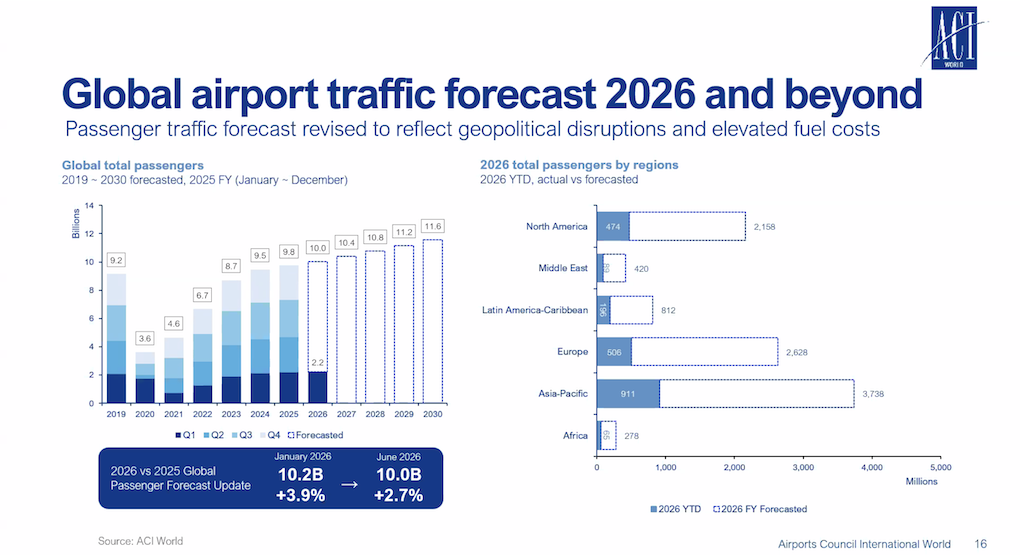

The Middle East crisis means 2026 global passenger traffic will grow just +2.7% year-on-year to approximately 10 billion, compared with a previous forecast of +3.9%.

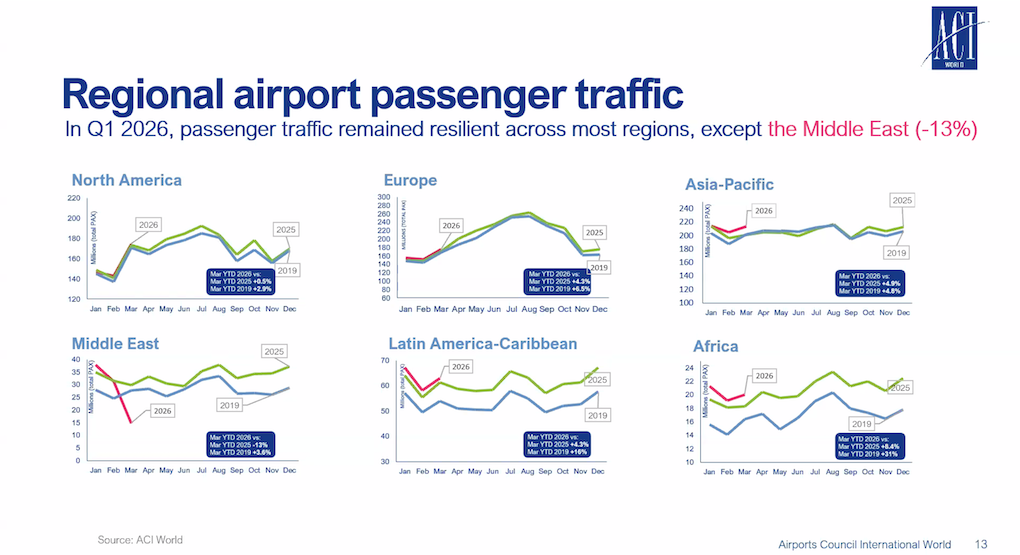

The largest adjustment concerns the Middle East, where passenger traffic is now projected to decline by around -10.5% year-on-year.

“Despite geopolitical disruptions and changing consumer behaviour, the long-term outlook for aviation remains strong and resilient,” he said. “We do not currently assume a structural change in long-term traffic growth.”

Middle East and Africa Duty Free Association President & Avolta CEO Middle East & Africa Abdeslam Agzoul described the first half of 2026 as “an exceptionally challenging period” for MEADFA members and the wider travel retail community.

He cited the 3 June drone strike on Kuwait International Airport, which killed one person and injured around 60, as a reminder of the vulnerability of transport infrastructure in the region.

Agzoul said, “Despite the disruption, operations resumed within hours, illustrating the resilience of our industry and the dedication of the people who work tirelessly to keep essential services running.”

Tourist traffic has declined sharply across several key markets, including the UAE, Oman, Qatar and Lebanon, while business travel has softened in some destinations, including Saudi Arabia.

Citing figures from UN Tourism, Agzoul noted visitor arrivals to the Middle East fell almost -14% in the first quarter of the year.

“It is certain that the figures will be much worse in quarter two,” he added.

Earlier, DFWC President Sarah Branquinho opened the session, followed by presentations from Cheglatonyev and Agzoul.

Cheglatonyev and Agzoul examined the impact of the Middle East conflict on passenger traffic, airport revenues, traveller behaviour and commercial performance, while offering their outlook for recovery.

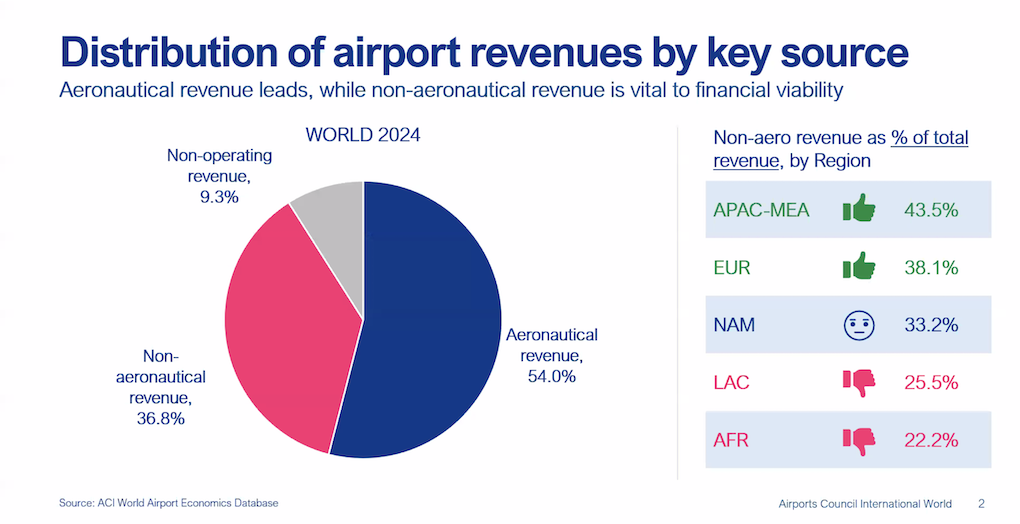

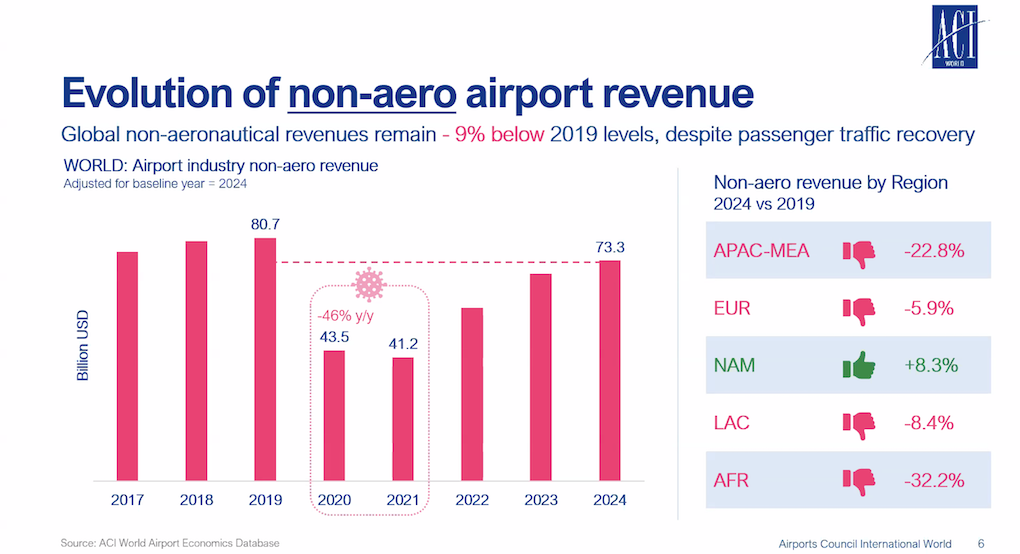

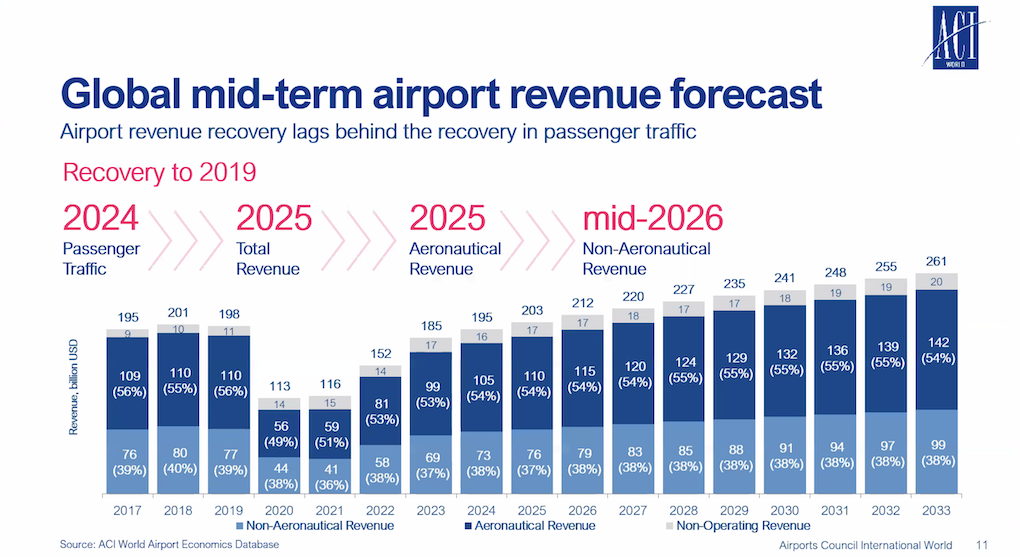

Cheglatonyev also presented an overview of global airport performance and the growing importance of non-aeronautical revenues.

He noted that airports worldwide served 9.4 billion passengers in 2024, surpassing 2019 levels by +3.6%. However, he said revenue recovery continues to lag behind passenger growth.

“Passenger volume has recovered, but airports are generating less non-aeronautical revenue per passenger than before the pandemic,” Cheglatonyev said.

In a key observation, he revealed global non-aeronautical revenue per passenger remains -12% below 2019 levels, while retail revenue per passenger is down -21%.

According to ACI World data, non-aeronautical revenues accounted for 37% of total airport revenues in 2024 and covered approximately 48% of airport operating costs globally.

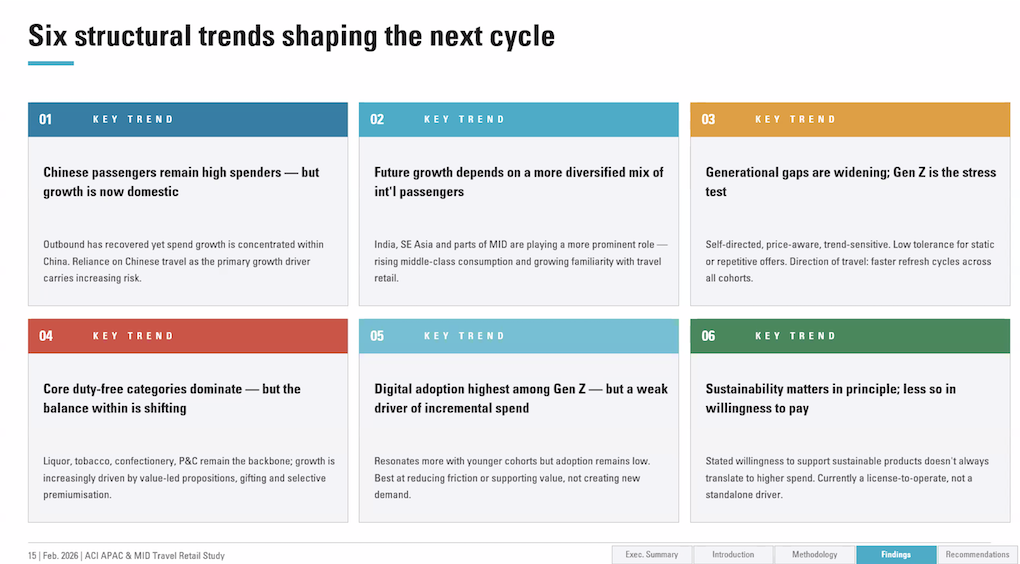

Drawing on findings from a travel retail study presented at The Trinity Forum in Doha this February, Cheglatonyev argued “the challenge facing airport retail today is no longer recovery but relevance”.

He highlighted several trends reshaping travel retail, including the diversification of traveller demographics, the increasing influence of Gen Z consumers, growing demand for premiumisation and gifting, and the role of digital tools in reducing friction throughout the airport journey.

The largest adjustment concerns the Middle East, where passenger traffic is now projected to decline by around -10.5% year-on-year due to the long-running war.

However, he sounded a more upbeat longer-term prognosis, commenting, “Despite geopolitical disruptions and changing consumer behaviour, the long-term outlook for aviation remains strong and resilient.

“We do not currently assume a structural change in long-term traffic growth.”

Looking ahead, Agzoul argued that flexibility will be critical, particularly in airport concession agreements.

“The classic concession-based contract model based on a blind minimum annual guarantee can work well when traffic and sales are growing, but it is often inappropriate during times of crisis,” he said.

“Put simply, as a retailer, we cannot guarantee sales to passengers who are not there.”

Asked why non-aeronautical revenues remain below pre-pandemic levels, Cheglatonyev pointed to growing competition from ecommerce, evolving passenger expectations and what he described as an “attention economy”.

“Airports and commercial partners compete not only for passengers’ wallets but also for their time and attention,” he said.

On recovery prospects, he suggested that the Middle East is likely to experience a gradual rather than rapid rebound.

Agzoul stressed the industry’s response must be rooted in partnership.

He said, “Partnership and collaboration are key to overcoming crises, generating opportunities and increasing value in the medium and long term.

“We hear the word resilience a lot in our industry, but it is the Middle East region that perhaps most embodies that resilience.

“I have every confidence that we will emerge stronger from this crisis and continue to set new standards for travel retail.” ✈